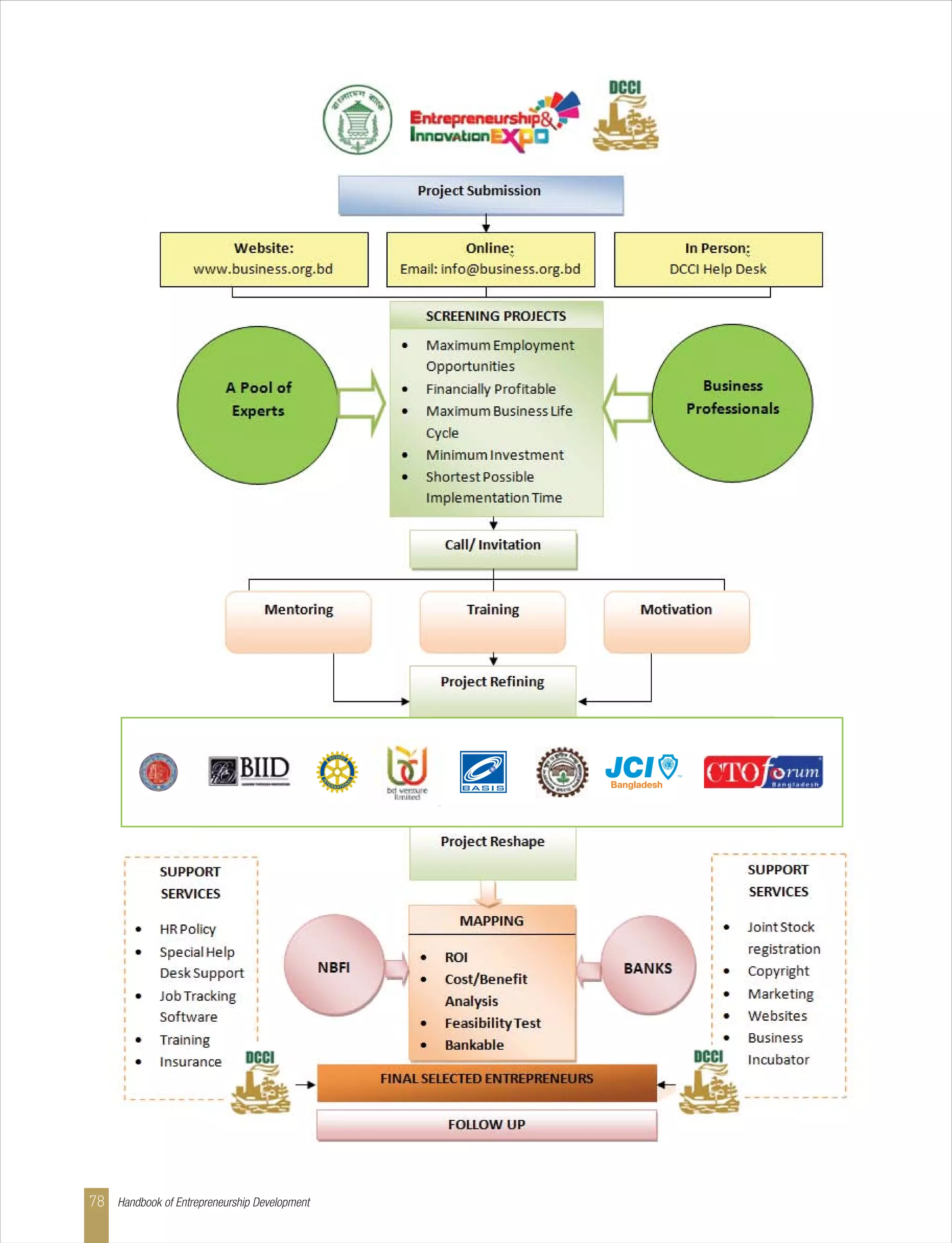

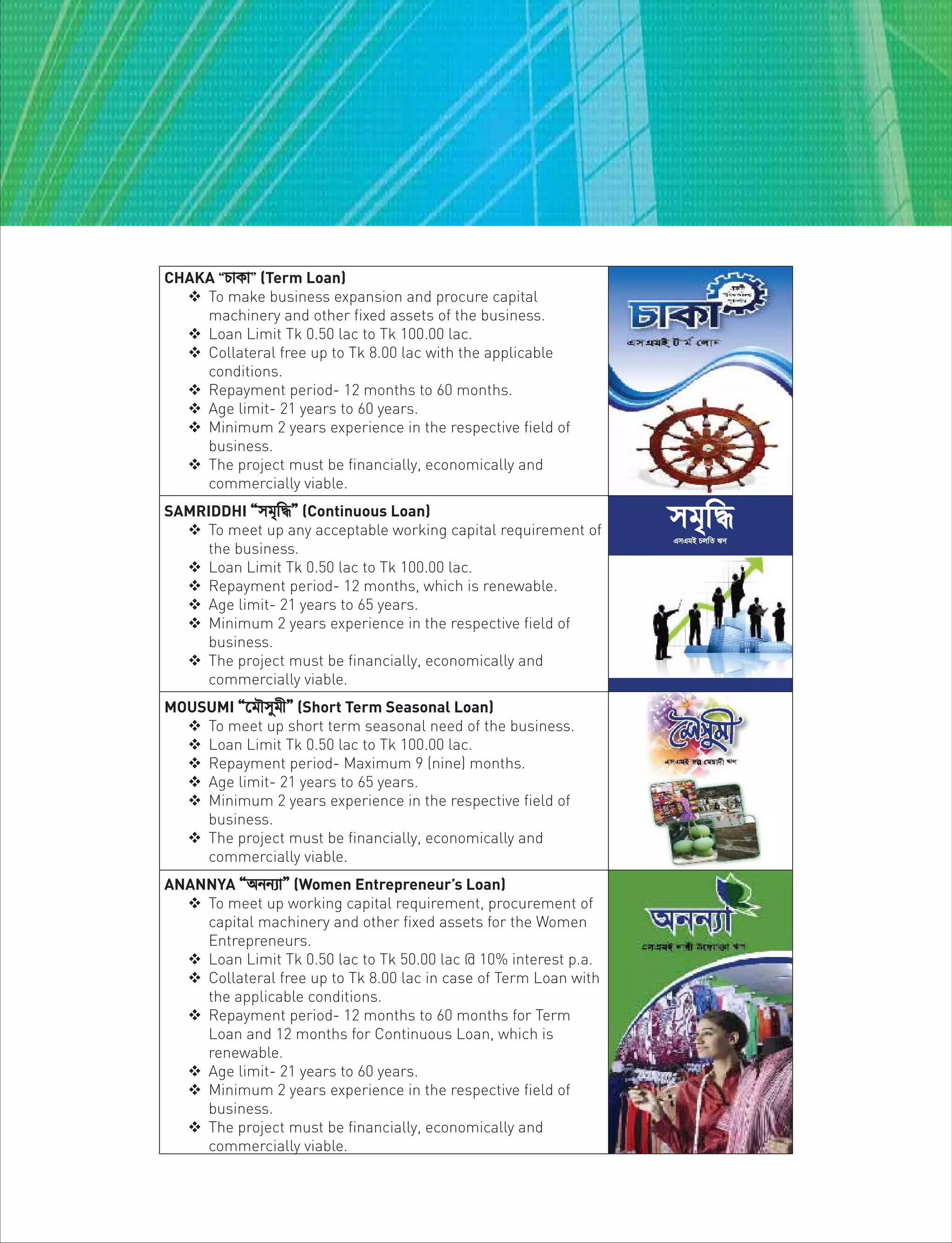

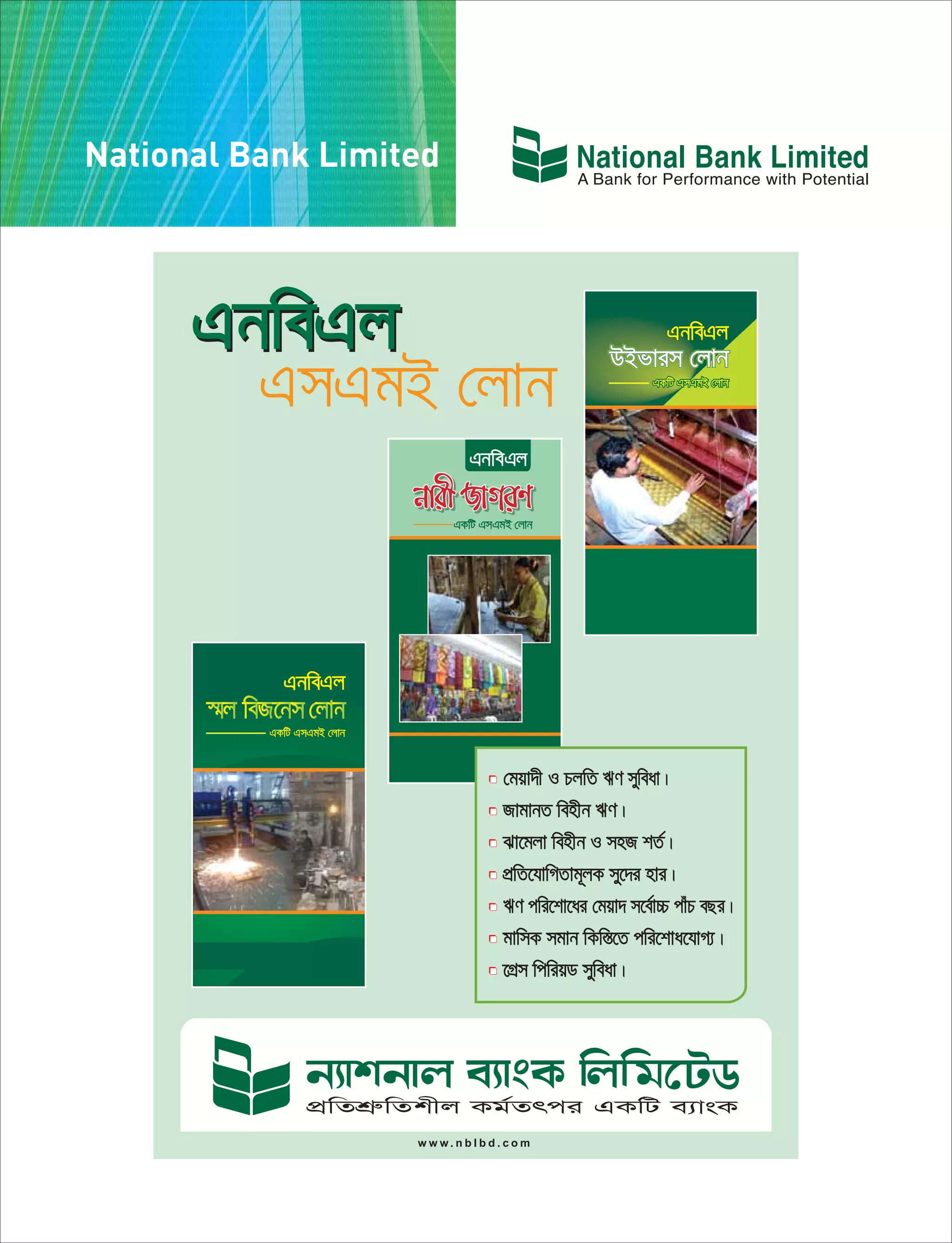

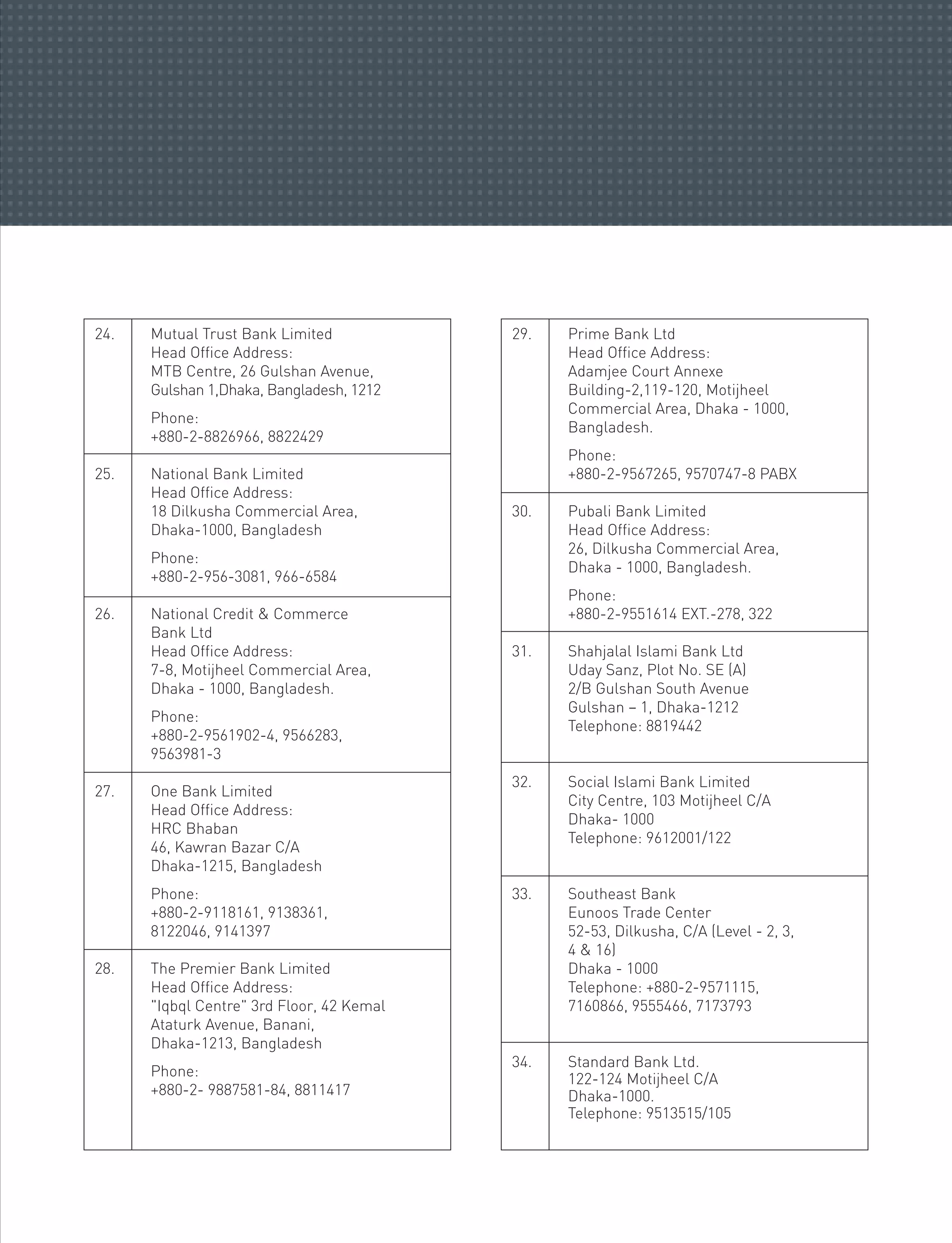

Downloaded 78 times

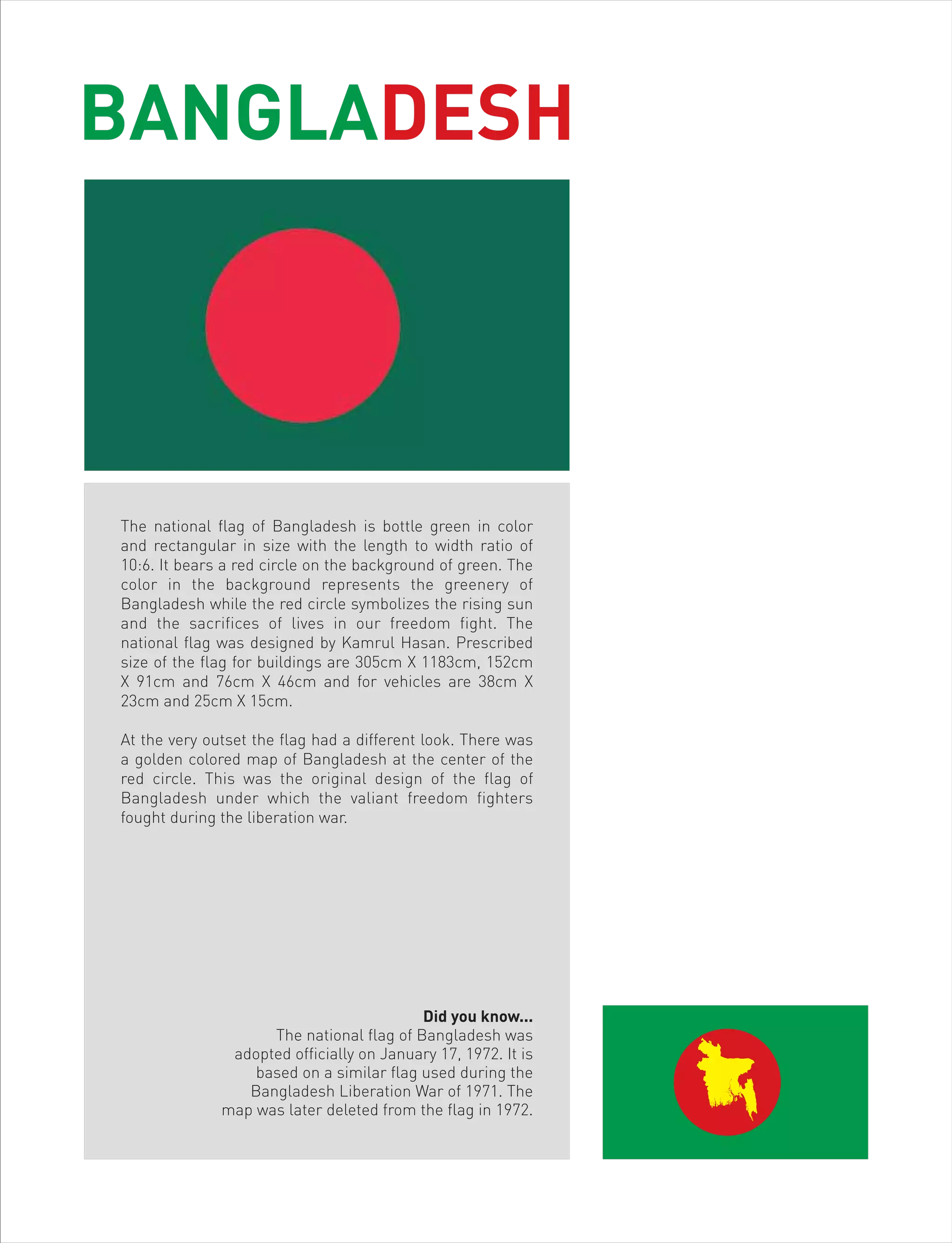

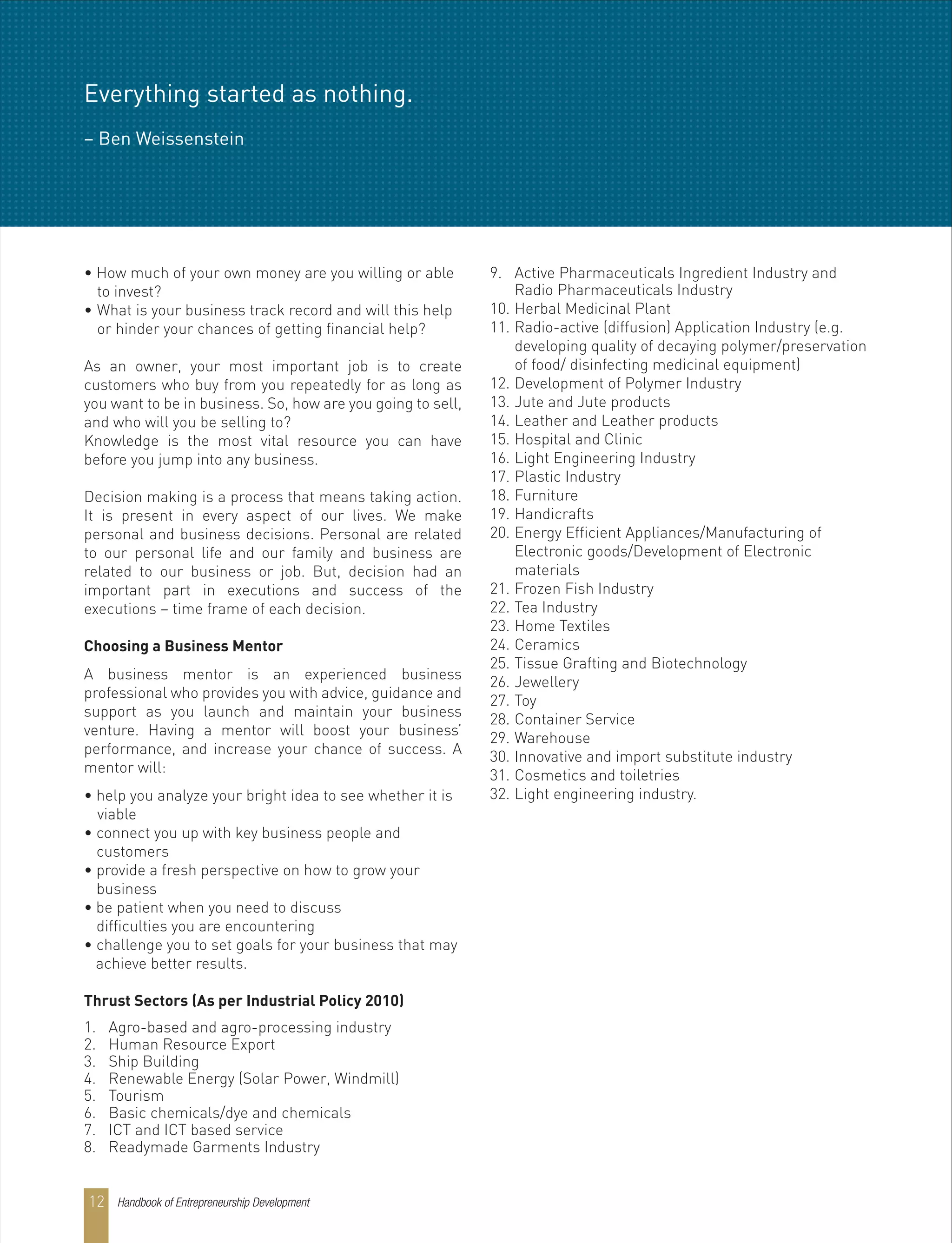

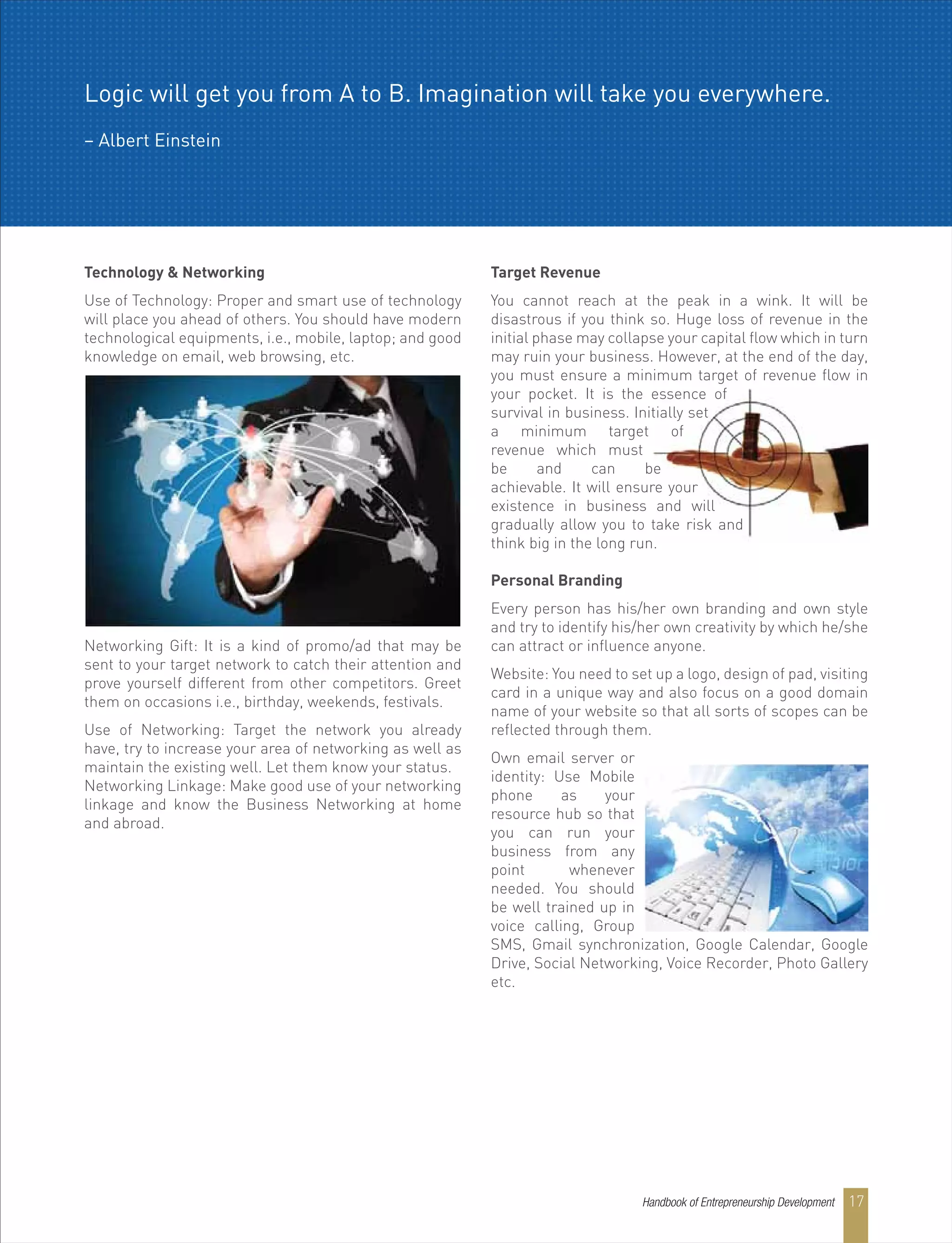

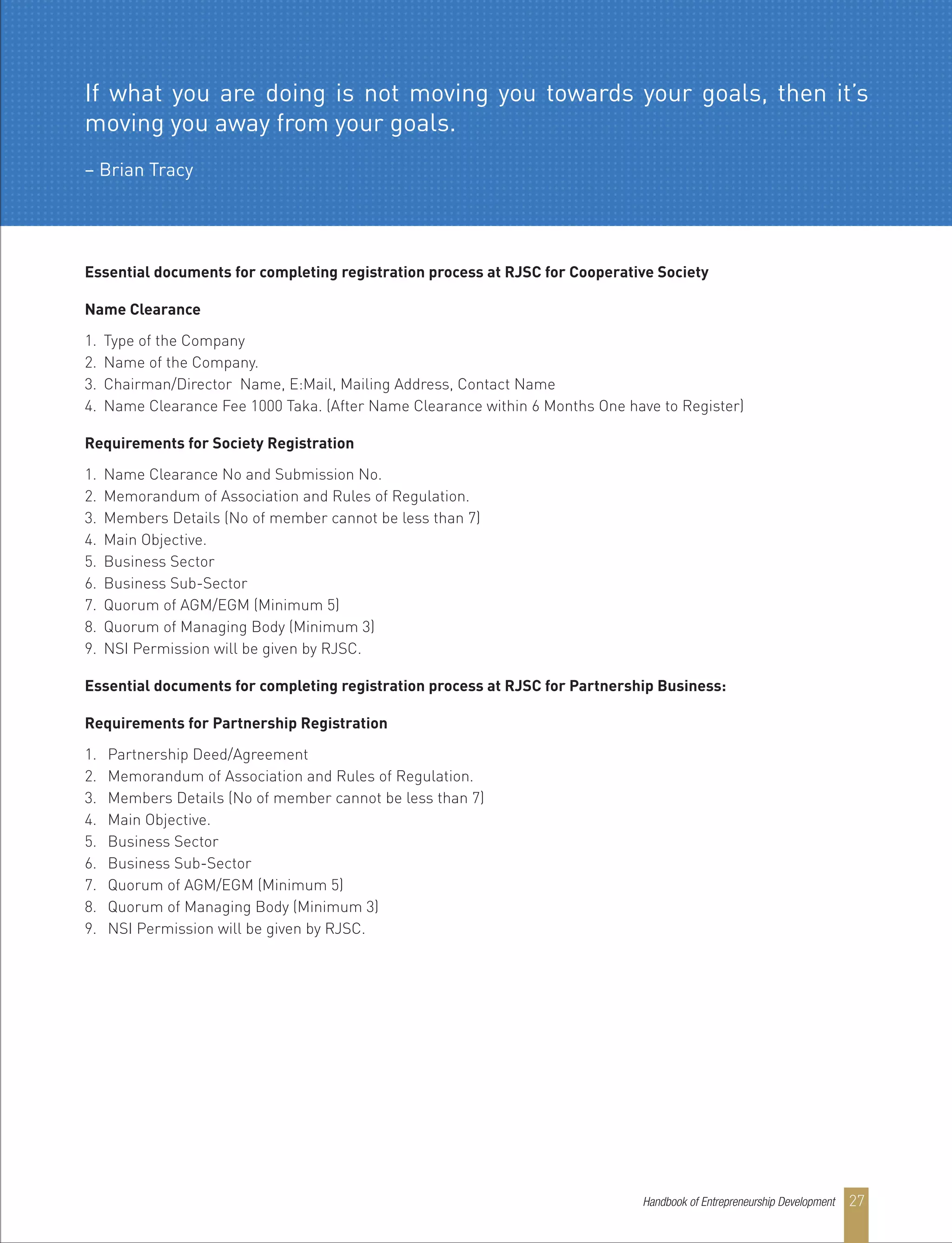

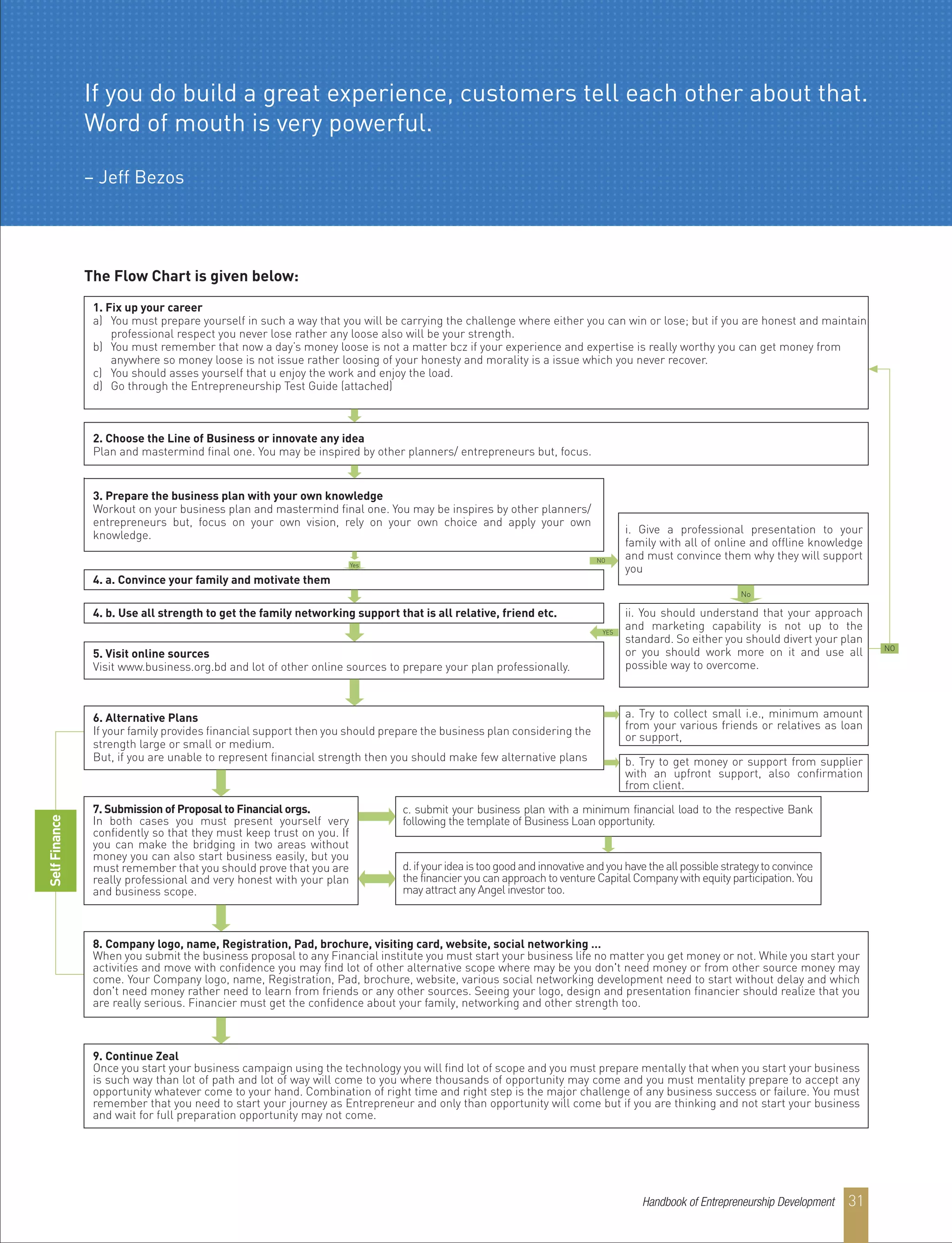

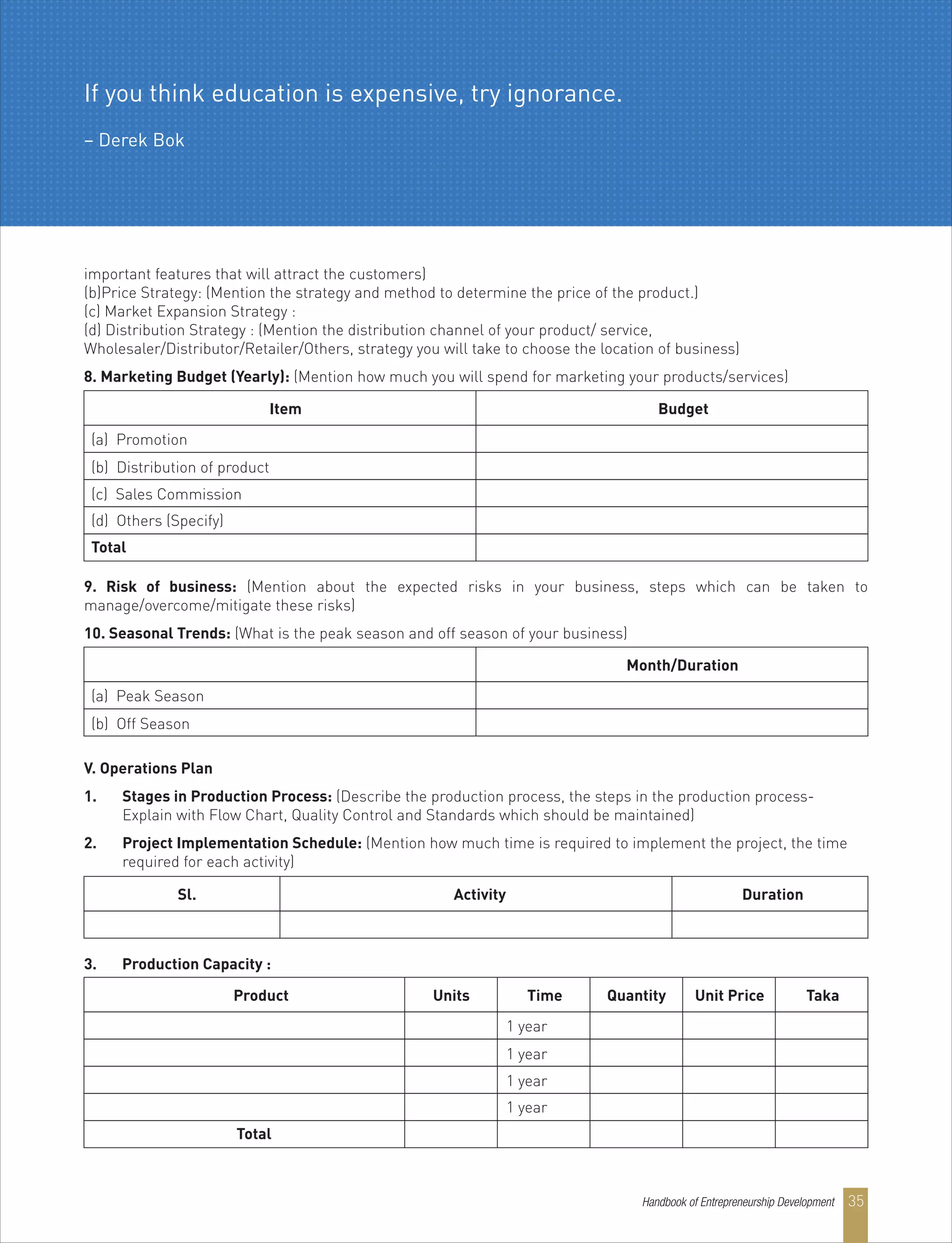

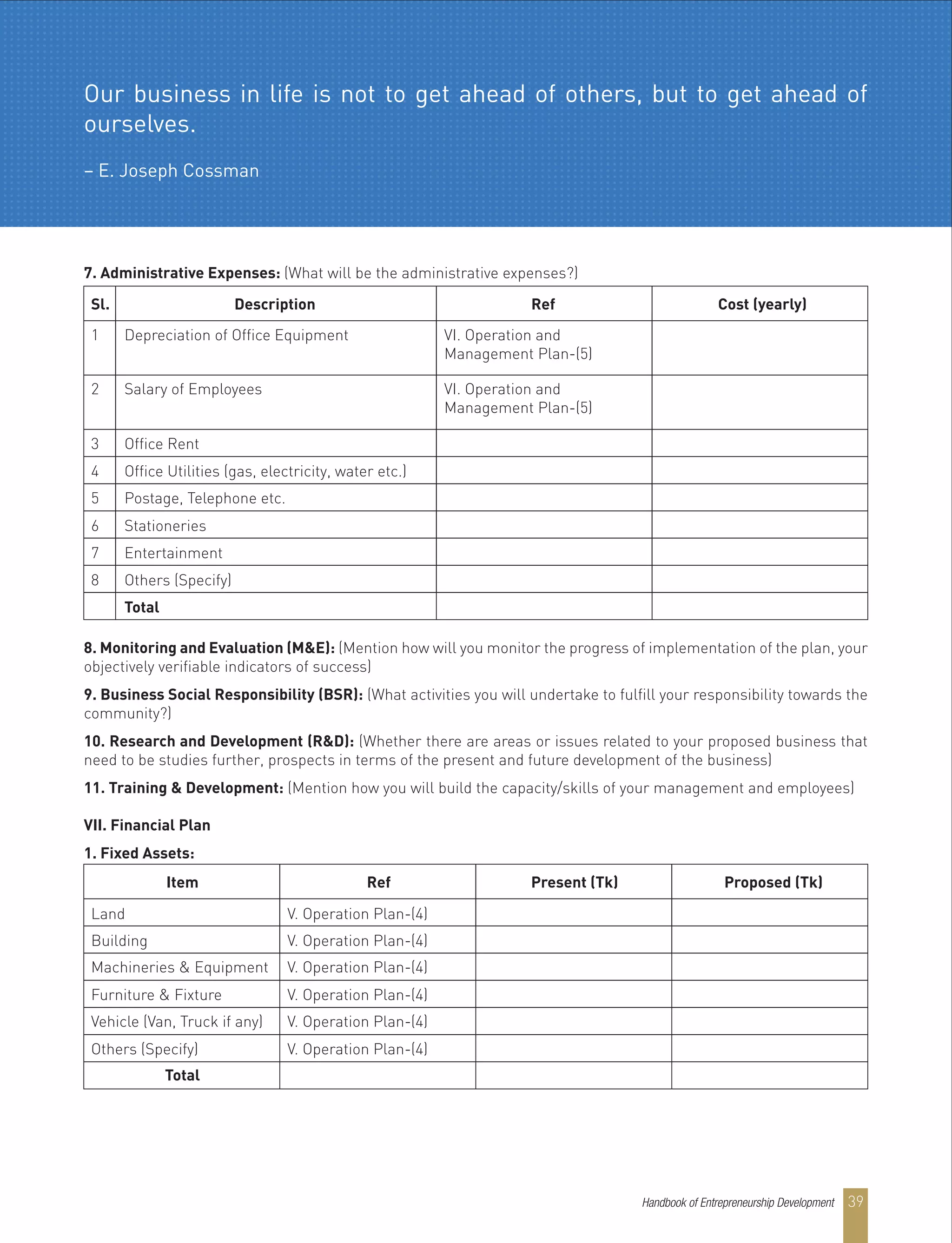

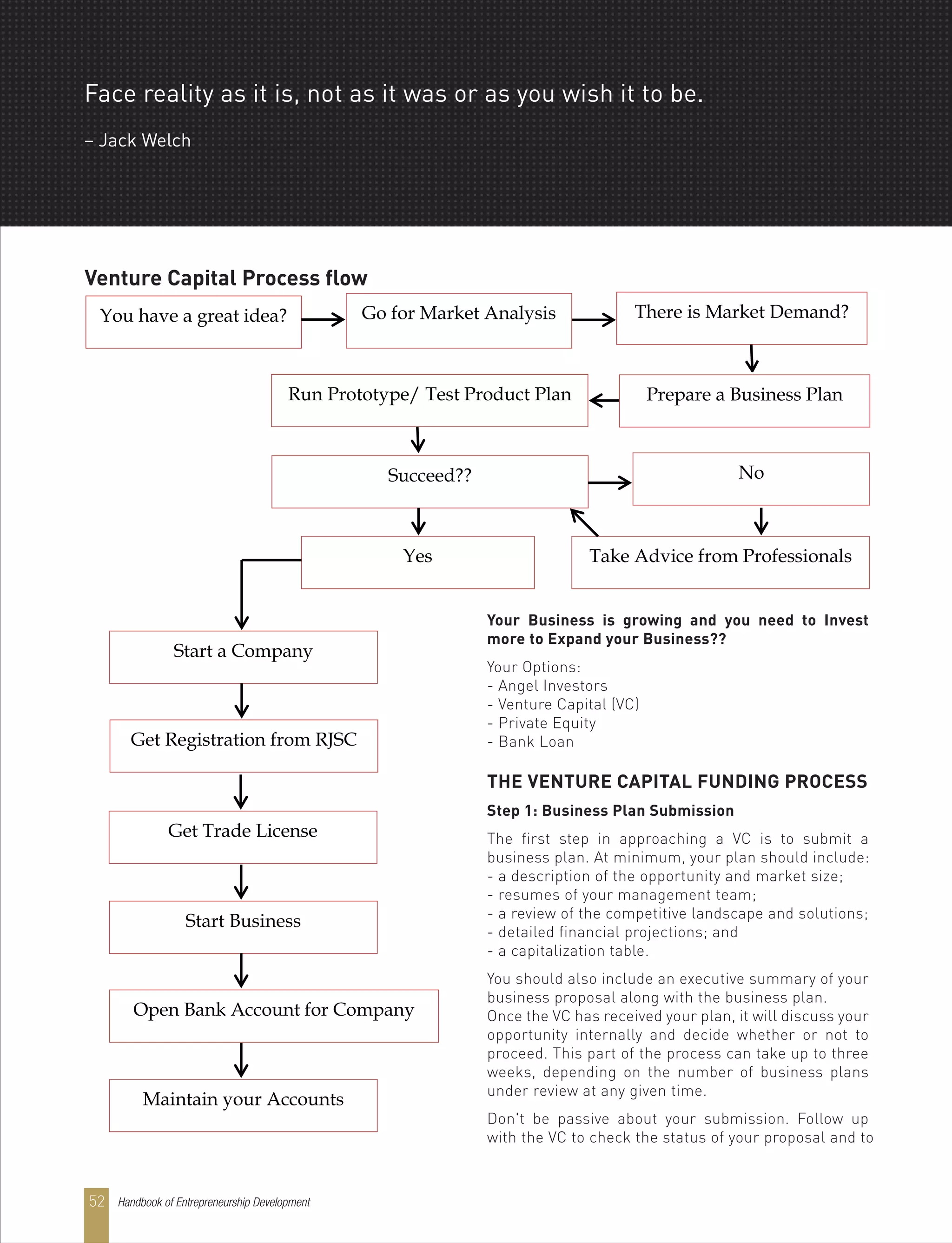

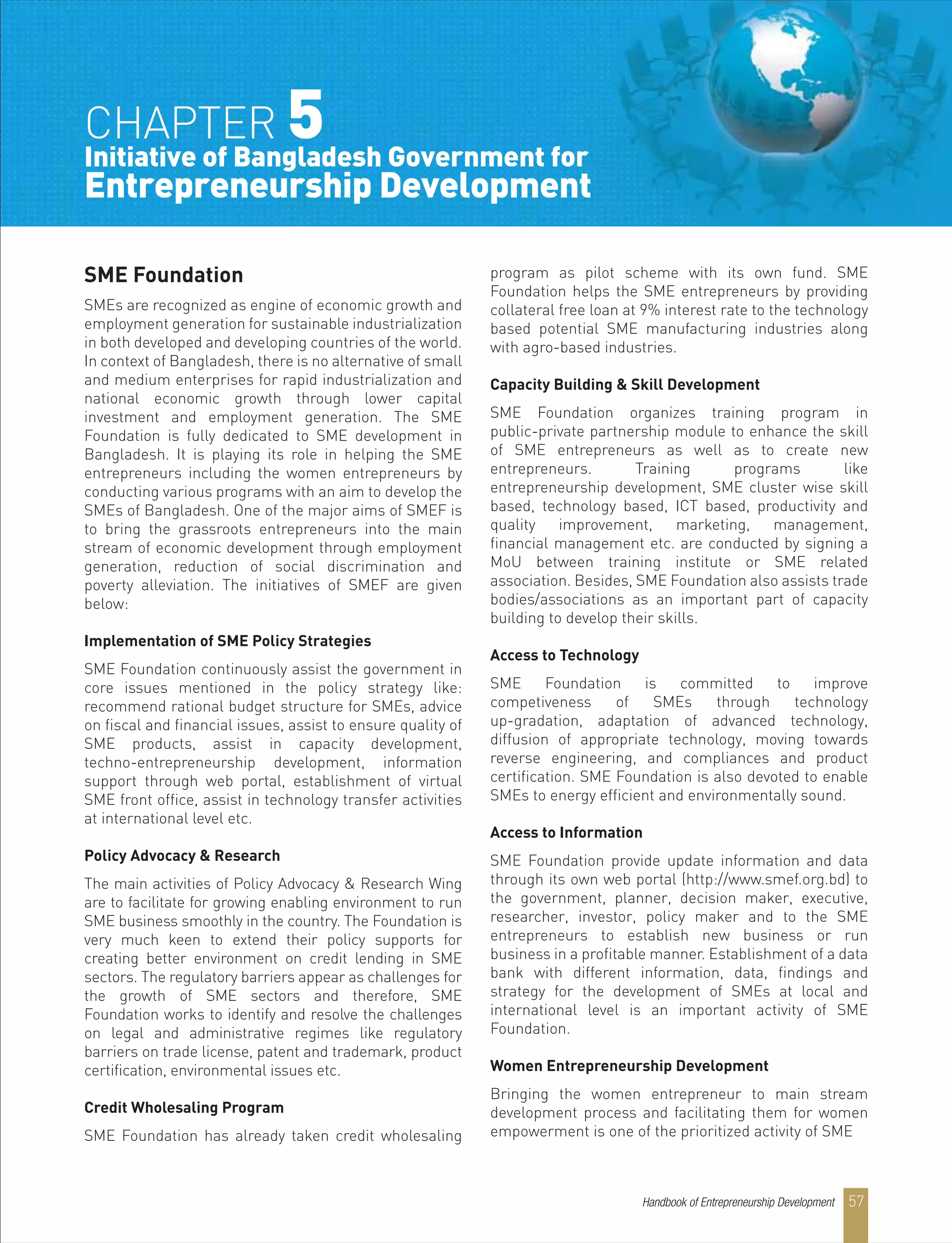

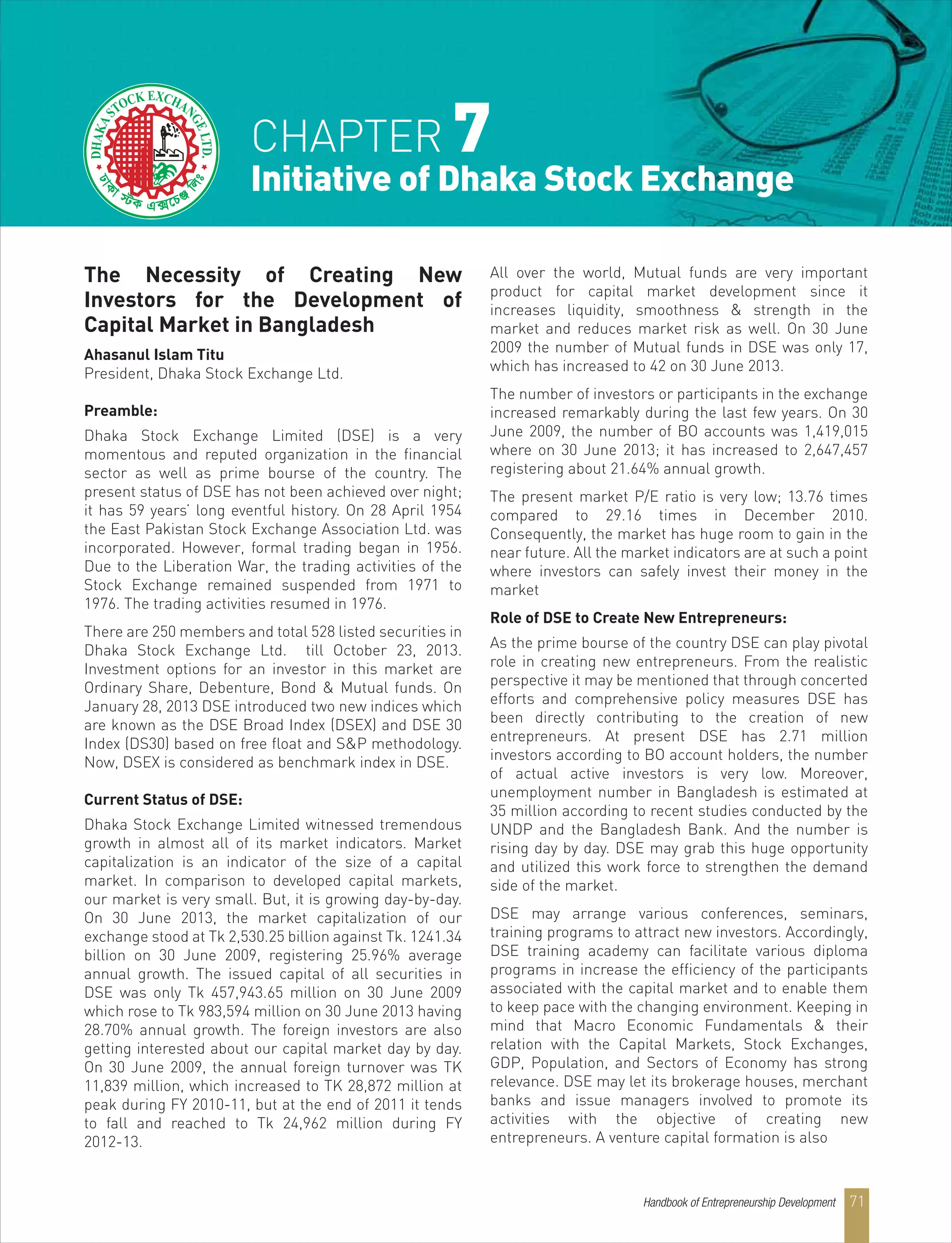

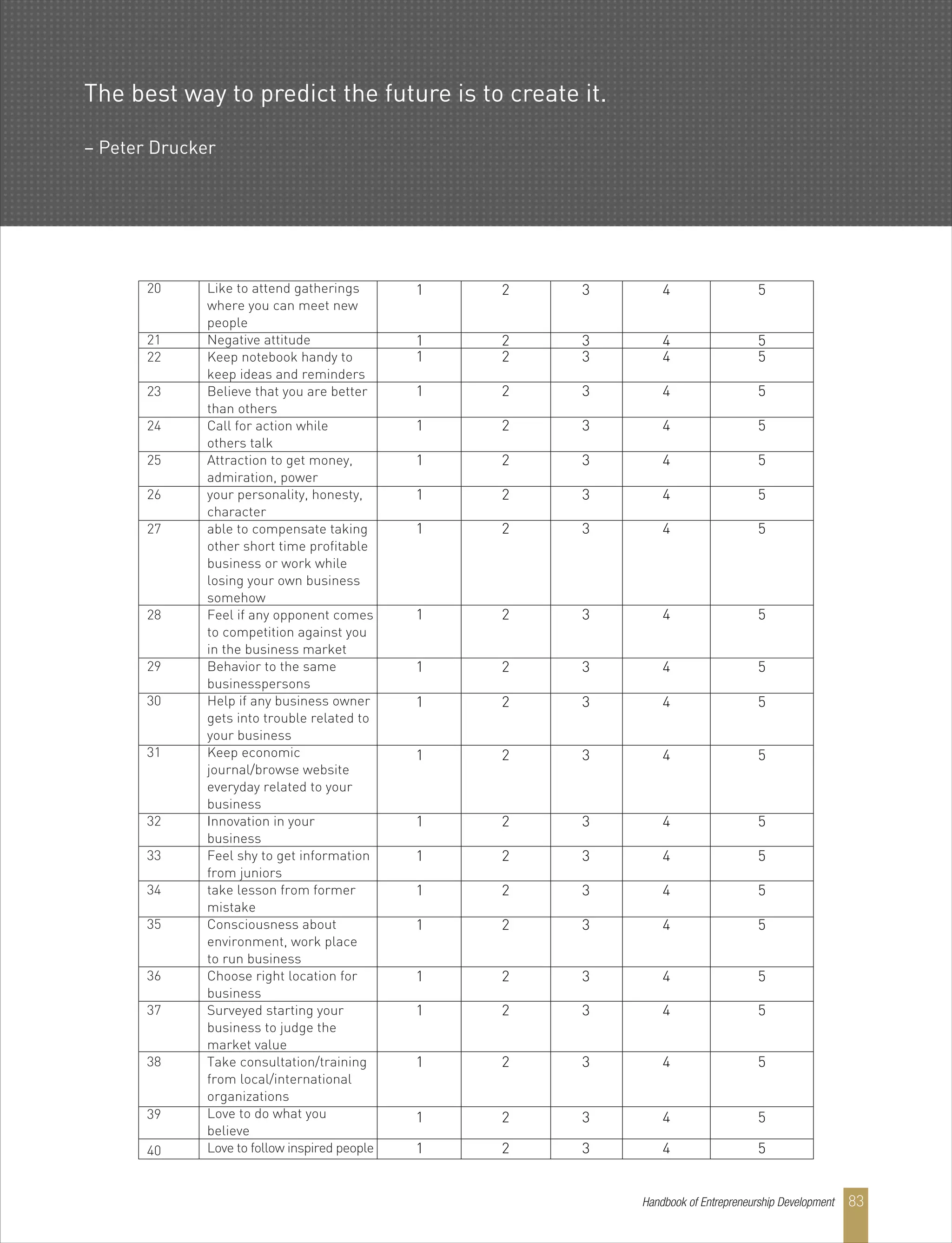

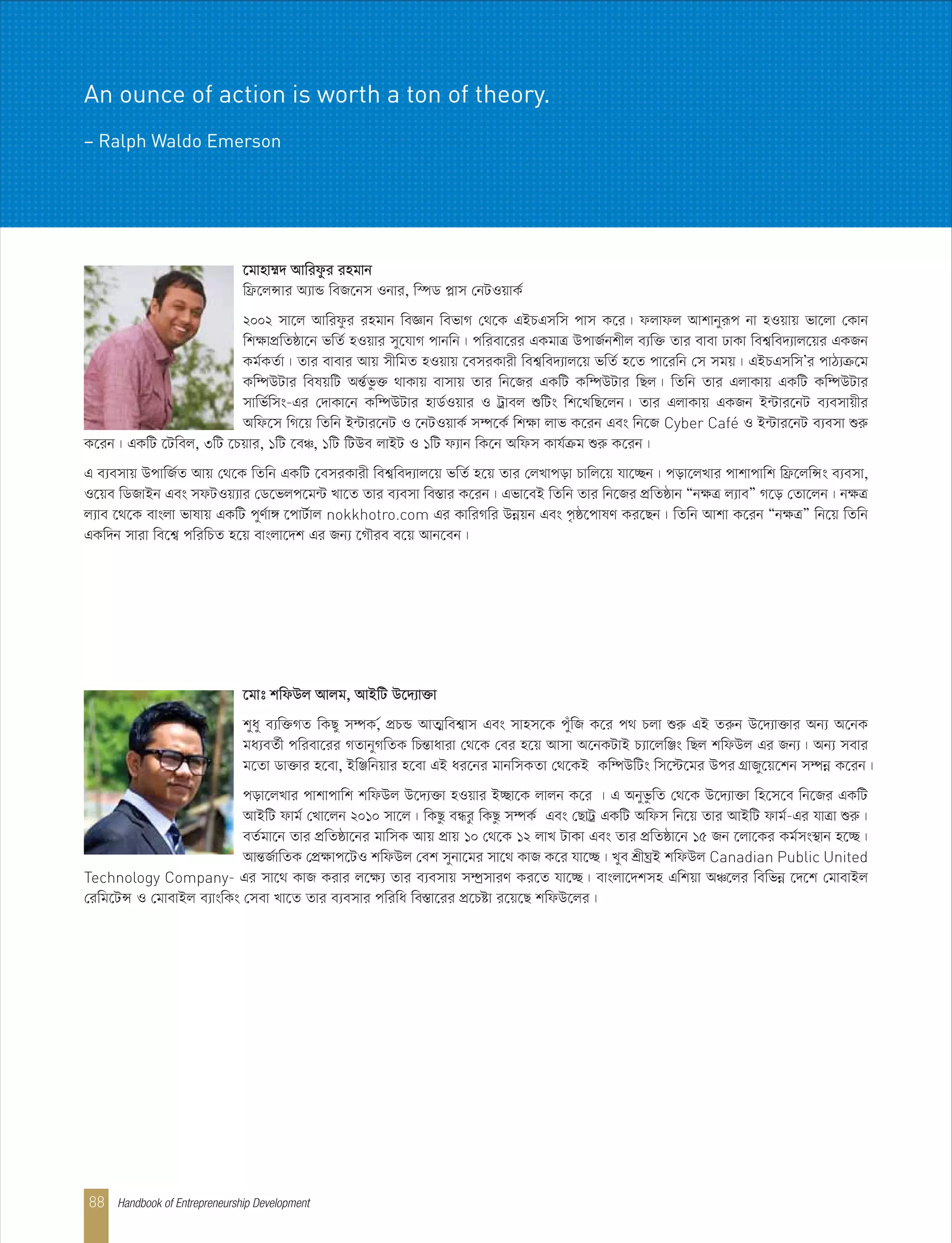

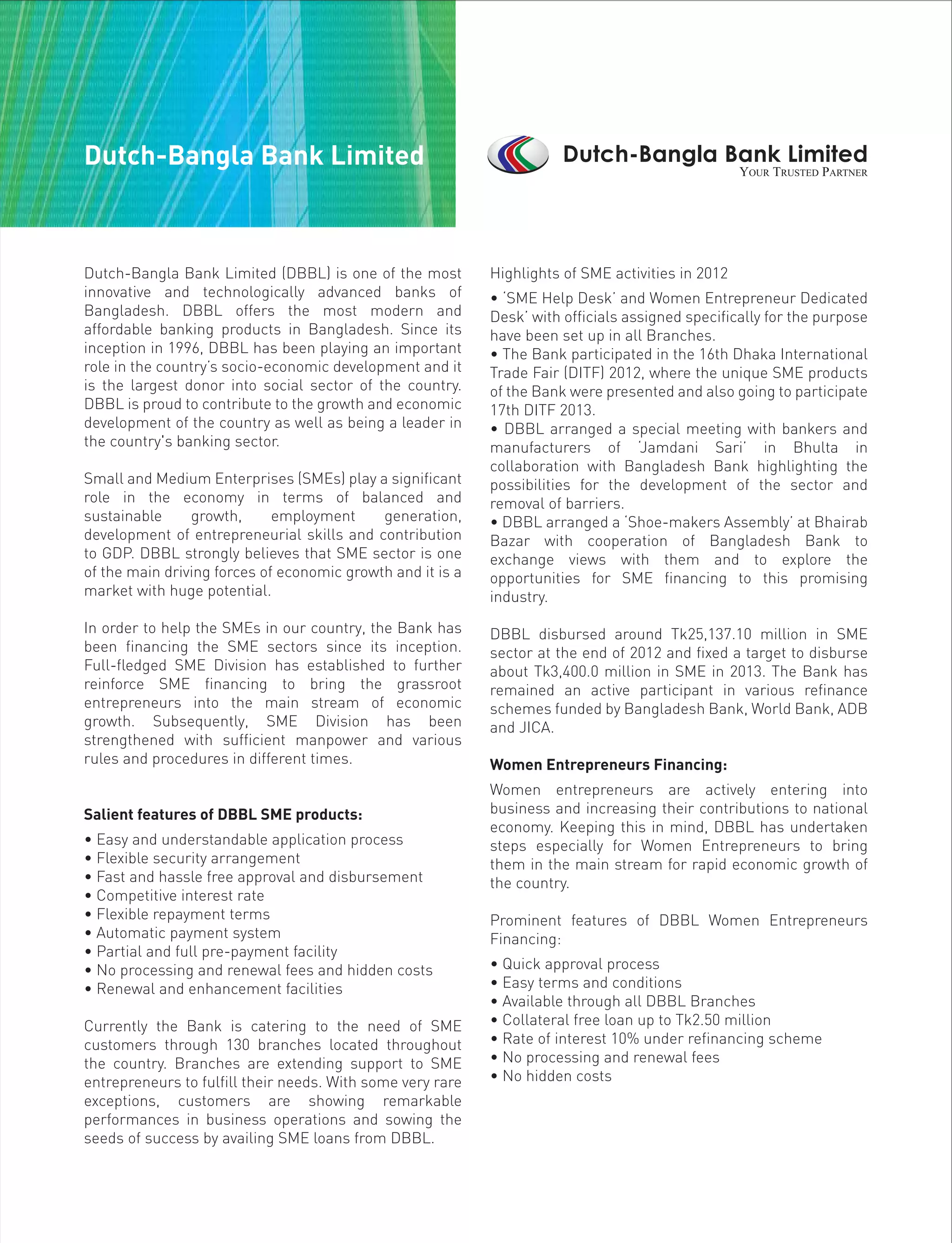

