Downloaded 111 times

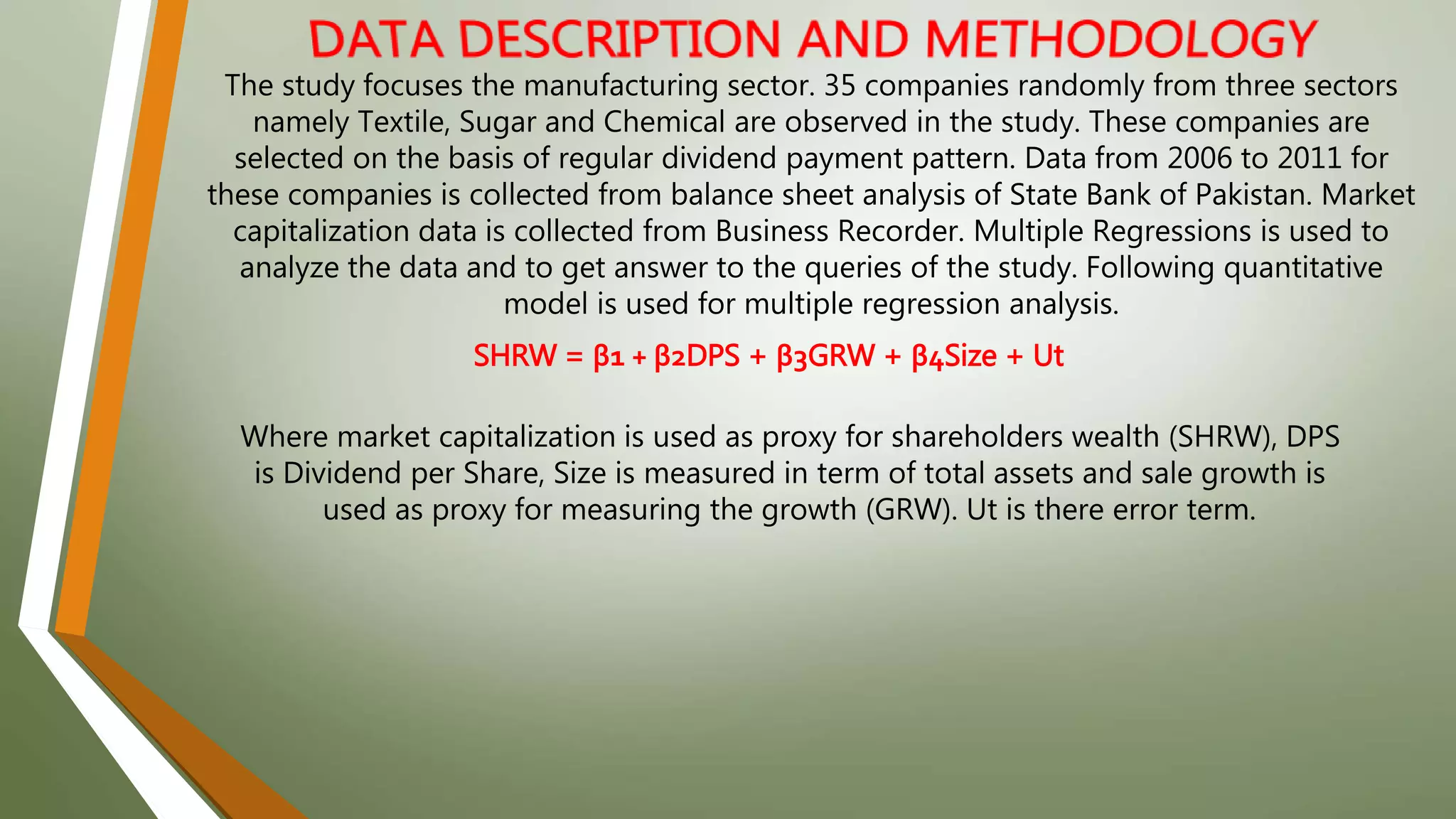

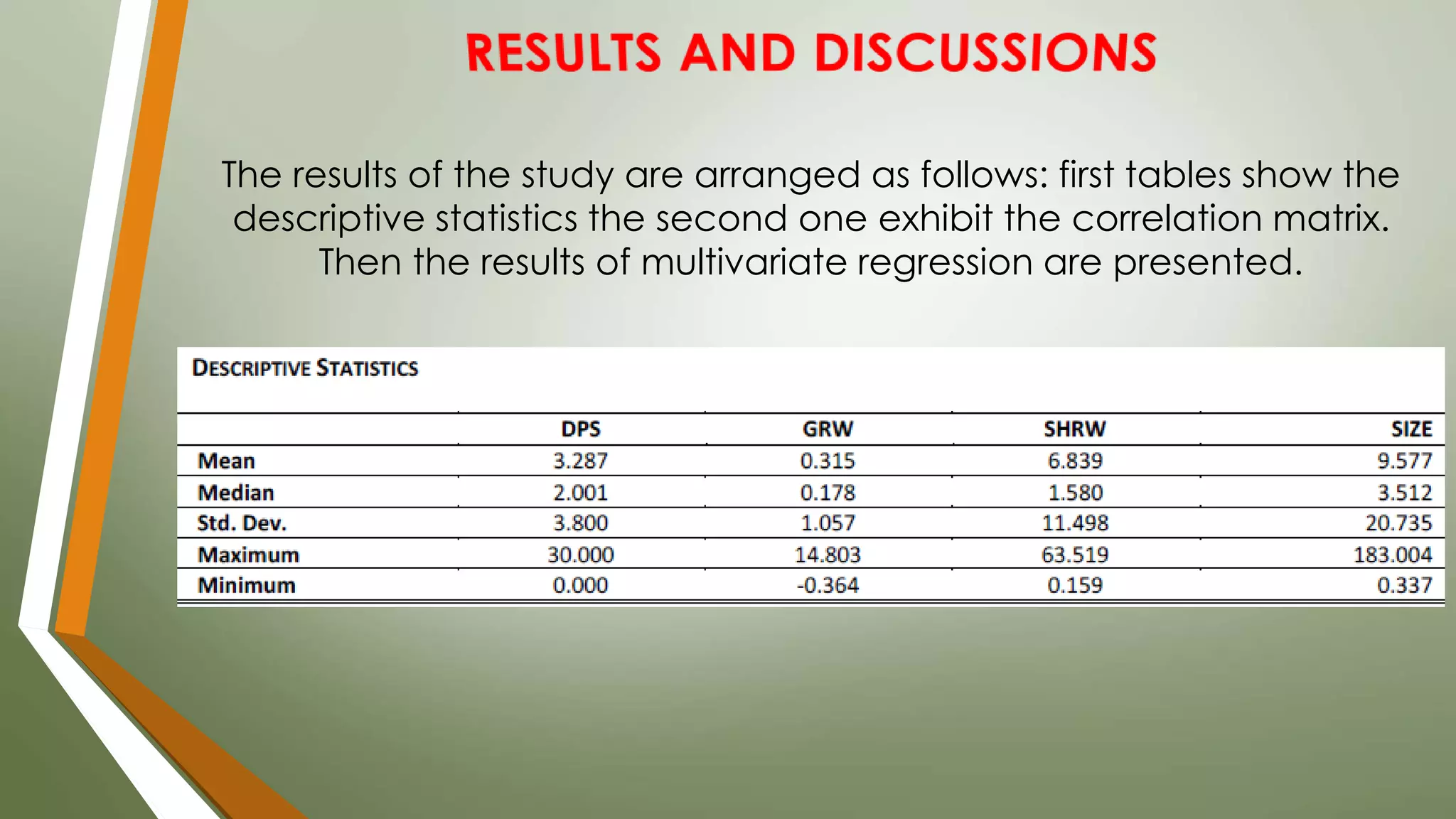

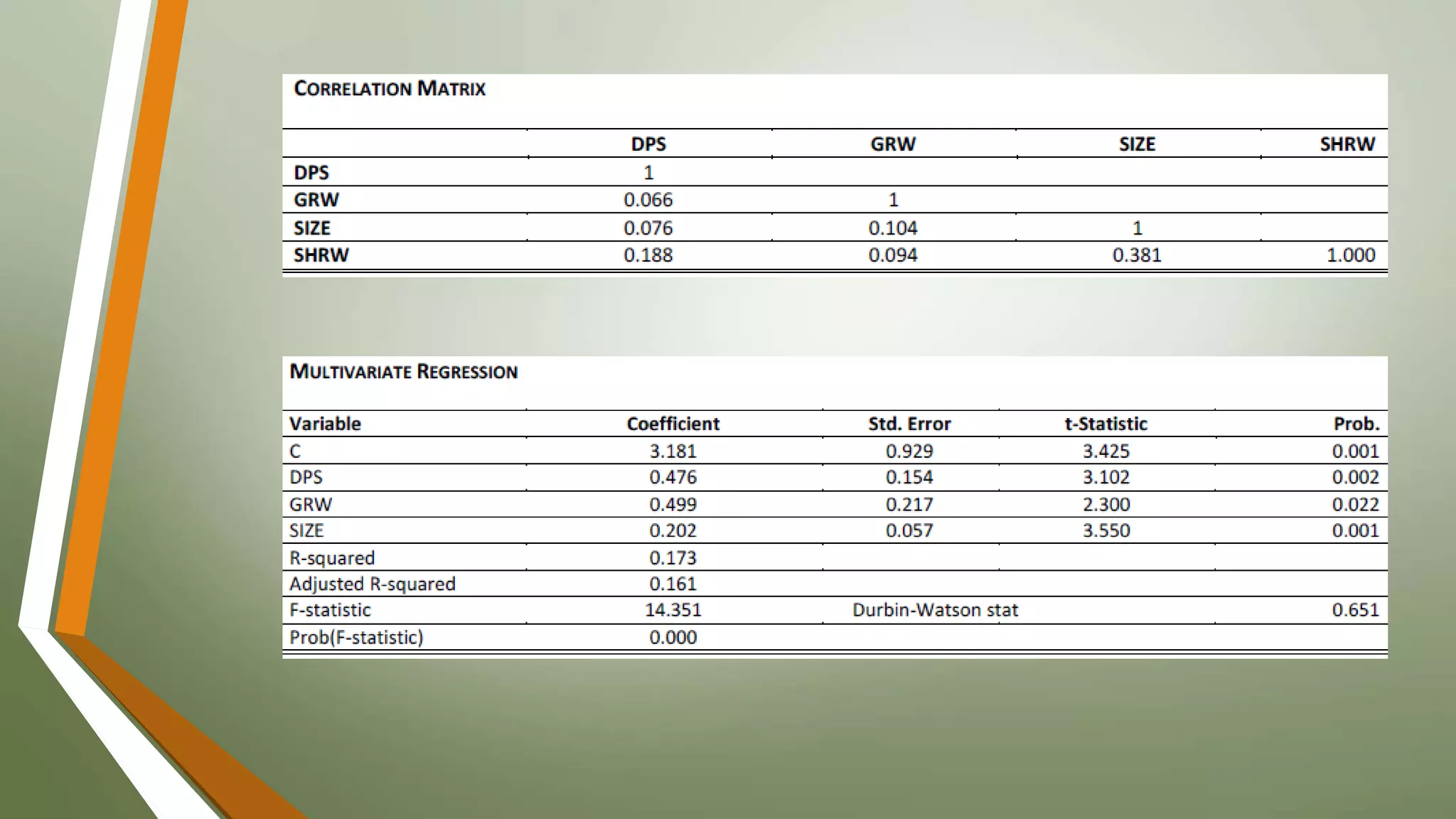

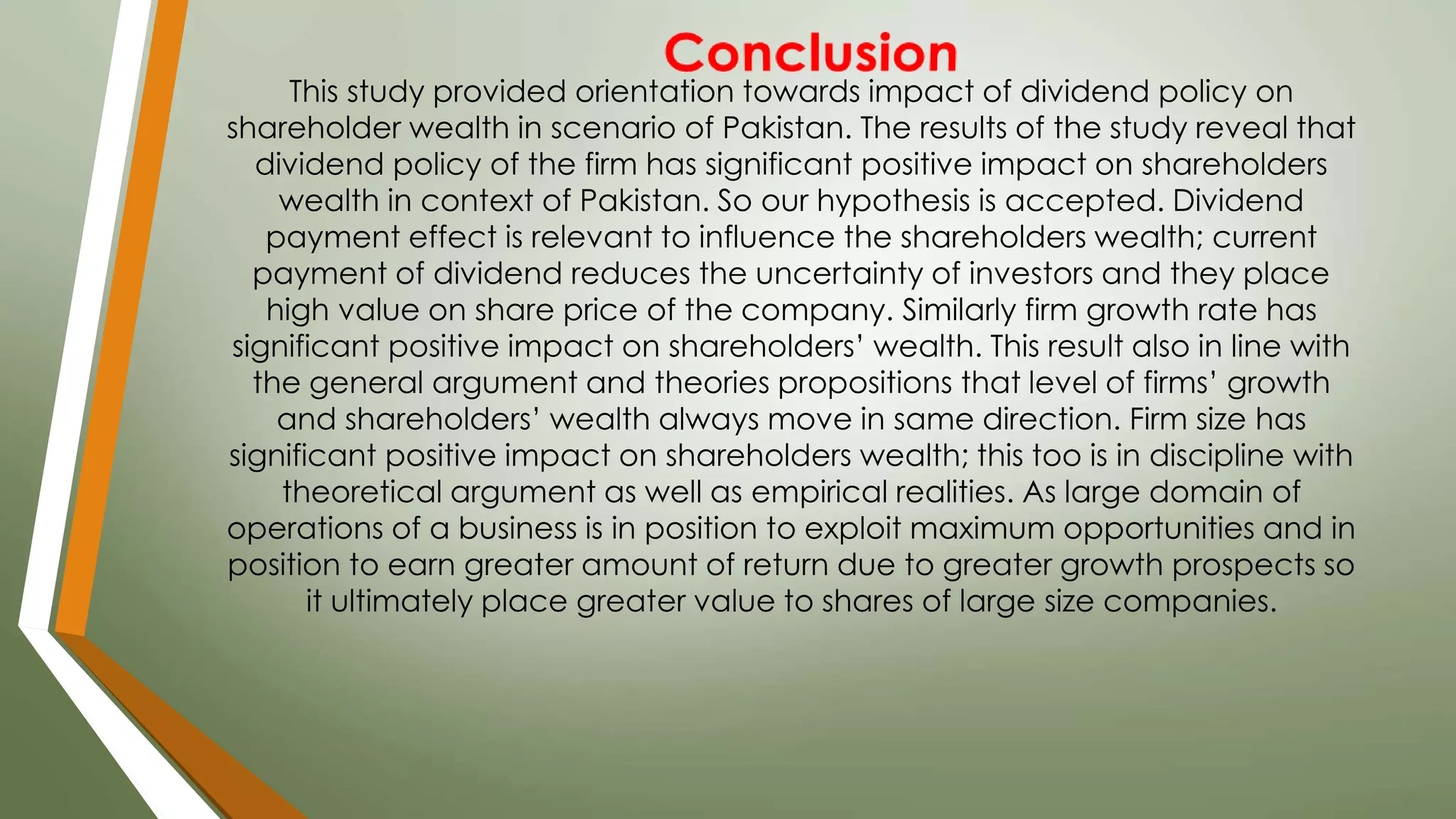

This study investigates the impact of dividend policy on shareholders' wealth in selected manufacturing industries in Pakistan, analyzing 35 companies across textile, sugar, and chemical sectors from 2006 to 2011. The findings indicate that a firm's dividend policy, growth rate, and size significantly and positively affect shareholder wealth, highlighting the importance of stable dividend payments for attracting investors. Ultimately, credible dividend policies can enhance market value and influence financial decision-making among corporate managers.

![Determinants of[1]](https://cdn.slidesharecdn.com/ss_thumbnails/determinantsof1-111212023317-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)