Downloaded 148 times

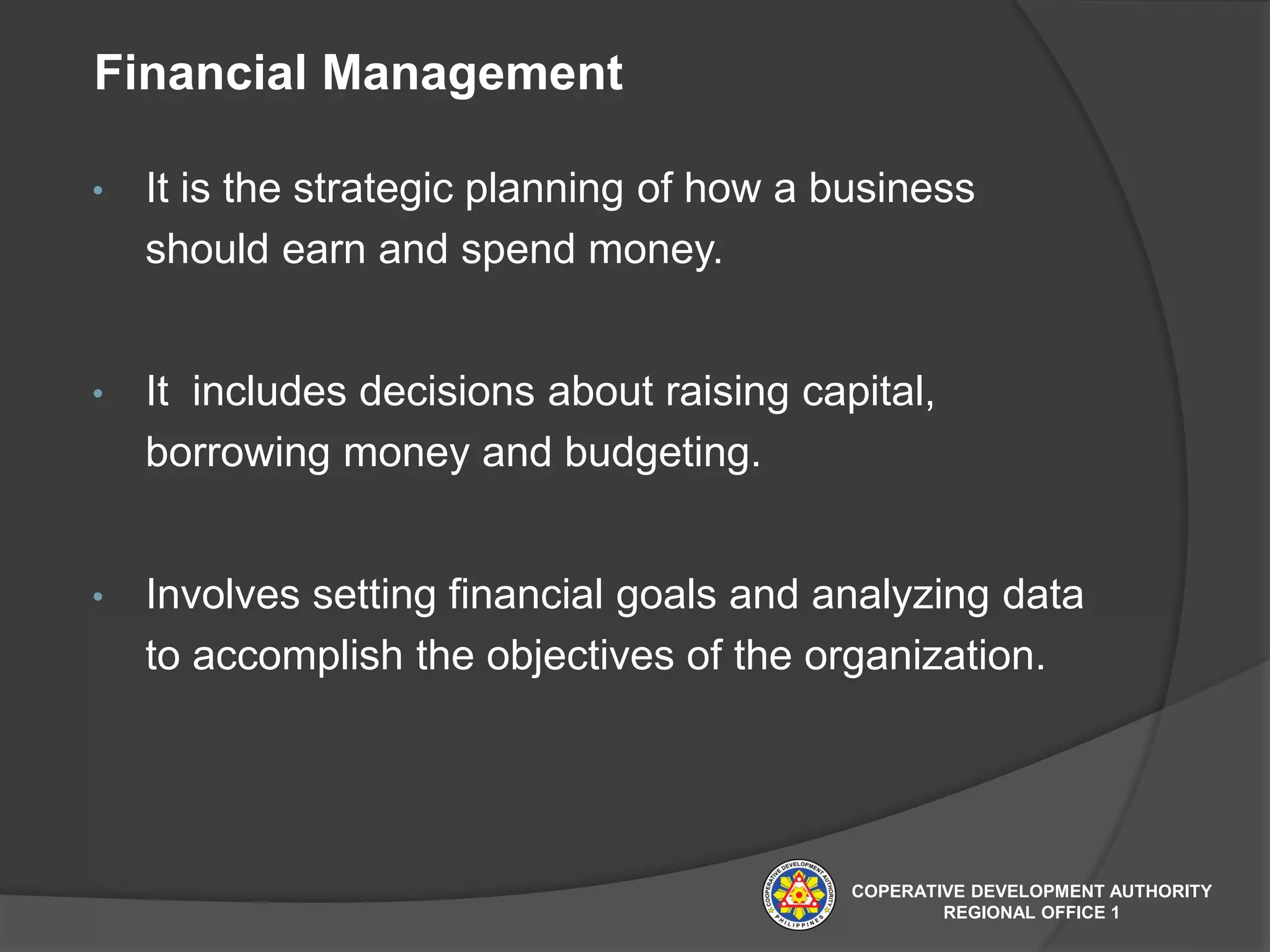