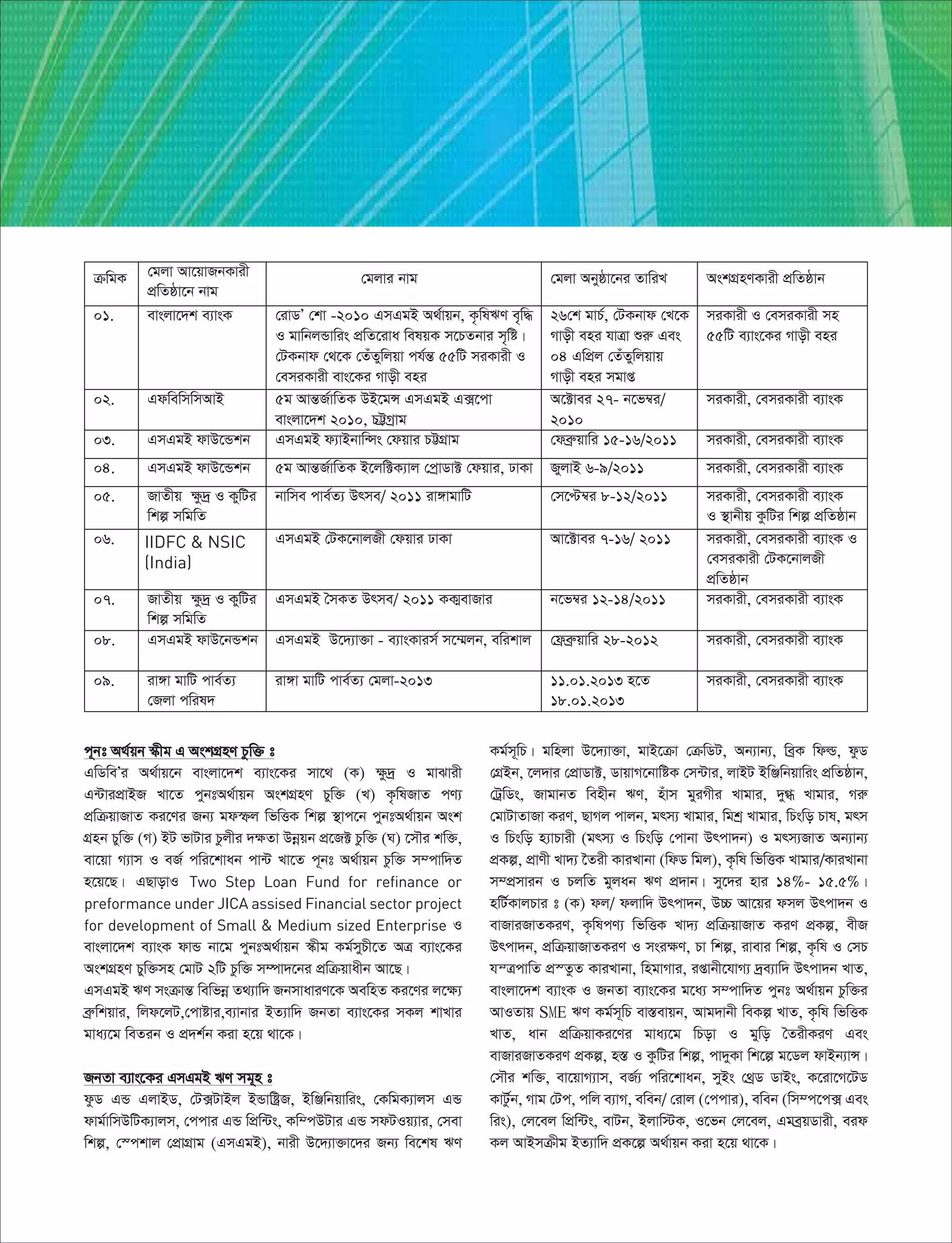

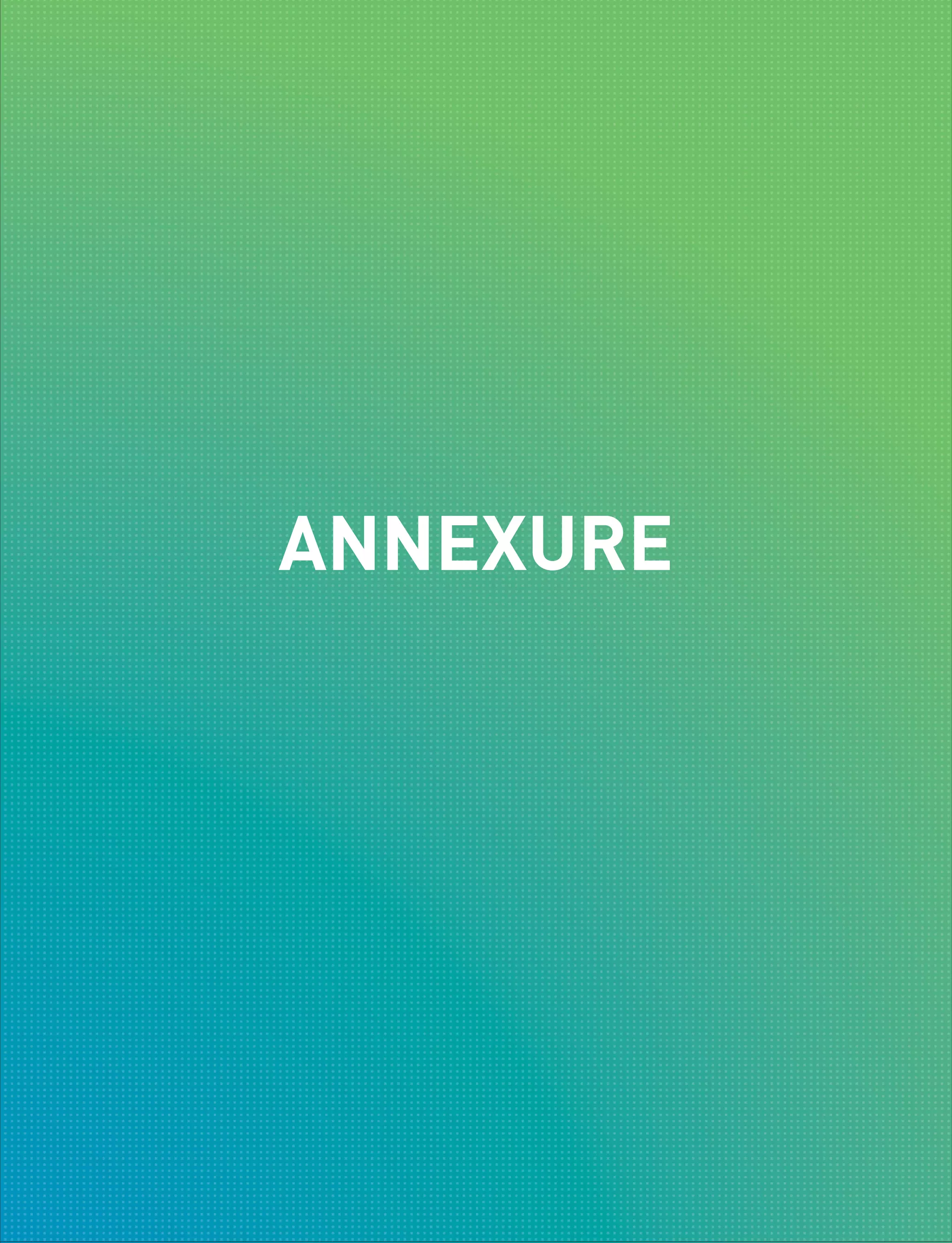

![Essential for Registration Process at RJSC for

Company

Name Clearance

1. Type of the Company

2. Name of the Company.

3. Chairman/Director Name, E:Mail, Mailing

Address, Contact Name

4. Name Clearance Fee 600 Taka. After Name

Clearance within 6 Months One have to Register)

Registration process

1. Name Clearance No and Submission No.

2. Memorandum of Association: (Soft copy + Hard

copy, Total 9 Clauses = 7 are essential, Last 2 will

be given by default by RJSC).

3. Articles of Association: (Soft copy + Hard copy,

Minimum 25 Clauses, Try to keep each Clause within

1000 digit)

4. Filled in Form IX: Consent of Director to act [Section

