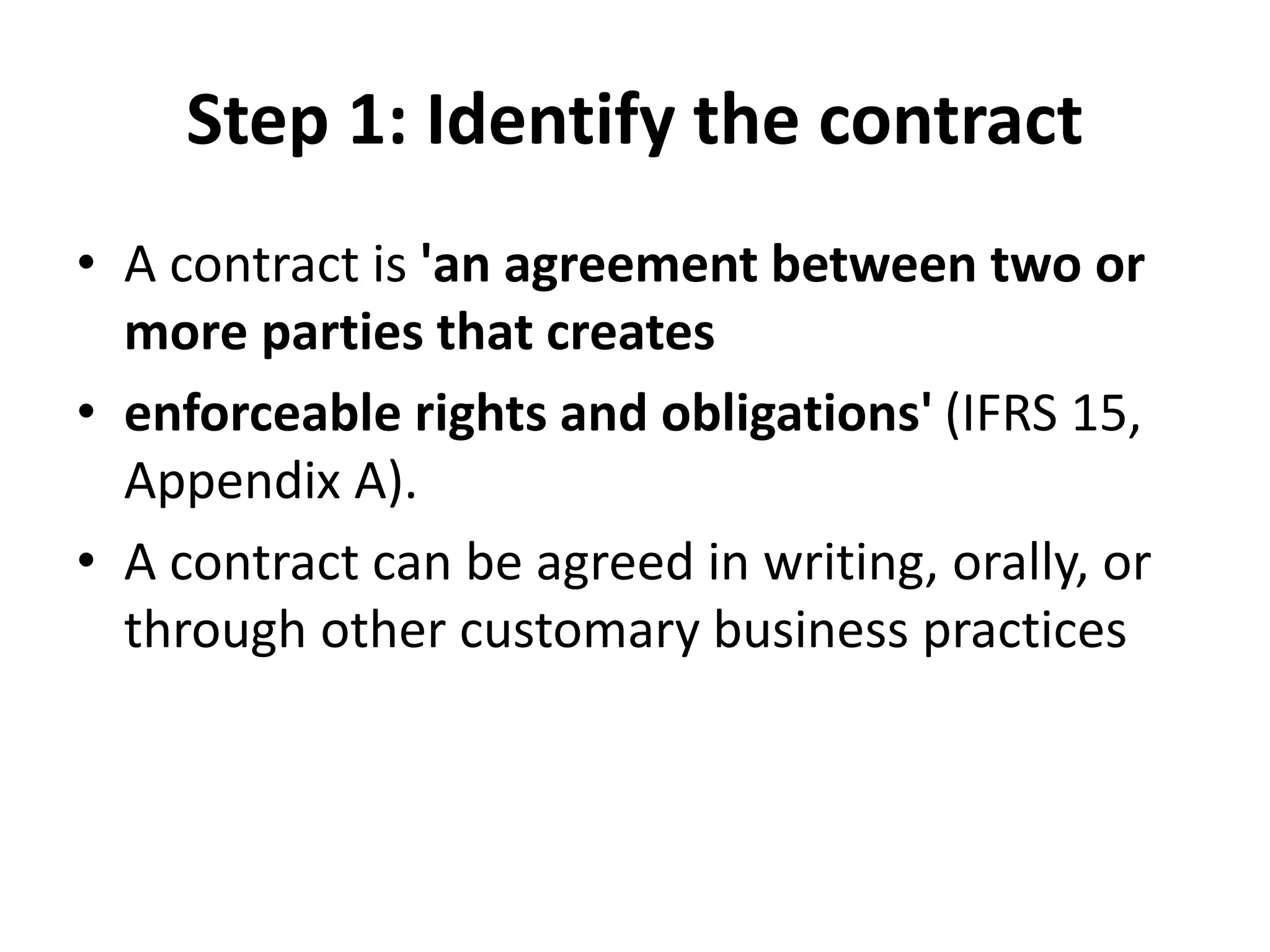

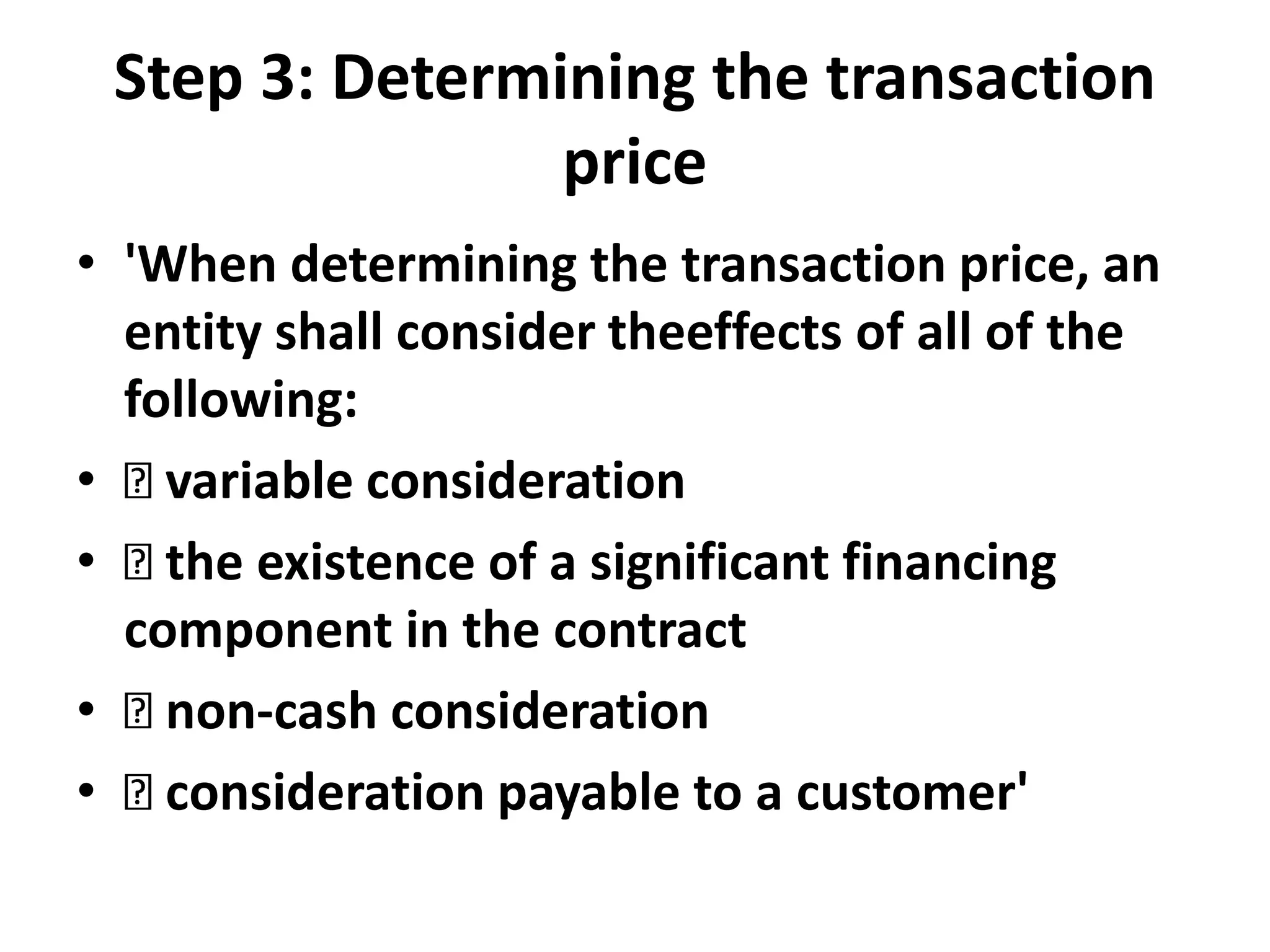

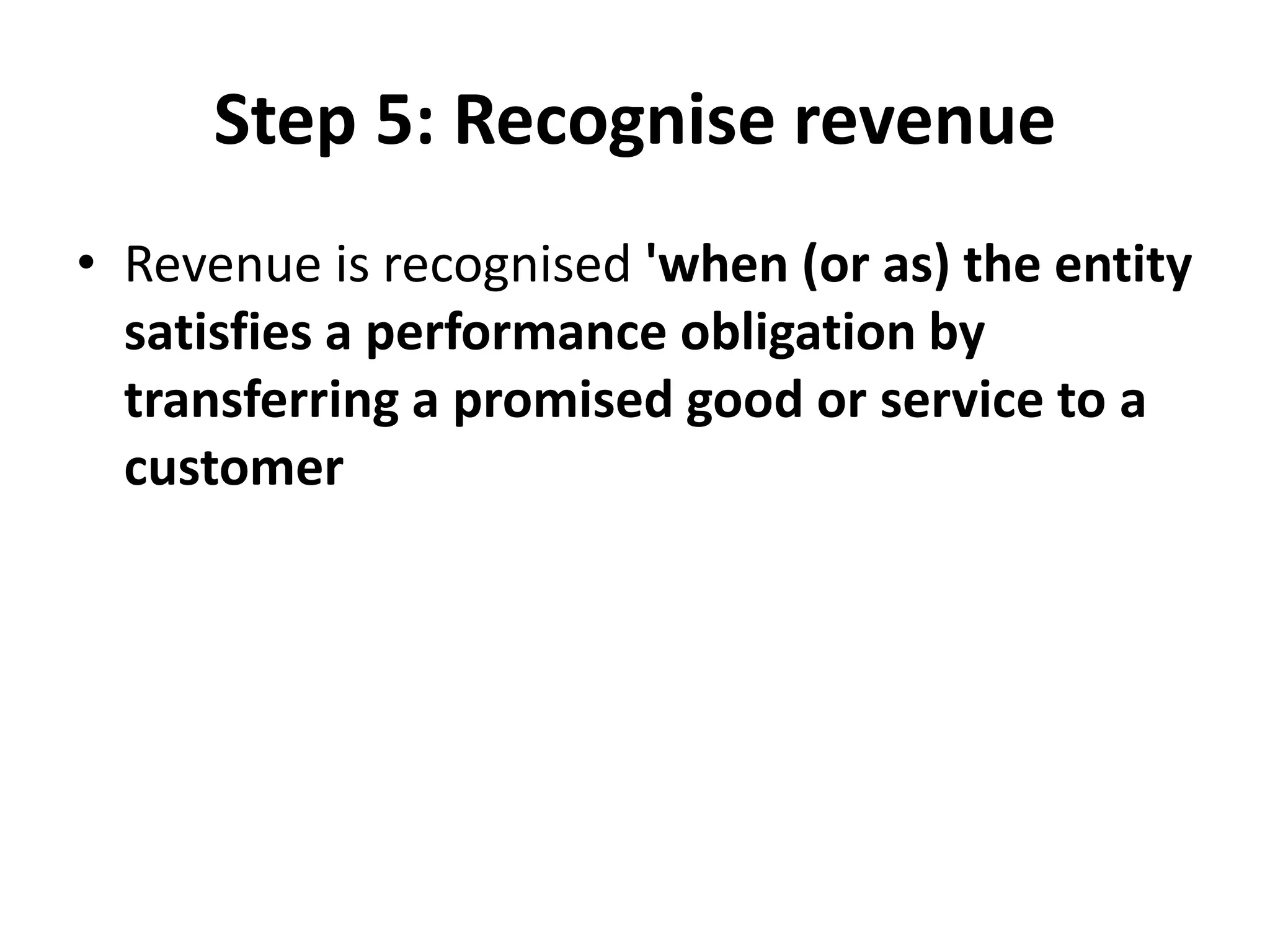

The document outlines the five-step process for revenue recognition under IFRS 15. The steps are: 1) identify the contract, 2) identify separate performance obligations, 3) determine the transaction price, 4) allocate the transaction price to each obligation, and 5) recognize revenue as obligations are satisfied. An example is provided of a computer sale with 12 months of technical support to illustrate applying the steps. Additional topics like repurchase agreements, bill-and-hold arrangements, and satisfying performance obligations over time are also summarized.