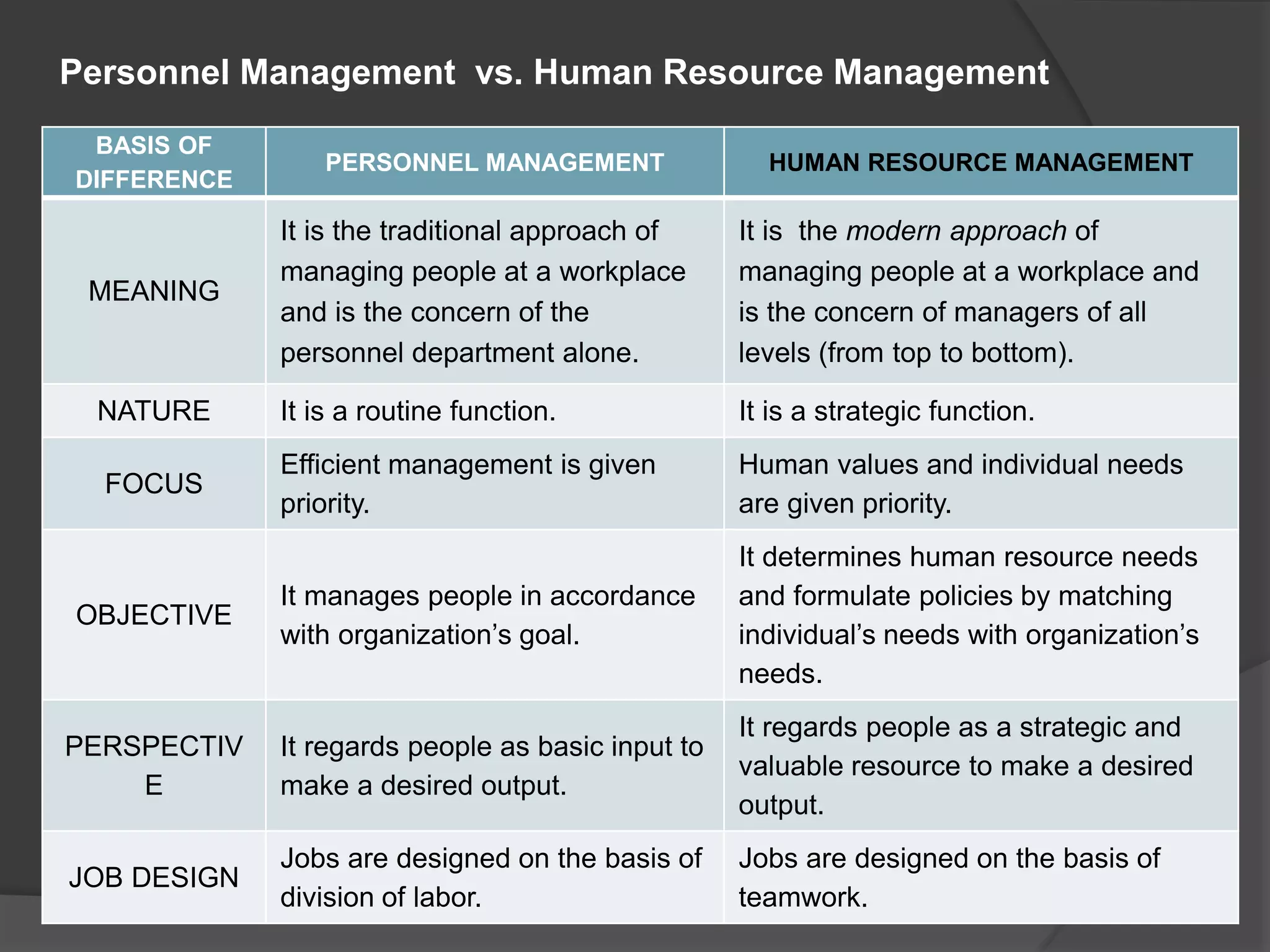