92]. (Should Provide Hard Copy with Chairman and

Director Signature + Soft Copy)

5. Particulars of Individual Subscriber: Particulars of

the Directors, Manager and Managing Agents and of

any change therein [Section 115] (Should Provide

Soft Copy for every Managing Directors, Directors,

Managers)

6. Subscribe Page: (Should Provide Hard Copy with

Chairman and Director Signature + Soft Copy) + Two

Witness Name, Position, Address, and Contact.

Registration of RJSC

Provide

Proposed

Name

Search:

Proposed

Name

Check: Status

& Print: Name

Clearance Letter

Deposit Fee:

In the

Particular Bank

Print:

Acknowledgment

& Bank Slip

Apply: Desired

Name

Name Clearance

Easy Process of Company Registration at DCCI Help Desk

Collect:

Certificate of

Incorporation &

Certified Copies

Check:

Status with

Submission

Number

Deposit Fee:

In the Particular

Bank

Print:

Acknowledgment

& Bank Slip

Visit:

www.roc.gov.bd

& Click: Apply

Fill up:

Required Fields

Upload:

Memorandum & Articles

of Association, Form IX

& Subscriber Pages

Click:

Submit and View

submissions

Associate yourself with people of good quality, for it is better to be alone

than in bad company.

– Booker T. Washington

Handbook of Entrepreneurship Development26](https://image.slidesharecdn.com/handbookofentrepreneurshipdevelopment-161028042425/75/Handbook-of-Entrepreneurship-Development-by-DCCI-28-2048.jpg)

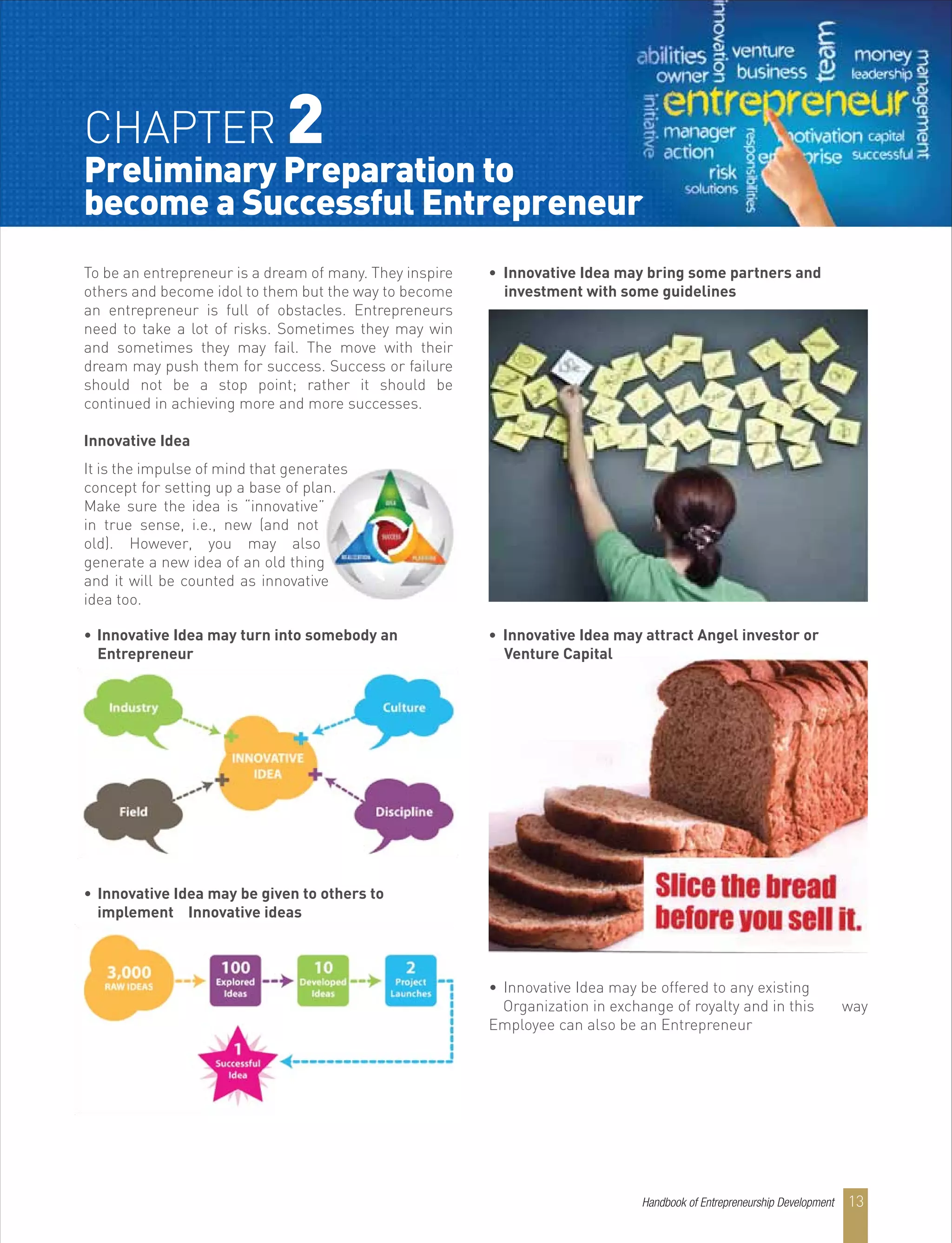

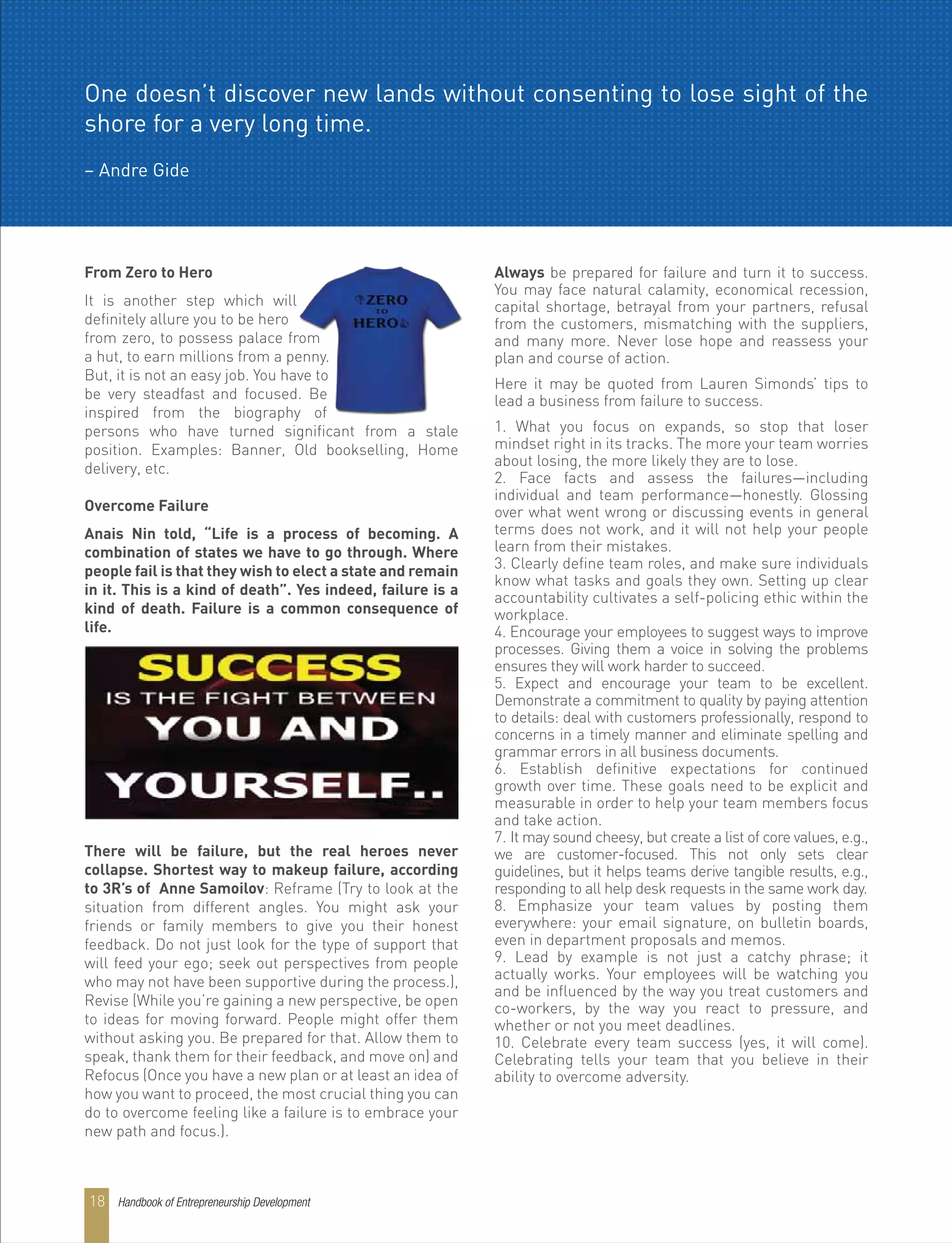

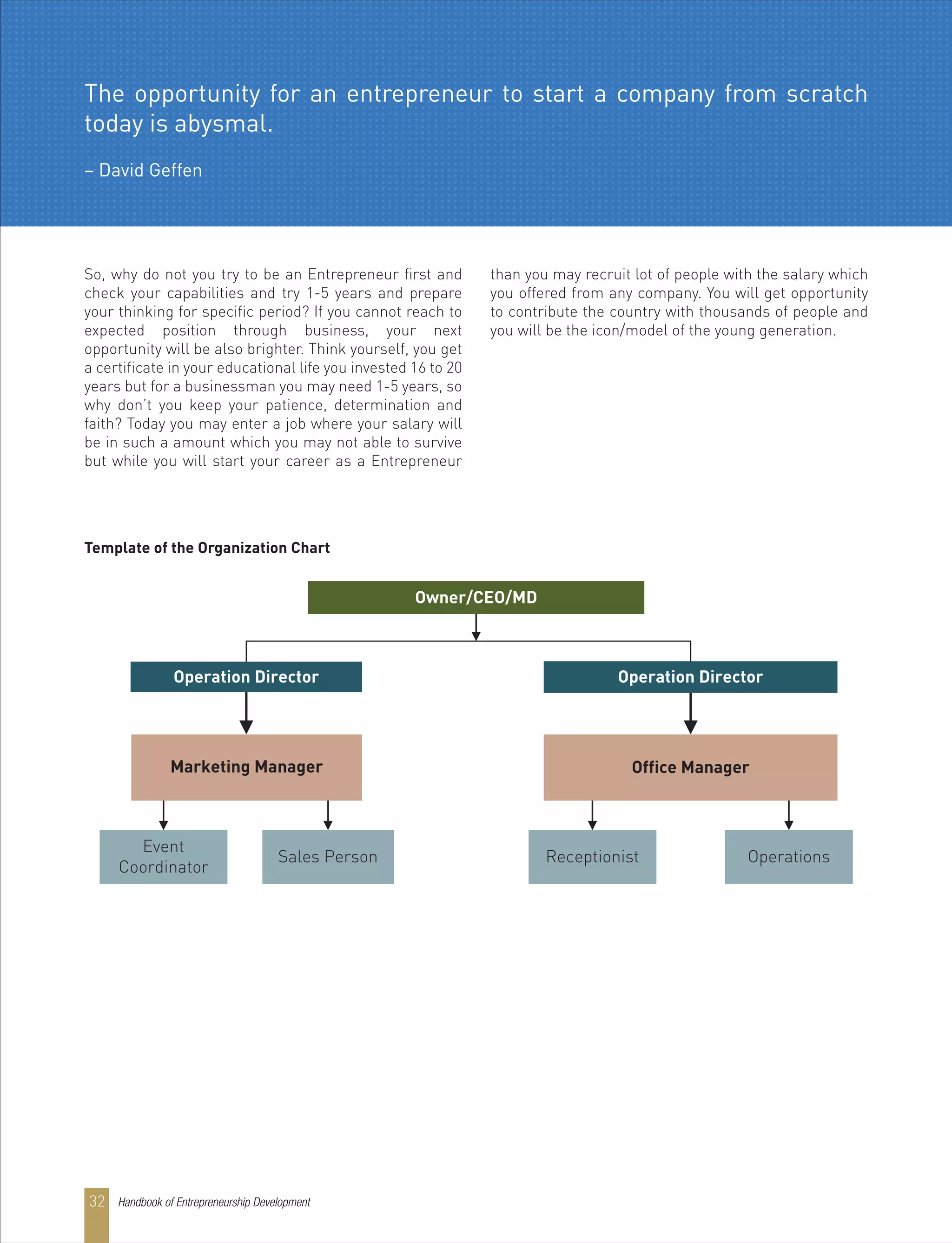

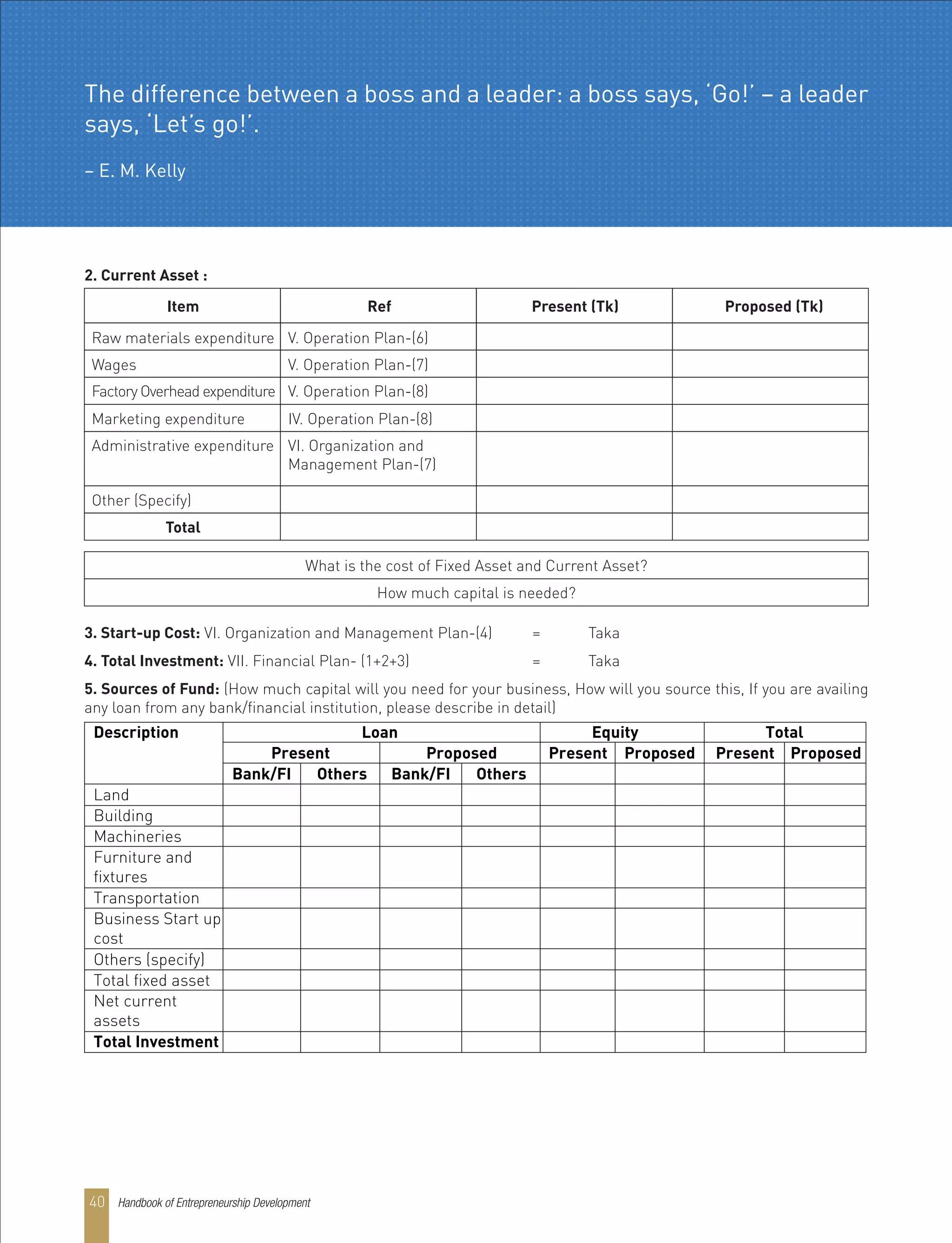

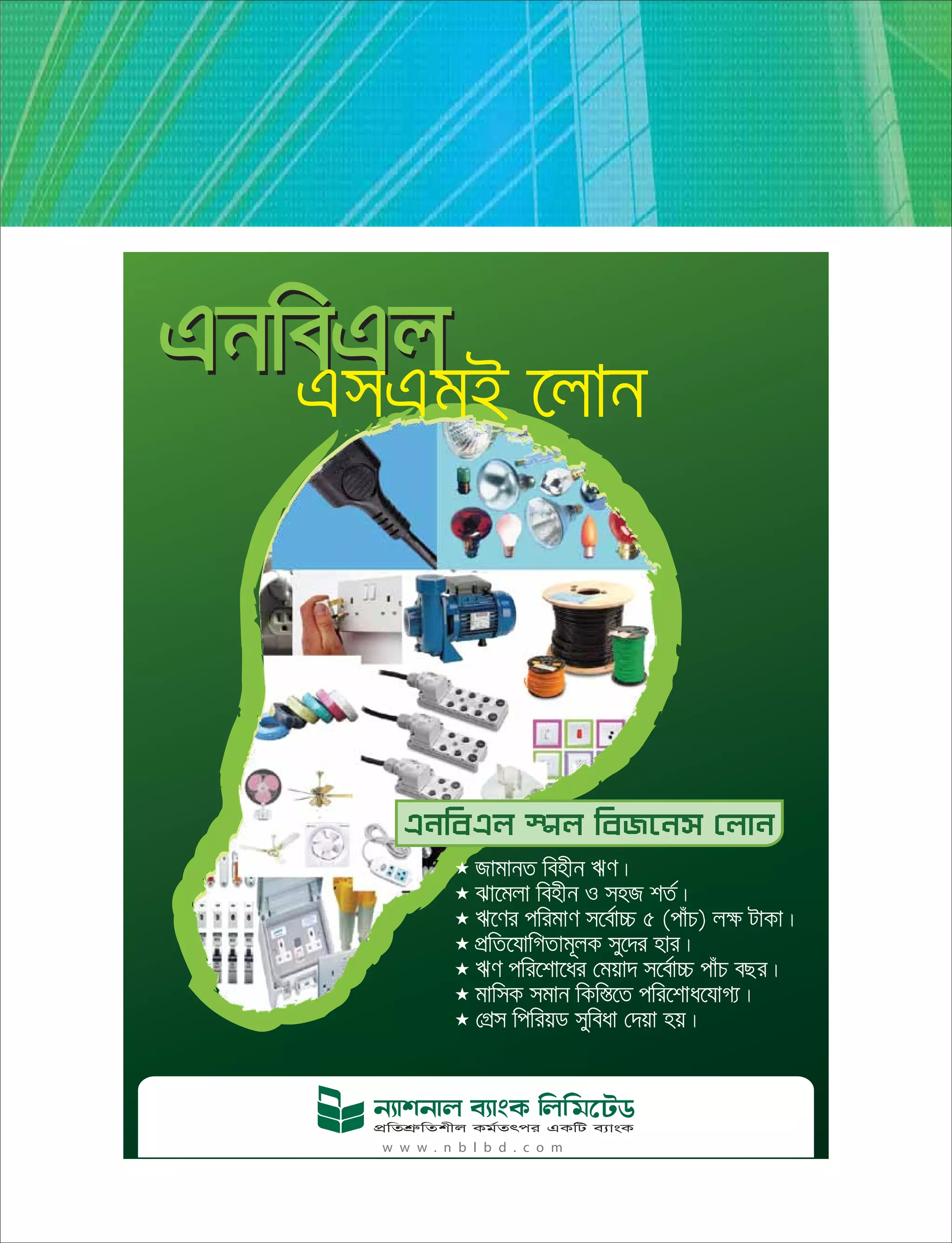

![club (for partnership business)

31. Resolution of partners for Credit taking

Financial institutions need the documents to

verify/understand/ evaluate the following in general:

1. The existence of the company/business,its

directors/business owners and the power to borrow and

legality of borrowing

2. The business operations risks and management

depth, experience and expertise of the owners and key

management team

3. The business operations risks and management

depth, experience and expertise of the owners and key

management team

4. The financial strength and repayment capability

(including the cash flow) of the borrower

5. The business net worth and gearing of borrower

6. The operating risks of the business

7. The strategies/contingency plans of the borrower to

mitigate such risks and maximise profitability

8. The proposed facilities are in line with the borrowing

needs

9. The amount applied for reflects the requirements of

the business based on existing or projected turnover

10. The overall risk associated with the proposed

borrowing

You should make full disclosure of all financial

information about yourself and ensure that it is accurate

at the time of your application. Declaration of the

correct information will also ensure that your Credit

application will be processed in a timely manner. Most

Financial Institutions have an application checklist that

lists out the documents required. You should ask the

financial institution for their checklist.

Visit and Interview by Financial Institutions

To understand the business and for the purpose of

clarification, financial institutions may carry out

interviews as well as conduct a site visit to your business

premises. This is to enable the financial institution to

verify and assess your financial position better. The

questions posed during the interview session and site

visit relates to the nature of business, management

structure, market positioning i.e. market share,

competitors, market outlook, future plans.

STAGE 3: ASSESSMENT OF THE CREDIT APPLICATION

After you have submitted all the required documents,

the financial institution will assess your Credit

application. You can refer to the client charter displayed

at the financial institution brochure , website to find out

the duration needed by the financial institution to

process your application. In assessing your Credit

application, the financial institution

would look for certain basic requirements which are

summarised as follows:

1. The viability of your business

2. Whether the risks are acceptable based on the

lending guidelines of the financial institution

3. Whether your Credit is for business development

4. Your credit history with the financial institution

5. Your key management and business style i.e.

conservative, aggressive, prudent etc.

6. Your succession plan, age and health

7. Sources of capital e.g. from the shareholders of the

business

8. Sufficiency of your financial commitment in the

business (in the form of shareholders' funds, directors'

advances and third party collateral provided by the

owners themselves) [You should ensure that you put in

adequate capital to support your business and not rely

solely on bank Credits. This is to ensure that your

business has the capacity to absorb any adverse shock

to its performance.]

9. Your capacity or ability of the business to repay the

Credit considering Primarily from the generation of

sufficient cashflow i.e. cash received less cash

disbursed for expenses incurred is adequate to service

the Credit. (Profits cannot be relied upon to service nor

repay Credits as it is a derived figure at the end of a

period) and Other sources of repayment. The

repayment programme will be structured in a manner

that will not impose undue strain on the business.

10. Security offered by you to compensate/mitigate

weaknesses.

Financial institutions do conduct credit checks and

study the conduct of the business current accounts,

repayment records of their Credits and trade facilities.

Some financial institutions have already put in place

their Credit evaluation matrix in the form of scores as

part of their credit evaluation processes.

Success is how high you bounce after you hit bottom.

– General George Patton

Handbook of Entrepreneurship Development46](https://image.slidesharecdn.com/handbookofentrepreneurshipdevelopment-161028042425/75/Handbook-of-Entrepreneurship-Development-by-DCCI-48-2048.jpg)

![Dhaka Chamber of Commerce & Industry FORUM

Welcome, Guest. Please login of register.

Forever Login

Search

News:

SMF - Just Installed!Login with username, password and session length

Dhaka Chamber of Commerce & Industry FORUM

Pages: [1]

Help Search Login Register

Subject / Started by Replies / Views Last post

Home

DCCI Help Desk and US Services and Products Center inaugurated 0 Replies

Started by rabbi 65 Views

JETRO Bangladesh Chief called on DCCI President 0 Replies

Started by rabbi 38 Views

MoU signing ceremony between DCCI and BASIS 0 Replies

Started by rabbi 32 Views

Bangladeshi Ambassador to Kuwait Call on DCCI President 0 Replies

Started by rabbi 31 Views

MoU signing ceremony between JCI and DCCI 0 Replies

Started by rabbi 26 Views

Discussion Meeting between DVCCI and Indian Delegation 0 Replies

Started by rabbi 30 Views

Discussion Meeting on Foreign Trade Investment: Opportunities and Challenges 0 Replies

Started by rabbi 27 Views

Discussion Meeting between DCCI and BCSIR 0 Replies

Started by rabbi 28 Views

High Commissioner of Nigeria called on DCCI President 0 Replies

Started by rabbi 26 Views

DCCI condemned attack incident which was held on A K Azad 0 Replies

Started by rabbi 34 Views

DCCI conducts motivational workshop at NSU to develop new entrepreneurs 0 Replies

Started by rabbi 32 Views

UGC Chairman acknowledges industry-academy dialogue for need-based ICT 0 Replies

Started by rabbi 27 Views

DCCI Publishes Tax Guide 2013-14 0 Replies

Started by rabbi 23 Views

Russia keen to invest in chemical and communication sector 0 Replies

Started by rabbi 21 Views

DCCI holds meeting with Association of Bankers, Bangladesh 0 Replies

Started by rabbi 20 Views

DCCI signs MoU with BD Venture Ltd. to promote 2000 entrepreneurs 0 Replies

Started by rabbi 20 Views

DCCI President urges Pakistan to invest in Bangladesh 0 Replies

Started by rabbi 22 Views

DCCI & BASIS organize workshop for 200 IT freelancers to make them entrepreneur 0 Replies

Started by rabbi 21 Views

Dutch trade delegation interested to work on development of water management 0 Replies

Started by rabbi 20 Views

Rotary International (D-3281) and BIID to provide 200 entrepreneurs 0 Replies

Started by rabbi 23 Views

DCCI Business Institute and Daffodil International University (DIU) signed MoU 0 Replies

Started by rabbi

September 03, 2013,

11:35:22 AM

by rabbi

September 03, 2013,

11:34:49 AM

by rabbi

September 03, 2013,

11:34:30 AM

by rabbi

September 03, 2013,

11:33:55 AM

by rabbi

September 03, 2013,

11:33:07 AM

by rabbi

September 03, 2013,

11:32:42 AM

by rabbi

September 03, 2013,

11:32:17 AM

by rabbi

September 03, 2013,

11:31:52 AM

by rabbi

September 03, 2013,

11:31:18 AM

by rabbi

September 03, 2013,

11:30:47 AM

by rabbi

September 03, 2013,

11:30:18 AM

by rabbi

September 03, 2013,

03:09:36 PM

by rabbi

September 25, 2013,

03:09:06 PM

by rabbi

September 25, 2013,

03:08:30 PM

by rabbi

September 25, 2013,

03:08:00 PM

by rabbi

September 25, 2013,

03:07:21 PM

by rabbi

September 25, 2013,

03:06:49 PM

by rabbi

September 25, 2013,

03:04:54 PM

by rabbi

September 25, 2013,

03:04:06 PM

by rabbi

September 25, 2013,

03:03:27 PM

by rabbi

September 25, 2013,

03:02:25 PM

by rabbi

Handbook of Entrepreneurship Development 81](https://image.slidesharecdn.com/handbookofentrepreneurshipdevelopment-161028042425/75/Handbook-of-Entrepreneurship-Development-by-DCCI-83-2048.jpg)