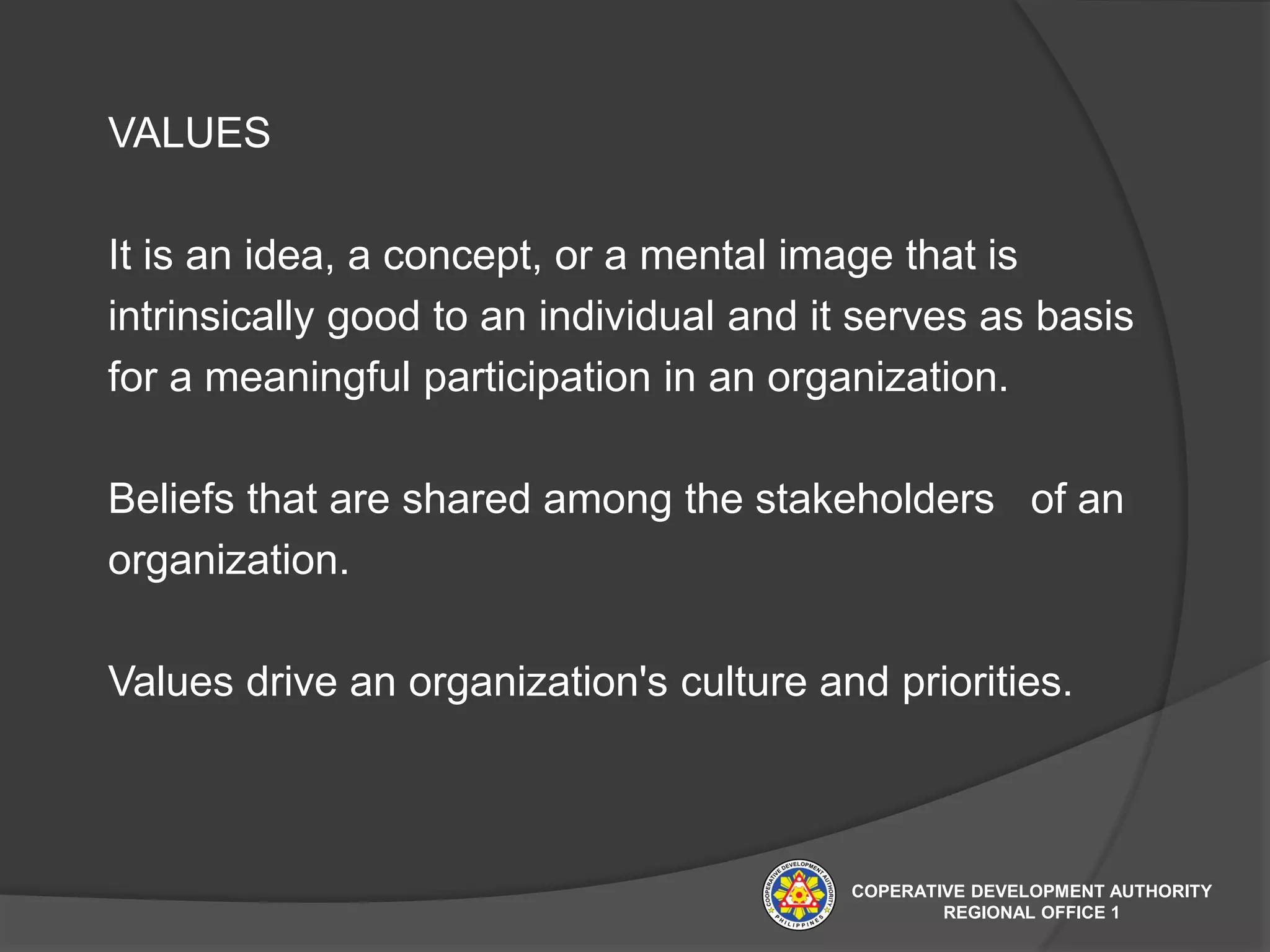