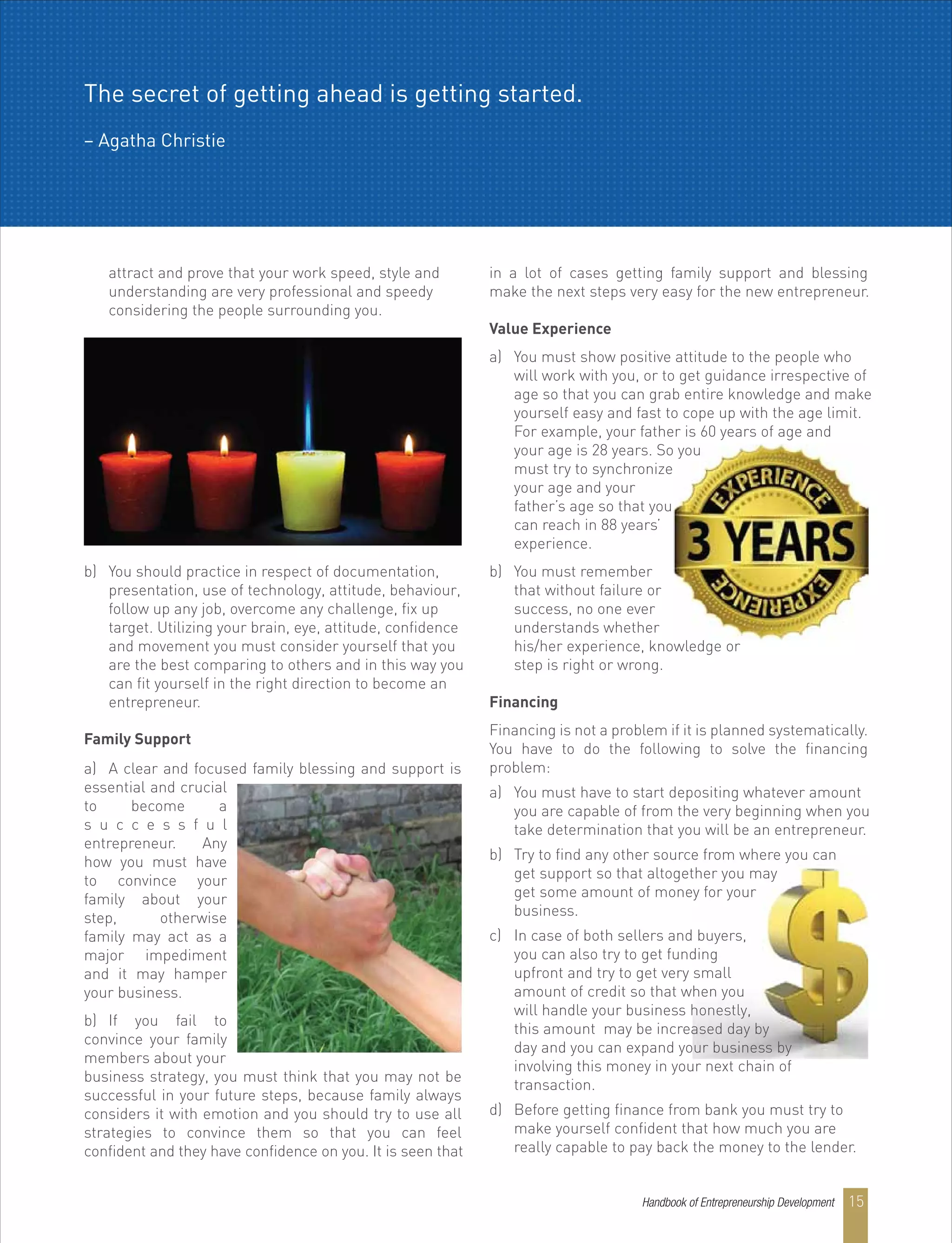

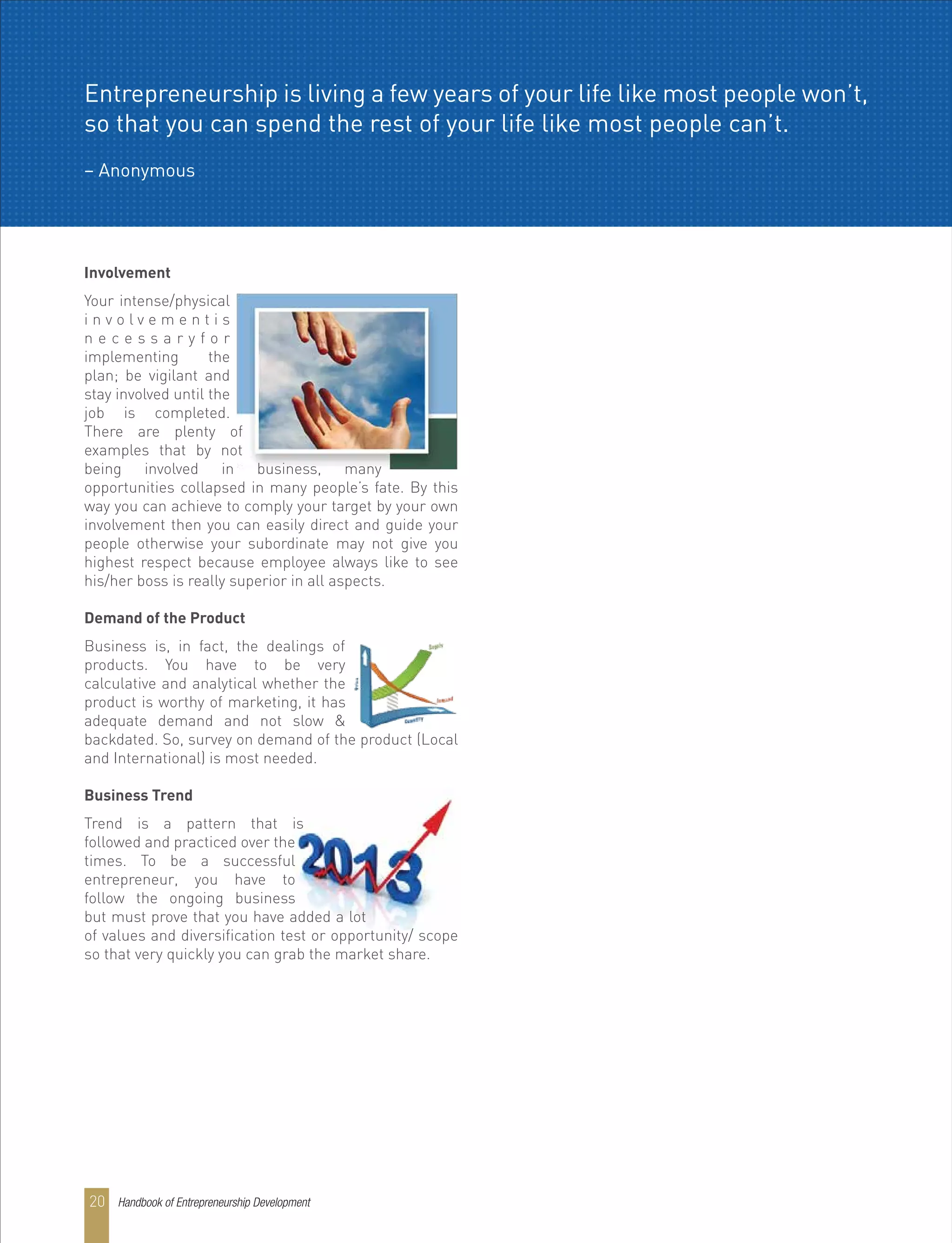

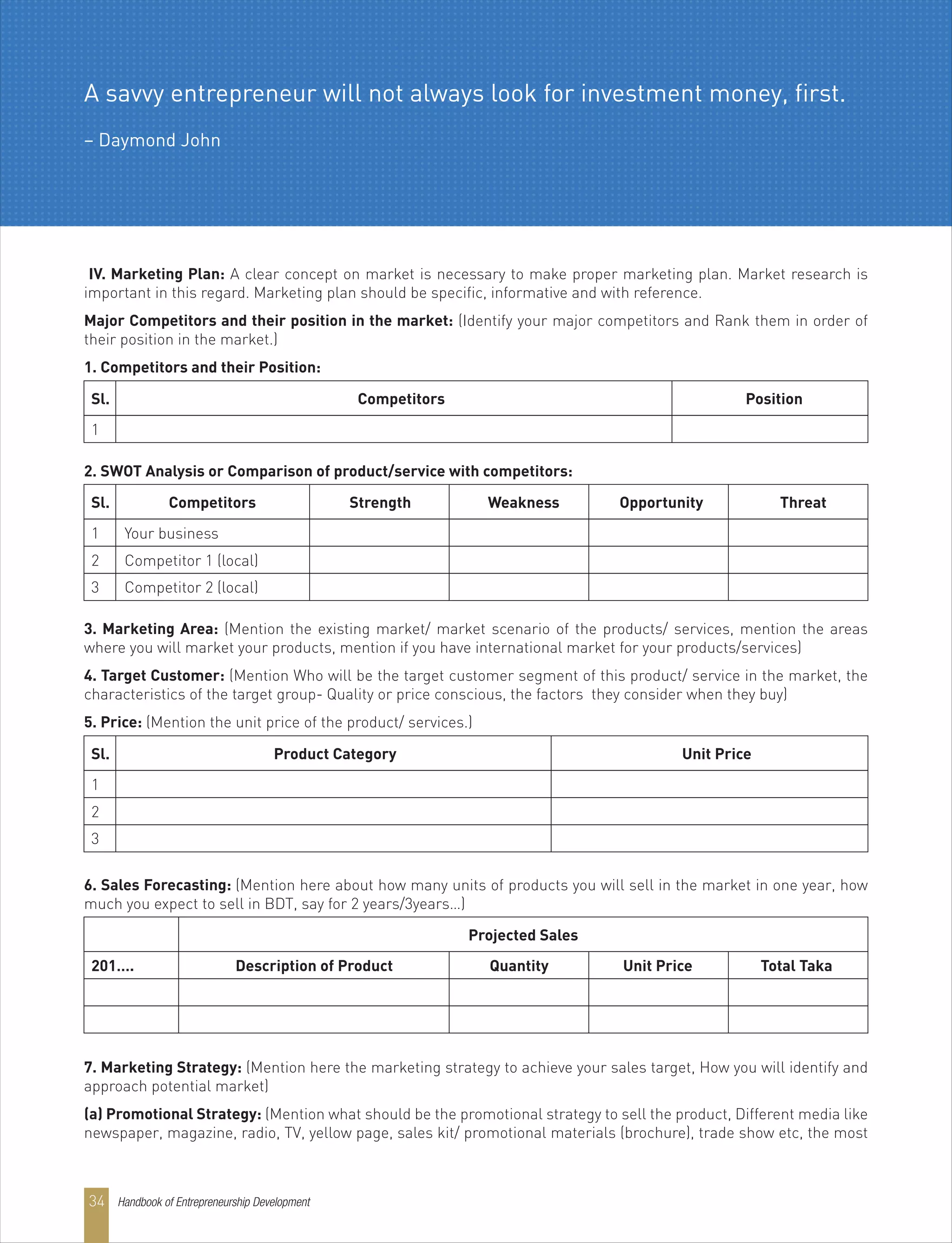

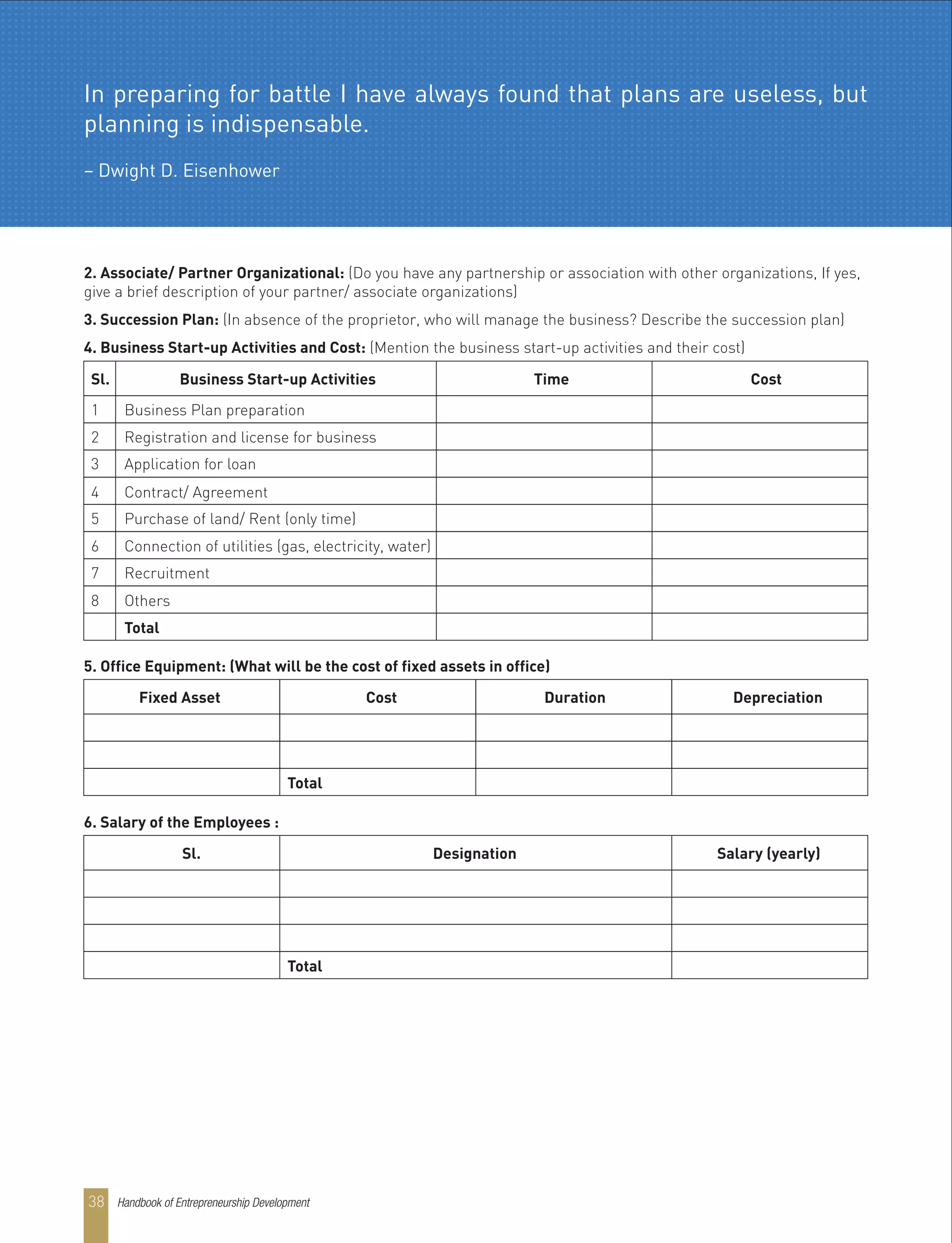

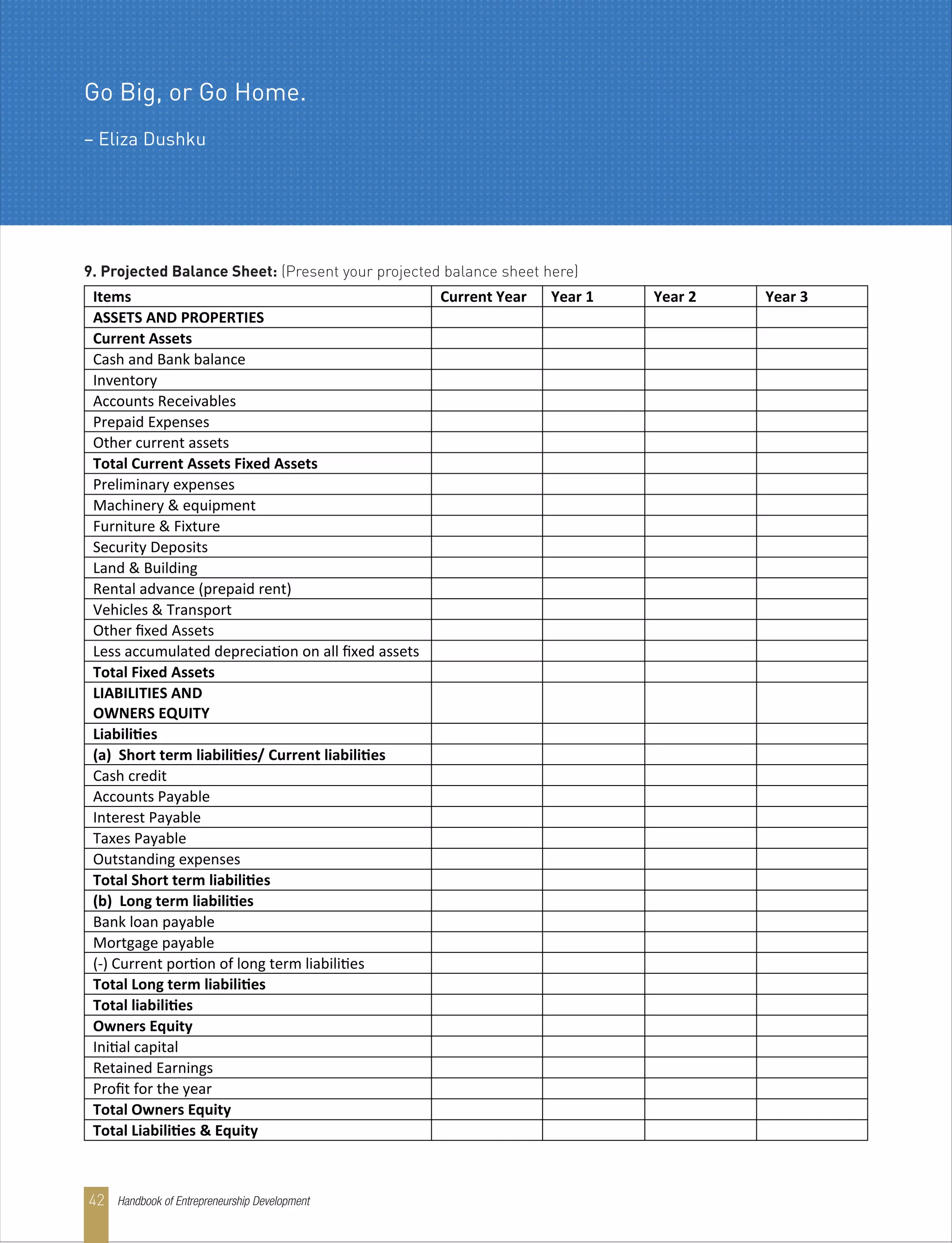

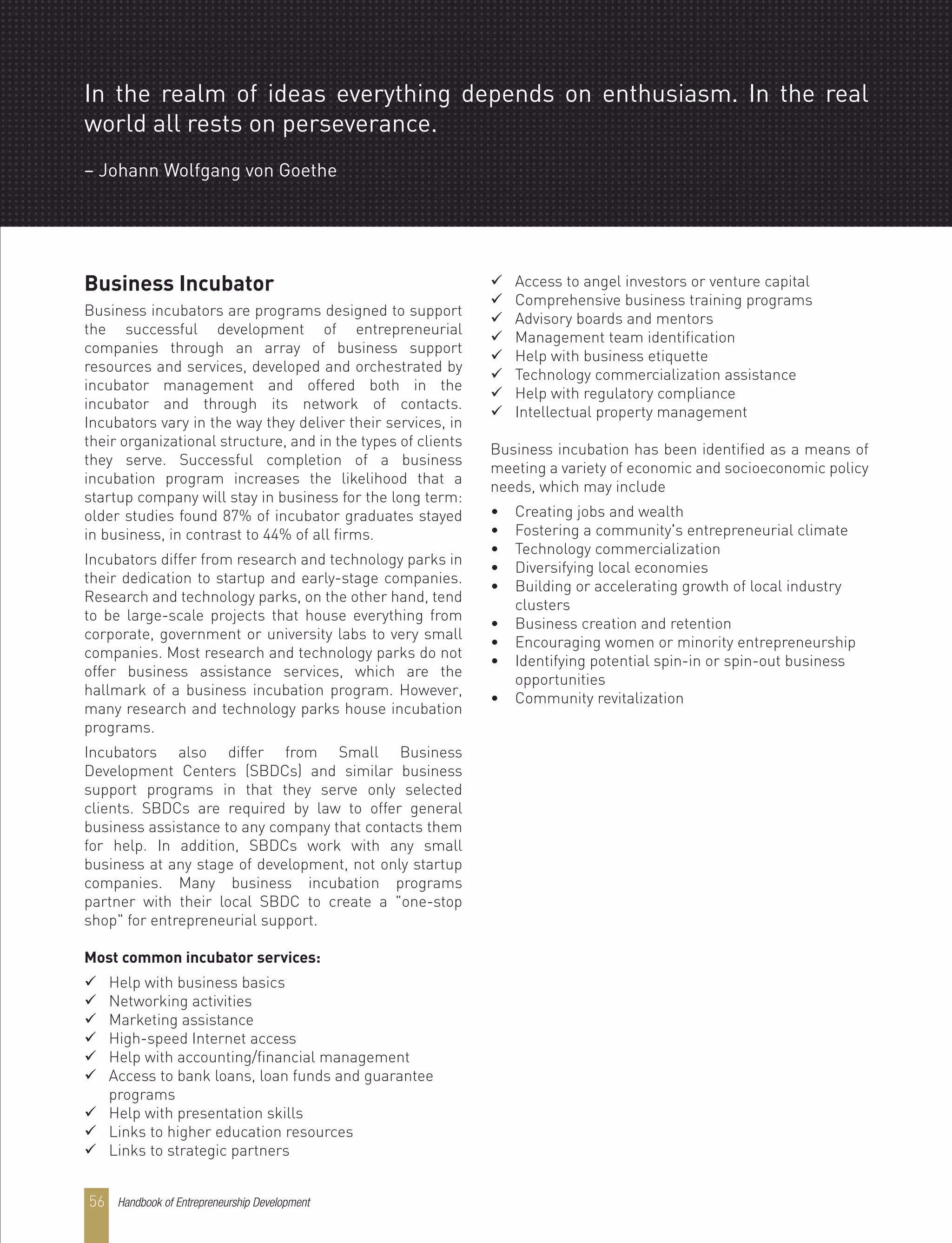

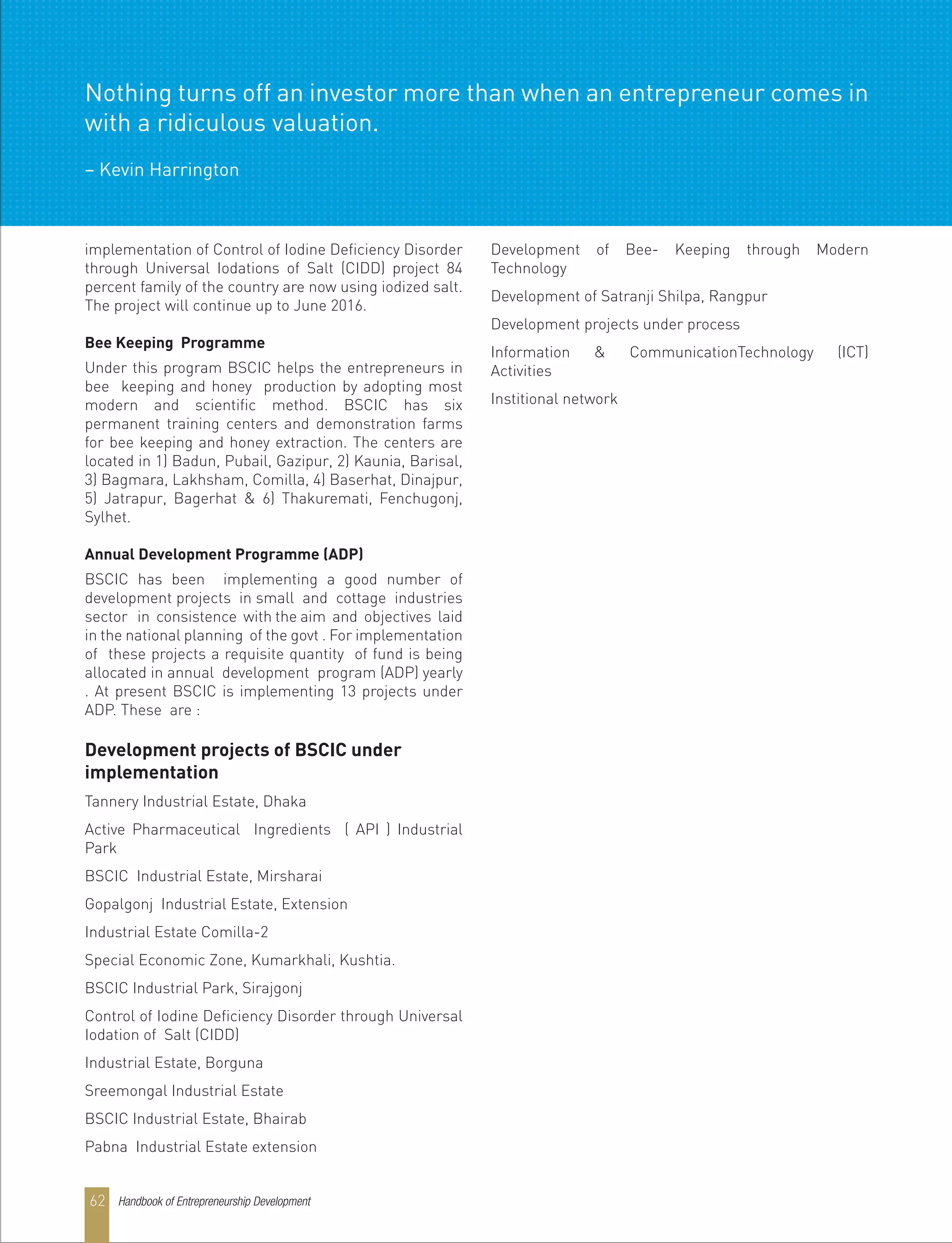

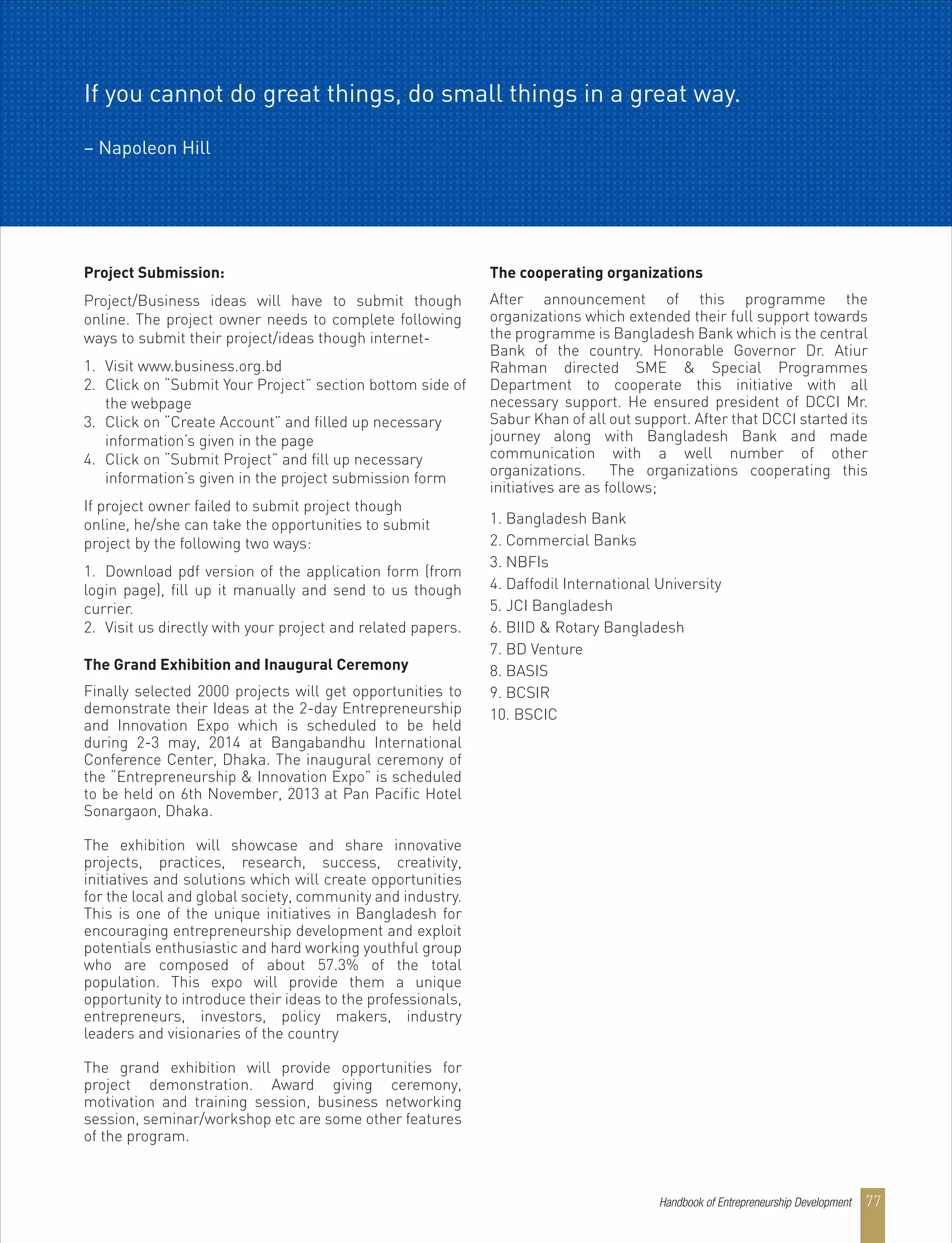

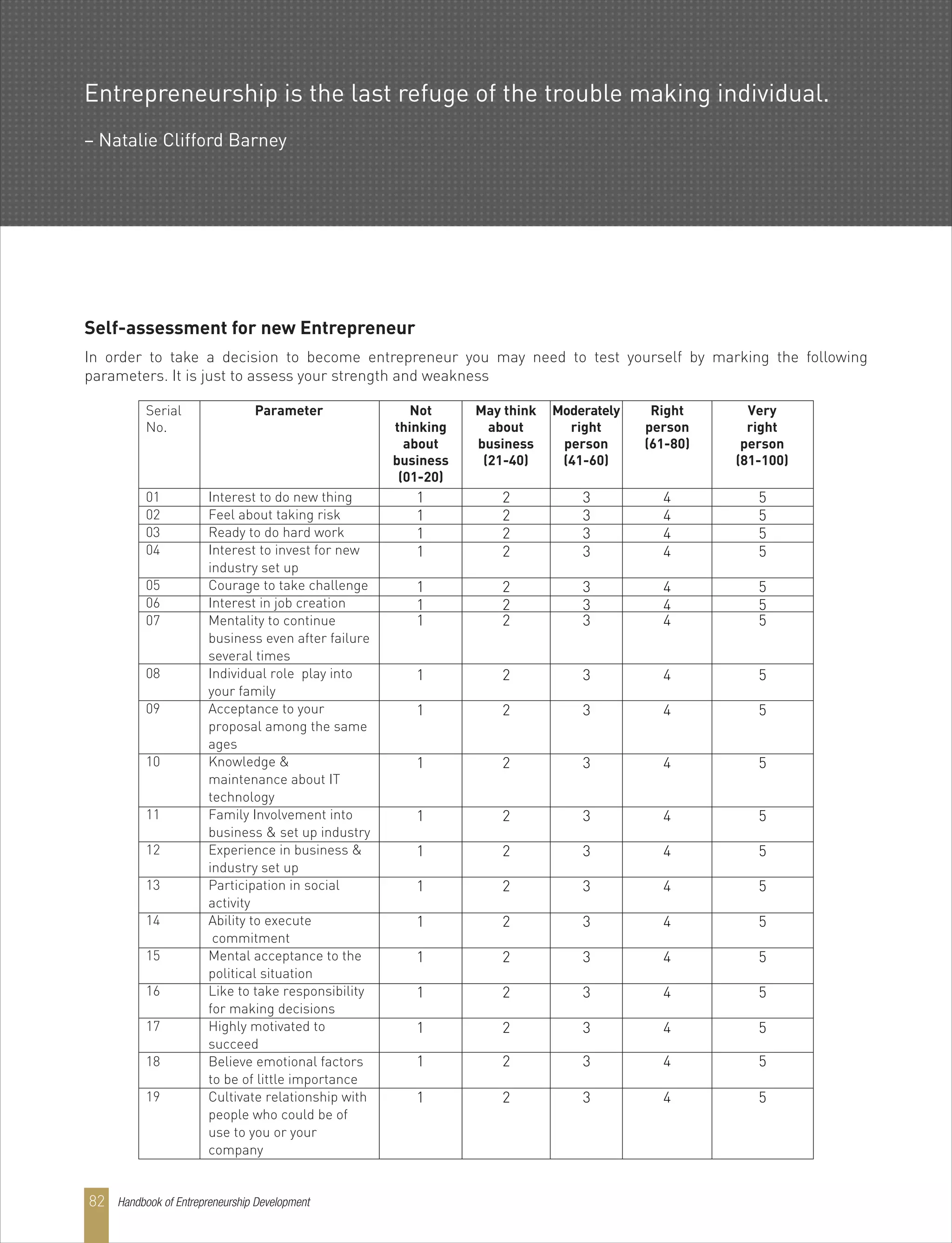

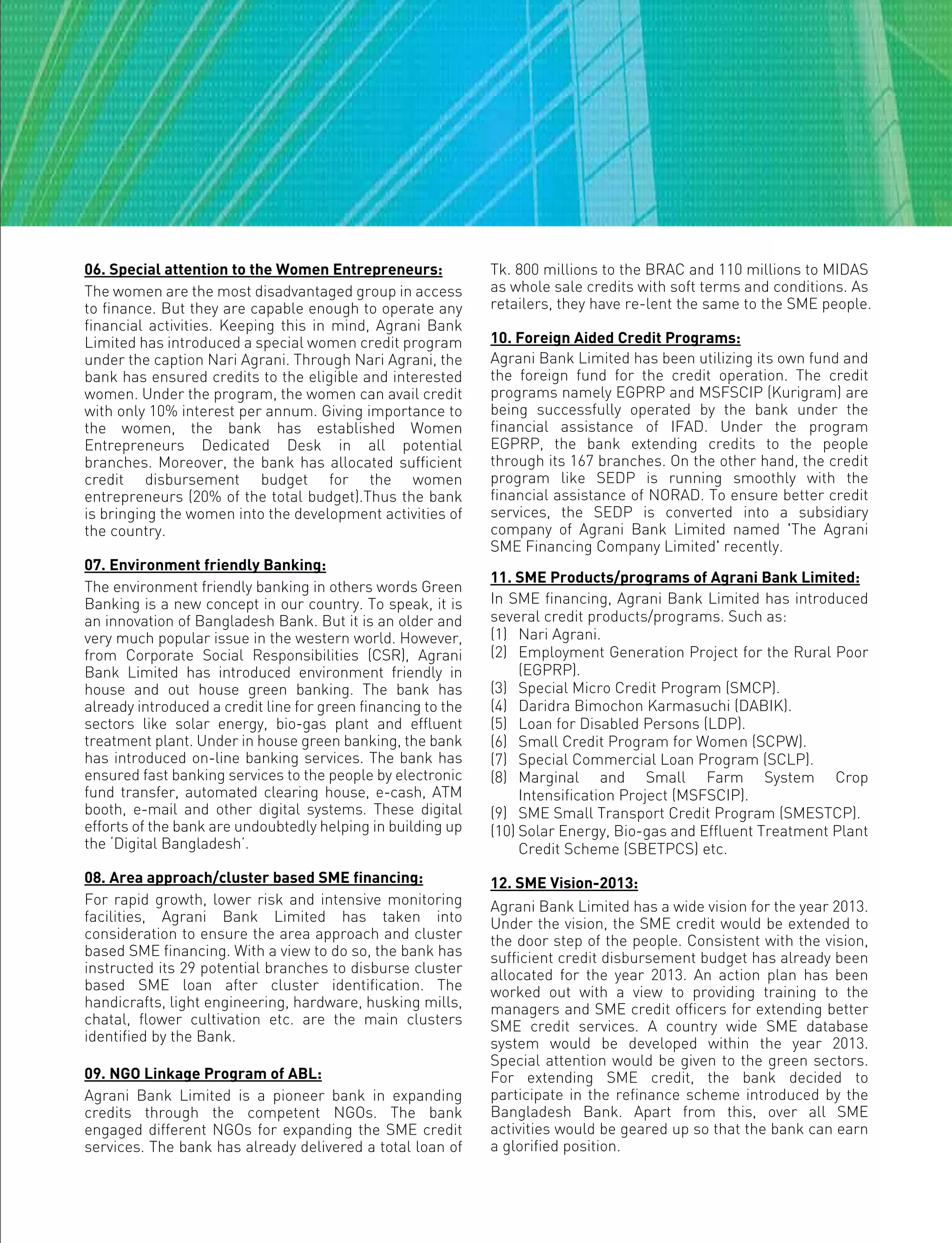

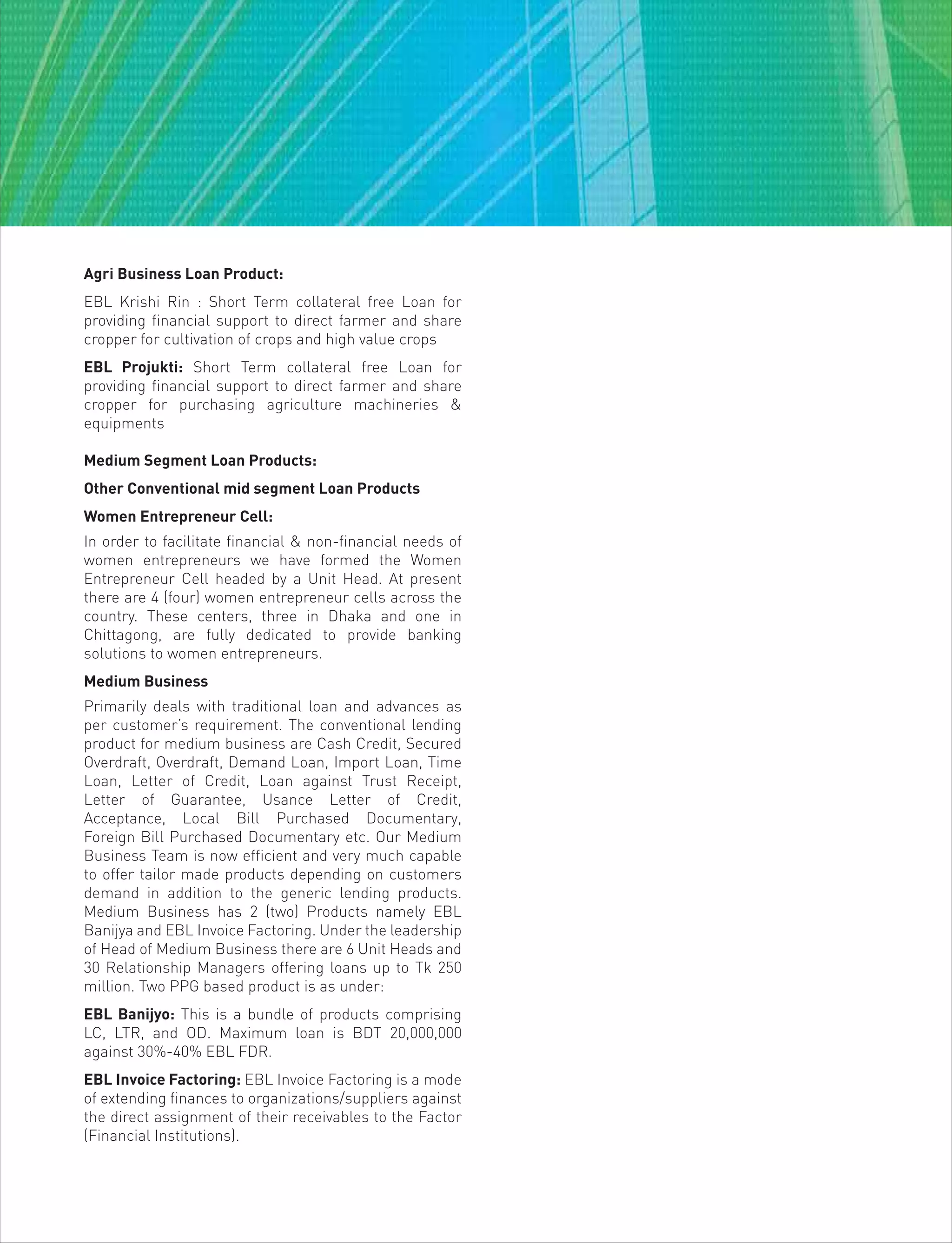

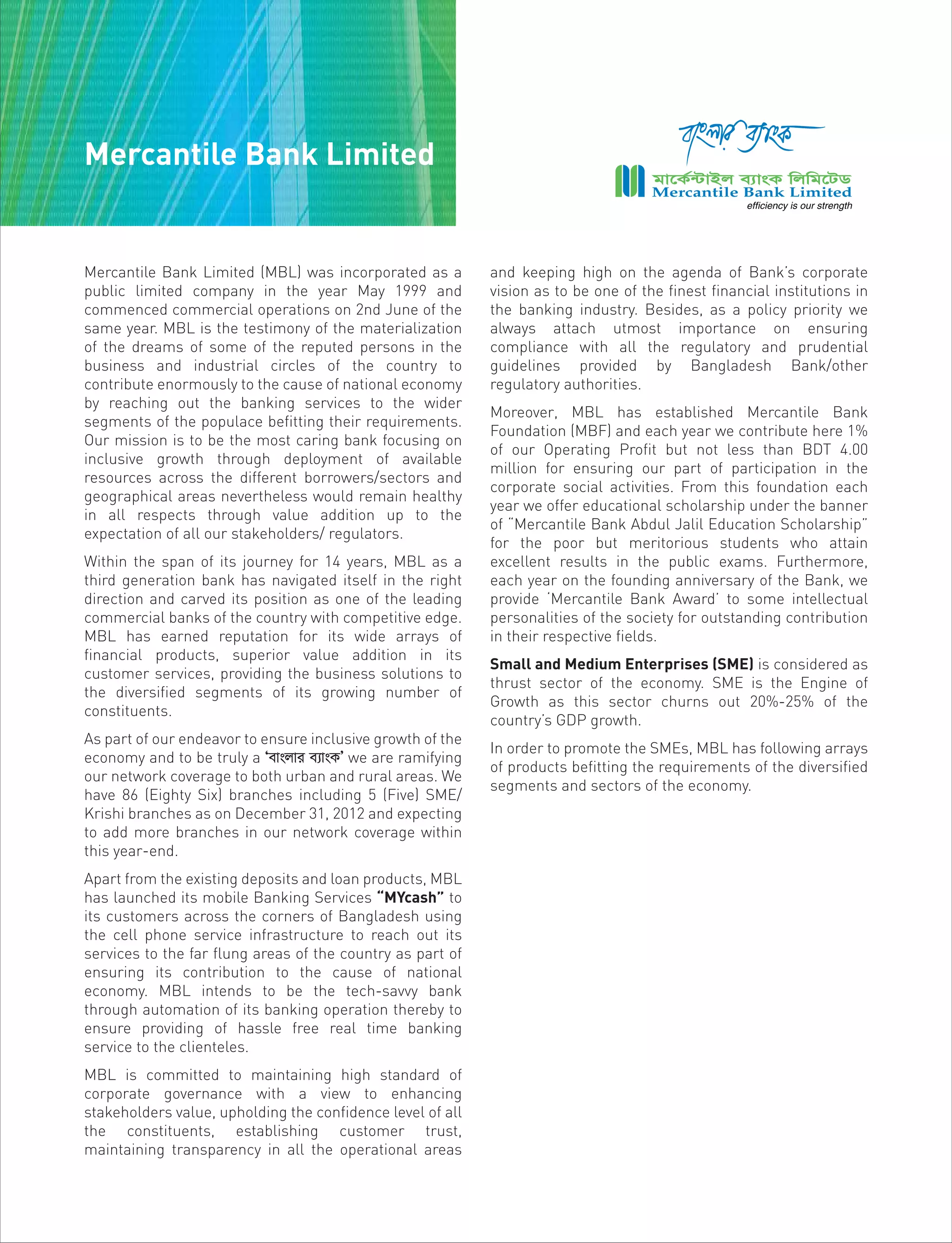

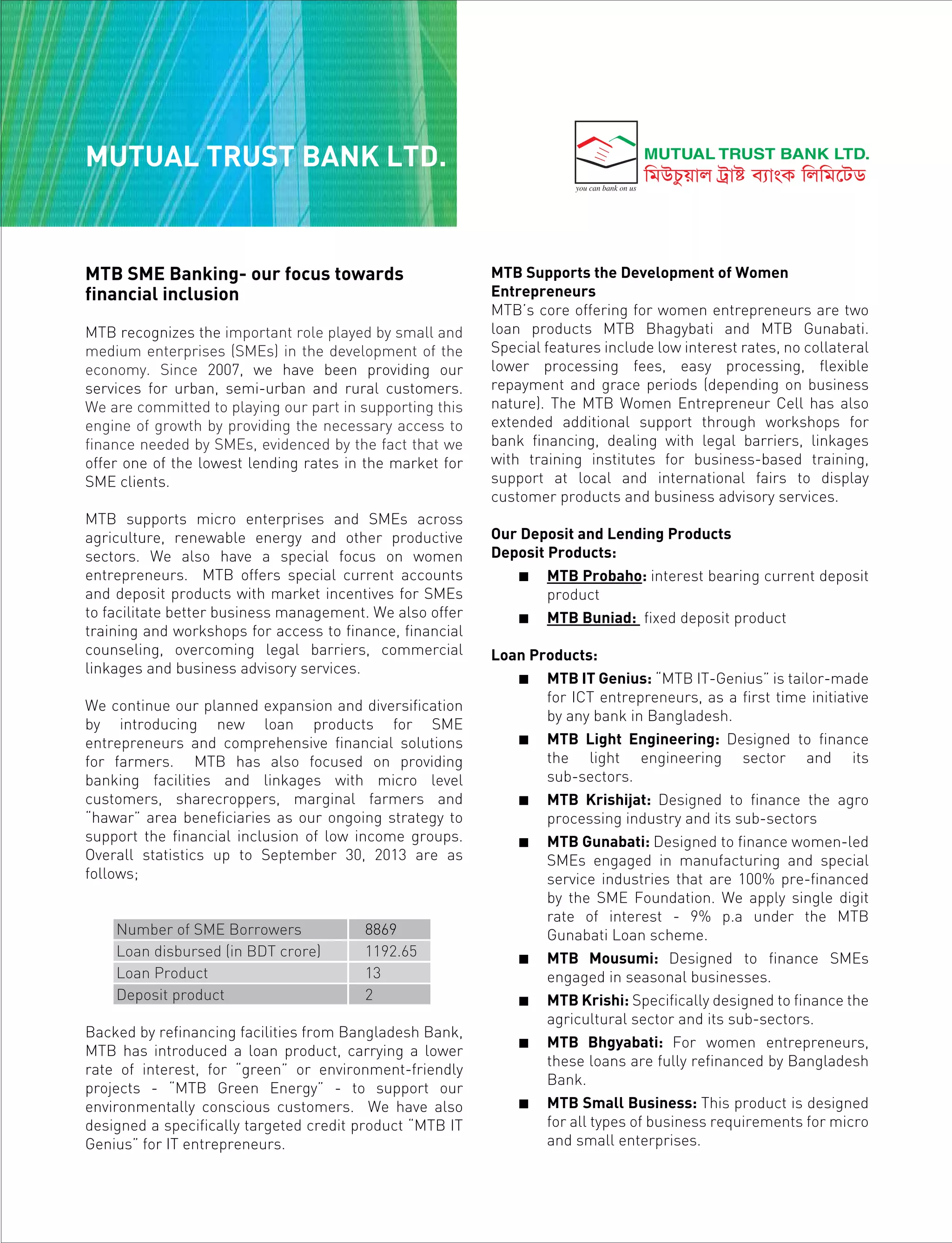

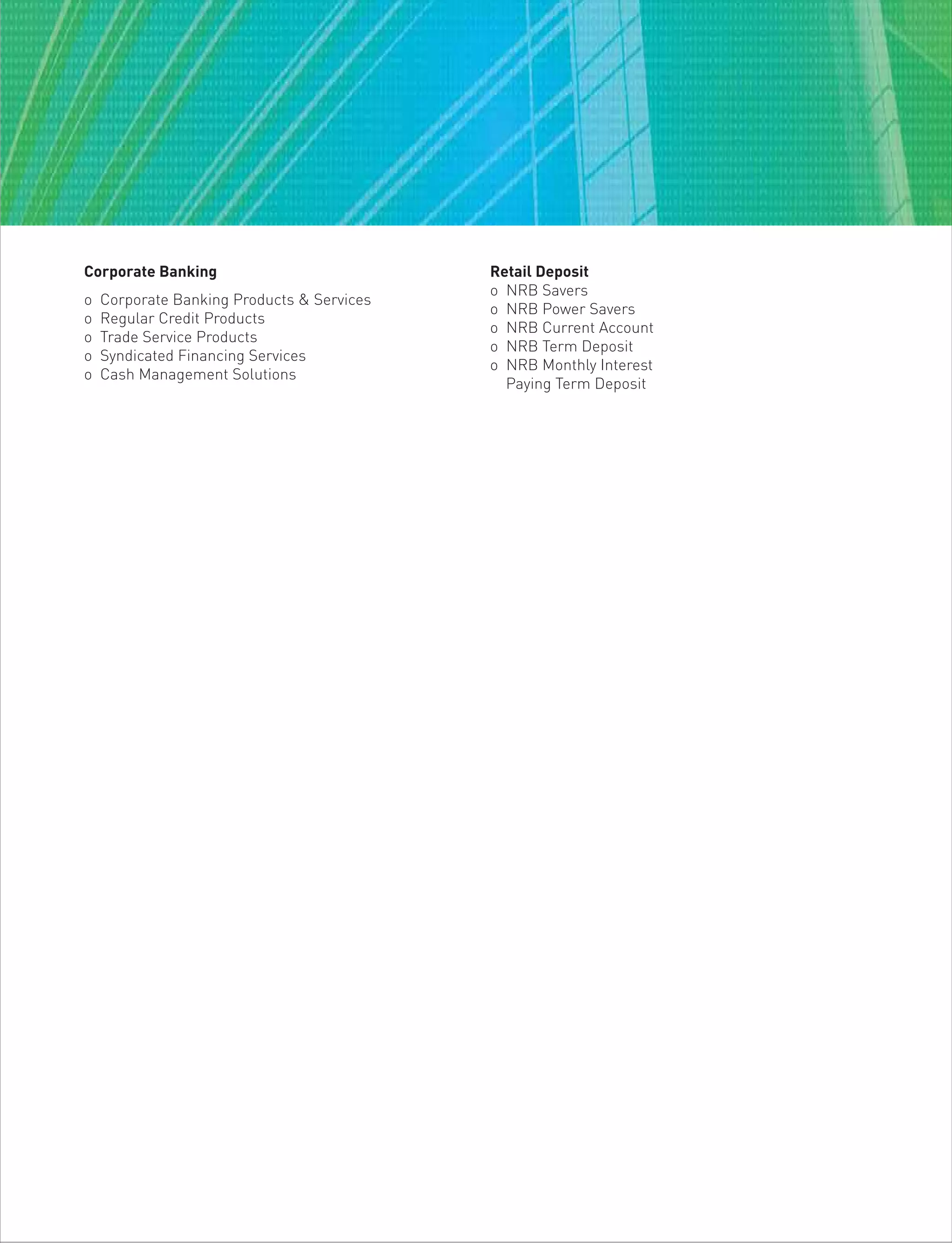

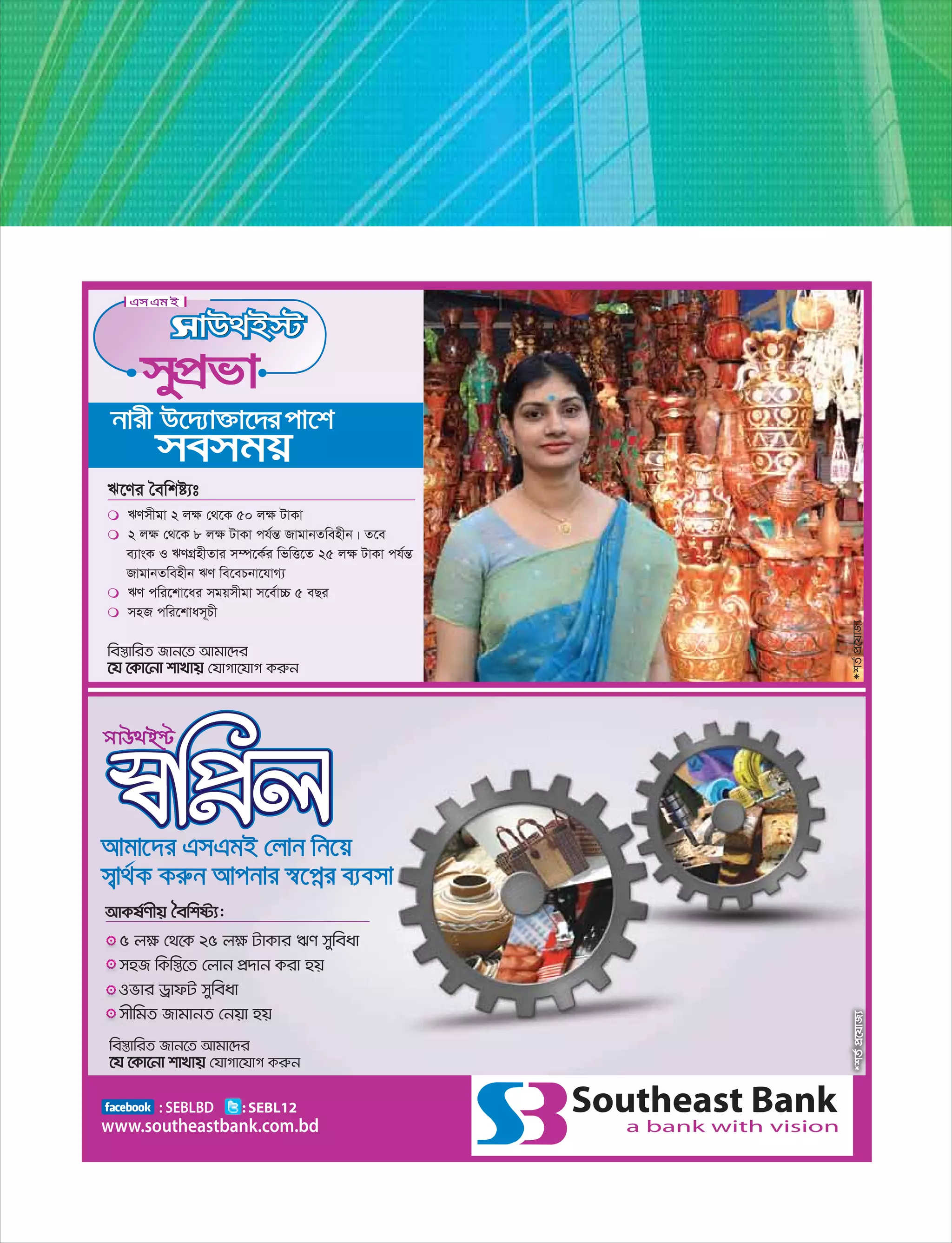

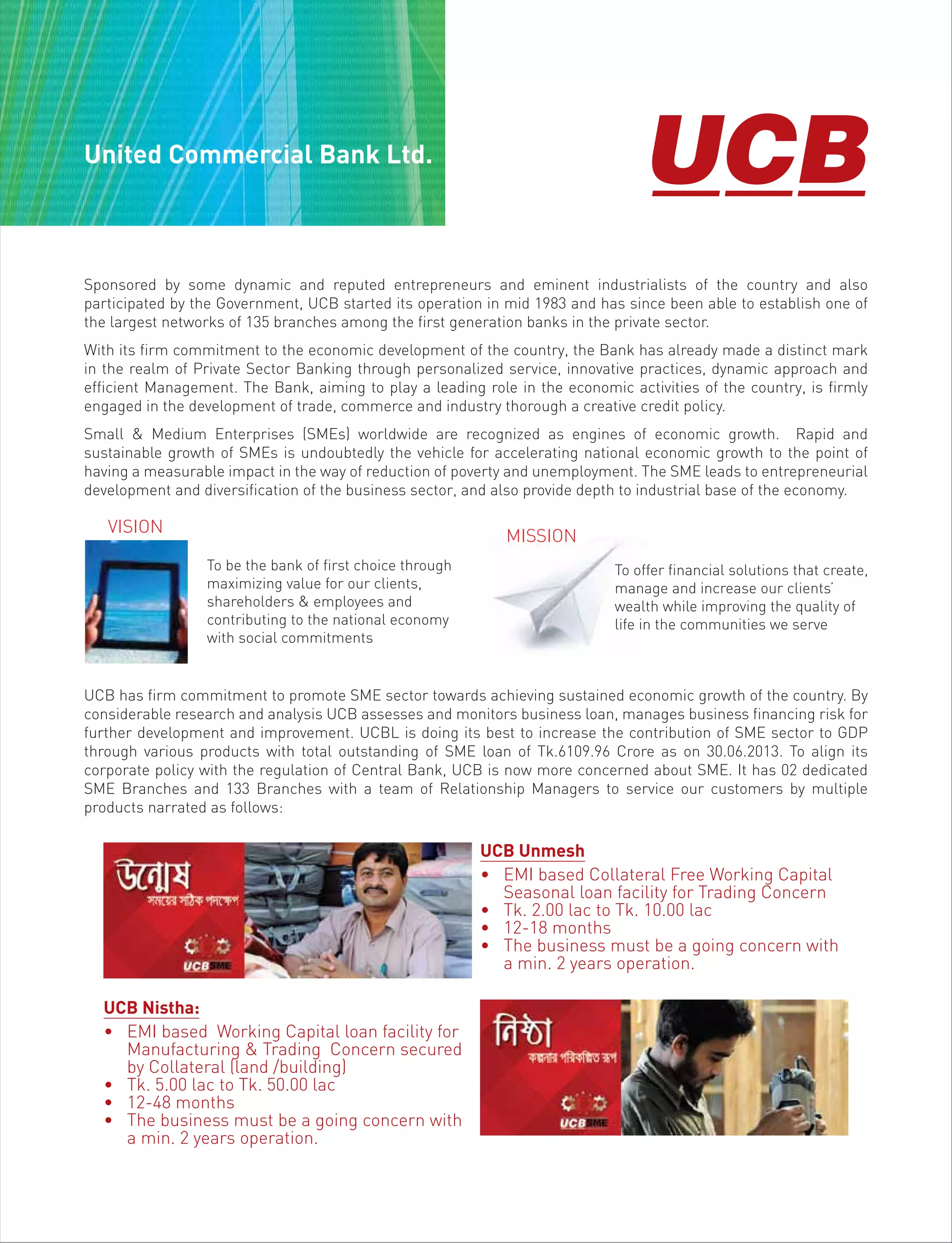

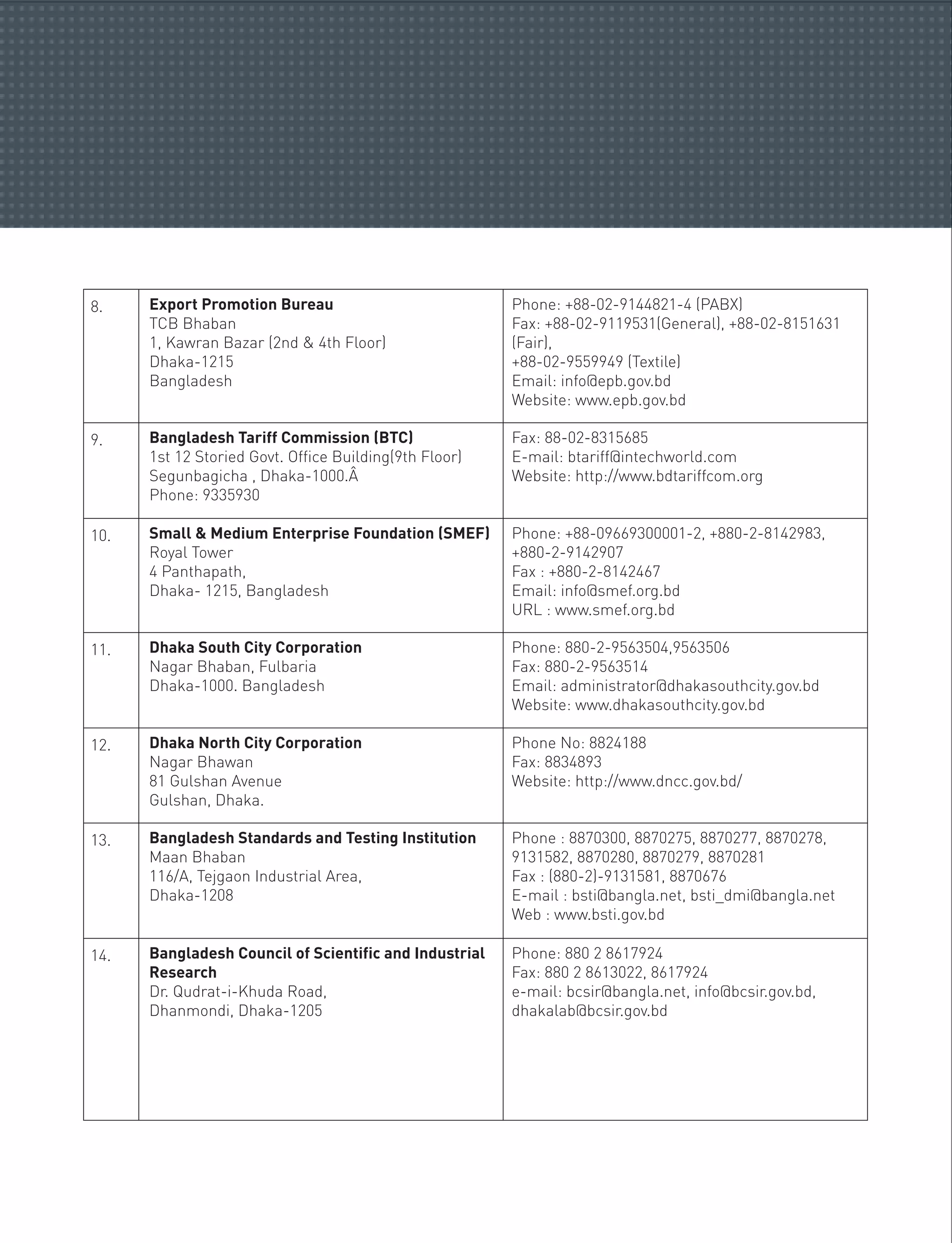

![Company Profile

National Finance Ltd (NFL) is incorporated as a Public

Limited Company under the Companies Act 1994 and

licensed by Bangladesh Bank under the Financial

Institutions Act 1993. The company was established with

the objective to create an institution that will cater to the

investment need of the economy.

The company started as a provider of lease finance for

acquiring assets for industrial and commercial use. As

the company grew, the products and services were

diversified to cater to the need of the growing customer

base. Besides Lease and Term Loan, NFL now offers a

number of other financial solutions i.e. Corporate

Finance, SME Finance, Consumer Finance, Auto Loan

and a wide range of working capital solution like Work

Order Finance, Factoring and Secured Overdraft facility.

NFL offers a wide range of deposit products like Fixed

Deposit, Monthly Income Scheme, Quarterly Earner

Scheme, NFL Double Delight, NFL Triple Crown, etc.

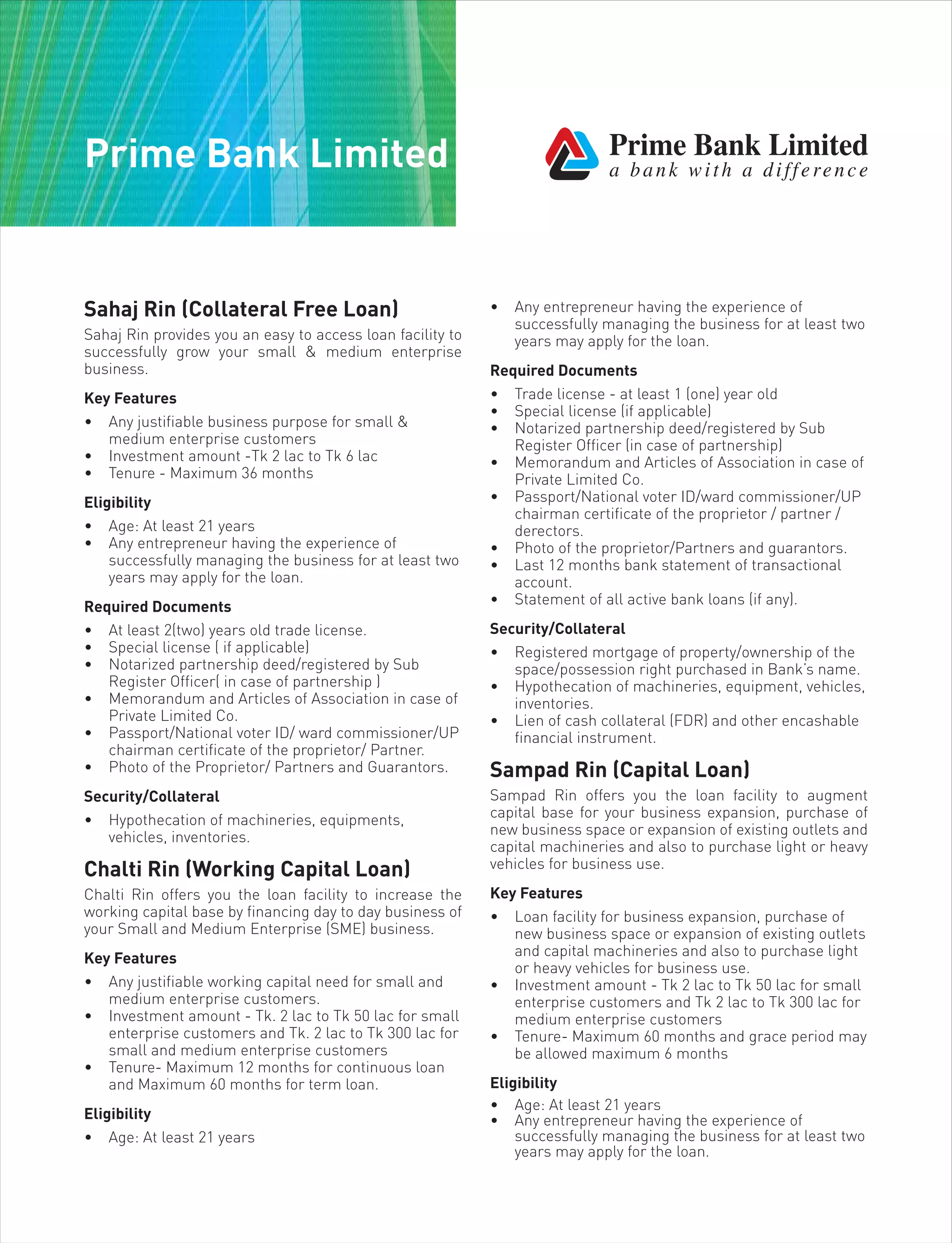

SME Finance

Loan Features:

1. Loan amount: Tk. 200,000/- to Tk. 5,000,000/-

2. Nature of Business: Manufacturer, Service Provider,

Business

3. Legal Formation: Proprietorship, Partnership,

Private limited company

4. Experience: At least 2 years

5. Nationality: Bangladeshi by born

6. Loan Tenure:

a. Working capital: 1 year

b. Term Loan/Lease: 2 -5 years

7. Age of the sponsor:

a. Minimum: 21 years

b. Maximum: 60 years

8. Security:

a. Mortgage [in applicable case]

b. Third party personal guarantee(s) [including

spouse/family member]

c. Hypothecation [in applicable case]

9. Employment: No government employee is eligible for

finance.

Required Document:

1. Trade License [up to date]

2. TIN

3. VAT [in applicable case]

4. Certificate of Incorporation, Memorandum and

Articles of Association, Board Resolution [for private

limited company]

5. Registered partnership deed

6. Financial report [2 years]

7. Bank statement [1 year]

8. National ID/Passport [photocopy]

9. Net worth statement of the sponsor(s)

10.Passport size photo [2 copies]

11.Last month’s electricity/gas/telephone bill

[photocopy]

12.Rental deed of office/factory

13.Stock list

14.Bio data and 2 copies passport size photo of the third

party guarantor(s)

15.Permission from authorized Ministry/concern [in

applicable case]

Women Entrepreneur Finance

Loan Features:

1. Loan amount: Tk. 200,000/- to Tk. 5,000,000/-

2. Rate: 10%

3. Nature of Business: Manufacturer, Service Provider,

Business

4. Legal Formation: Proprietorship, Partnership,

Private limited company

5. Experience: At least 2 years

6. Nationality: Bangladeshi by born

7. Loan Tenure:

a. Working capital: 1 year

b. Term Loan/Lease: 2 -5 years

8. Age of the sponsor:

a. Minimum: 21 years

b. Maximum: 60 years

9. Security:

a. Mortgage (Mortgage free loan up to Tk. 2,500,000/-)

[in applicable case]

b. Third party personal guarantee(s) [including

spouse/family member]

c. Hypothecation [in applicable case]