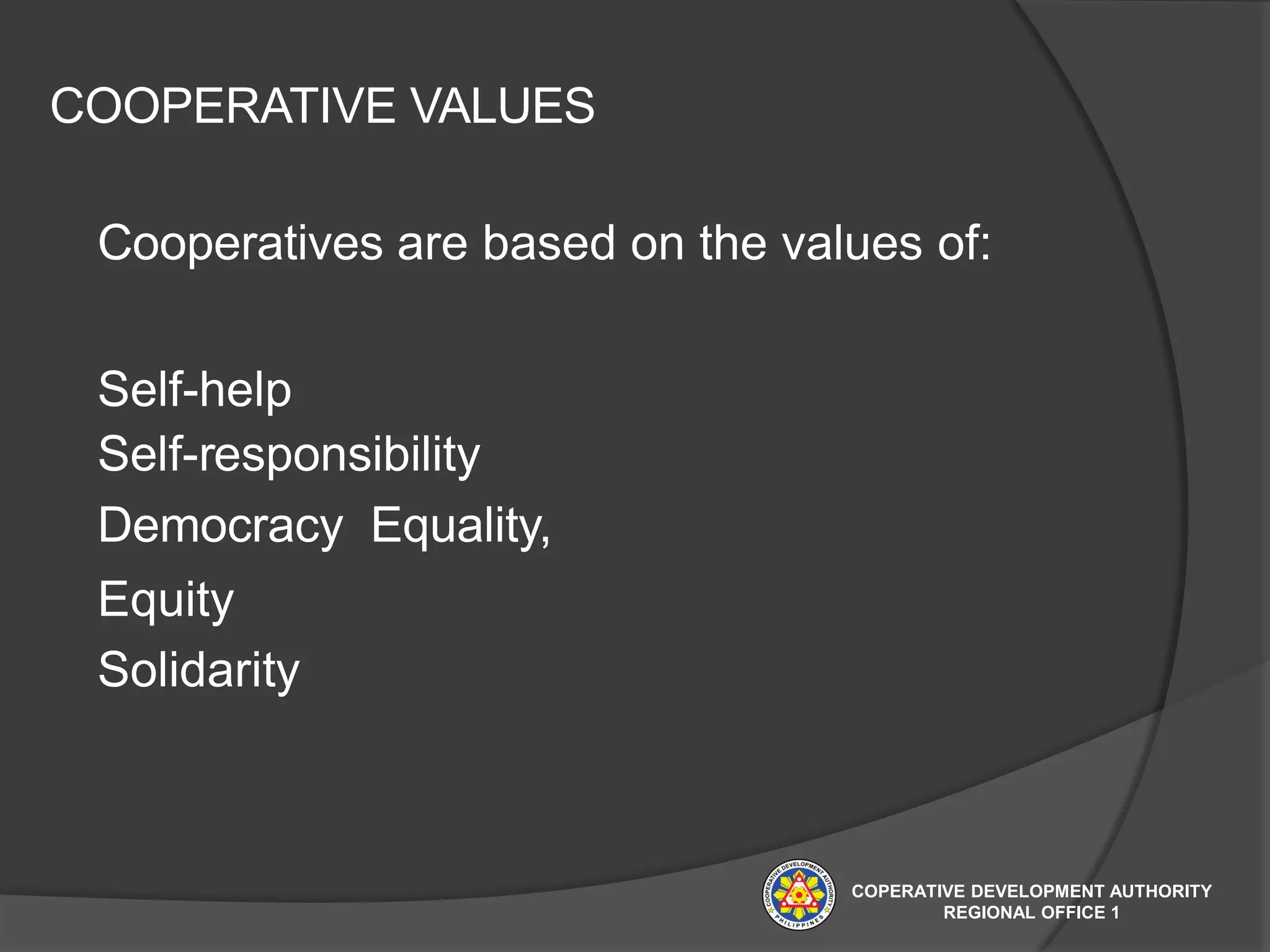