10.Employment: No government employee is eligible for

finance.

National Finance Ltd](https://image.slidesharecdn.com/handbookofentrepreneurshipdevelopment-161028042425/75/Handbook-of-Entrepreneurship-Development-by-DCCI-136-2048.jpg)

![Required Document:

1. Trade License [up to date]

2. TIN

3. VAT [in applicable case]

4. Certificate of Incorporation, Memorandum and

Articles of Association, Board Resolution [for

private limited company]

5. Registered partnership deed

6. Financial report [2 years]

7. Bank statement [1 year]

8. National ID/Passport [photocopy]

9. Net worth statement of the sponsor(s)

10.Passport size photo [2 copies]

11.Last month’s electricity/gas/telephone bill

[photocopy]

12.Rental deed of office/factory

13.Stock list

14.Bio data and 2 copies passport size photo of the

third party guarantor(s)

15.Permission from authorized Ministry/concern [in

applicable case]](https://image.slidesharecdn.com/handbookofentrepreneurshipdevelopment-161028042425/75/Handbook-of-Entrepreneurship-Development-by-DCCI-137-2048.jpg)

This document discusses the importance of entrepreneurship development in Bangladesh. It notes that Bangladesh aims to become a middle-income country by 2021 in order to achieve rapid economic growth. However, Bangladesh currently faces a crisis of unemployment, especially among educated youth. The document argues that promoting entrepreneurship among youth is the easiest way to solve this problem and ensure more employment opportunities. It states that today's educated youth remain unemployed even after completing their studies and need to acquire skills to make a living. The unemployment of educated youth is a major issue in Bangladesh that needs to be addressed to avoid social crisis. The document maintains that Bangladeshi youth have the energy and boldness to take up the challenge of becoming successful entrepreneurs.