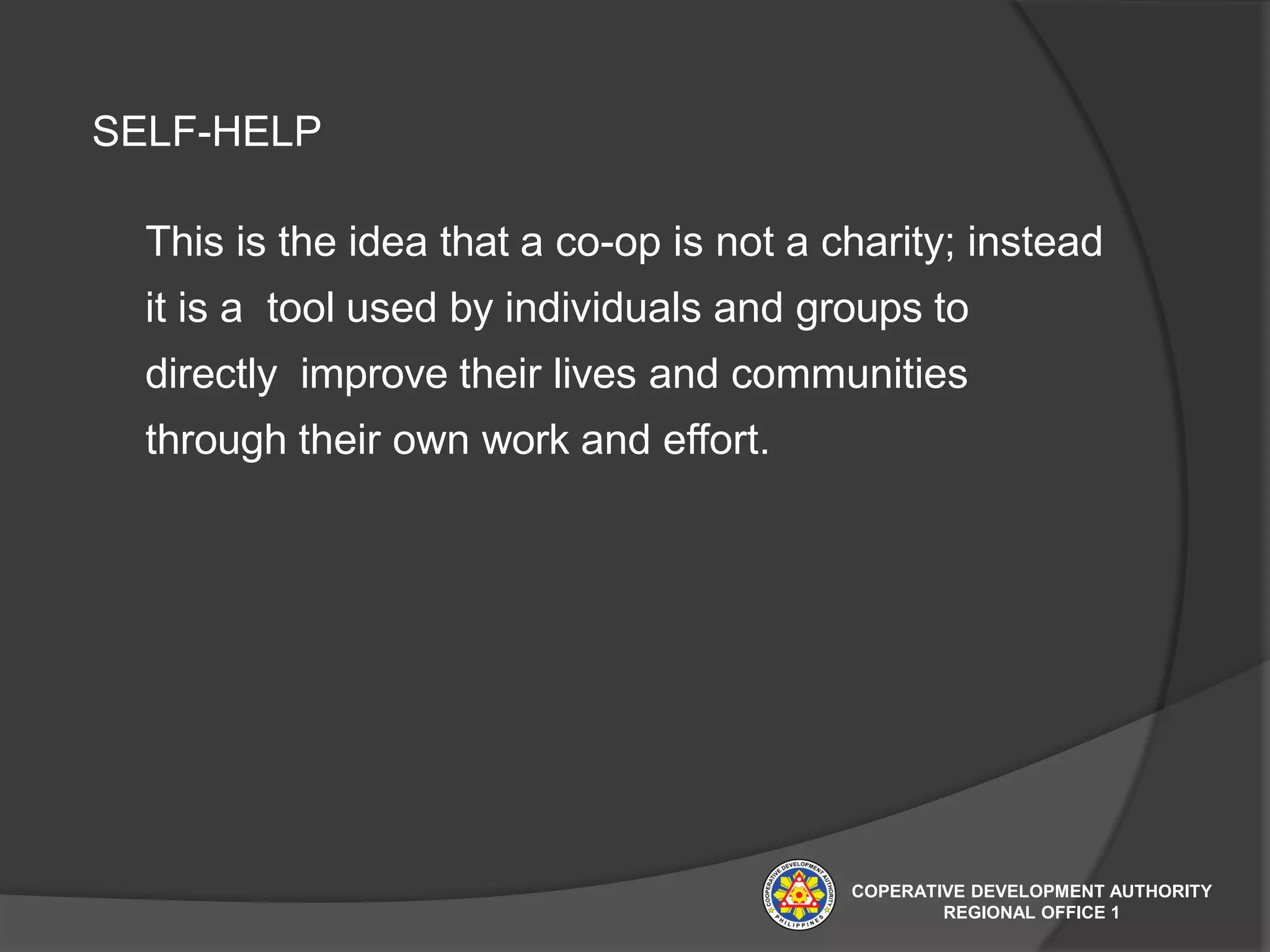

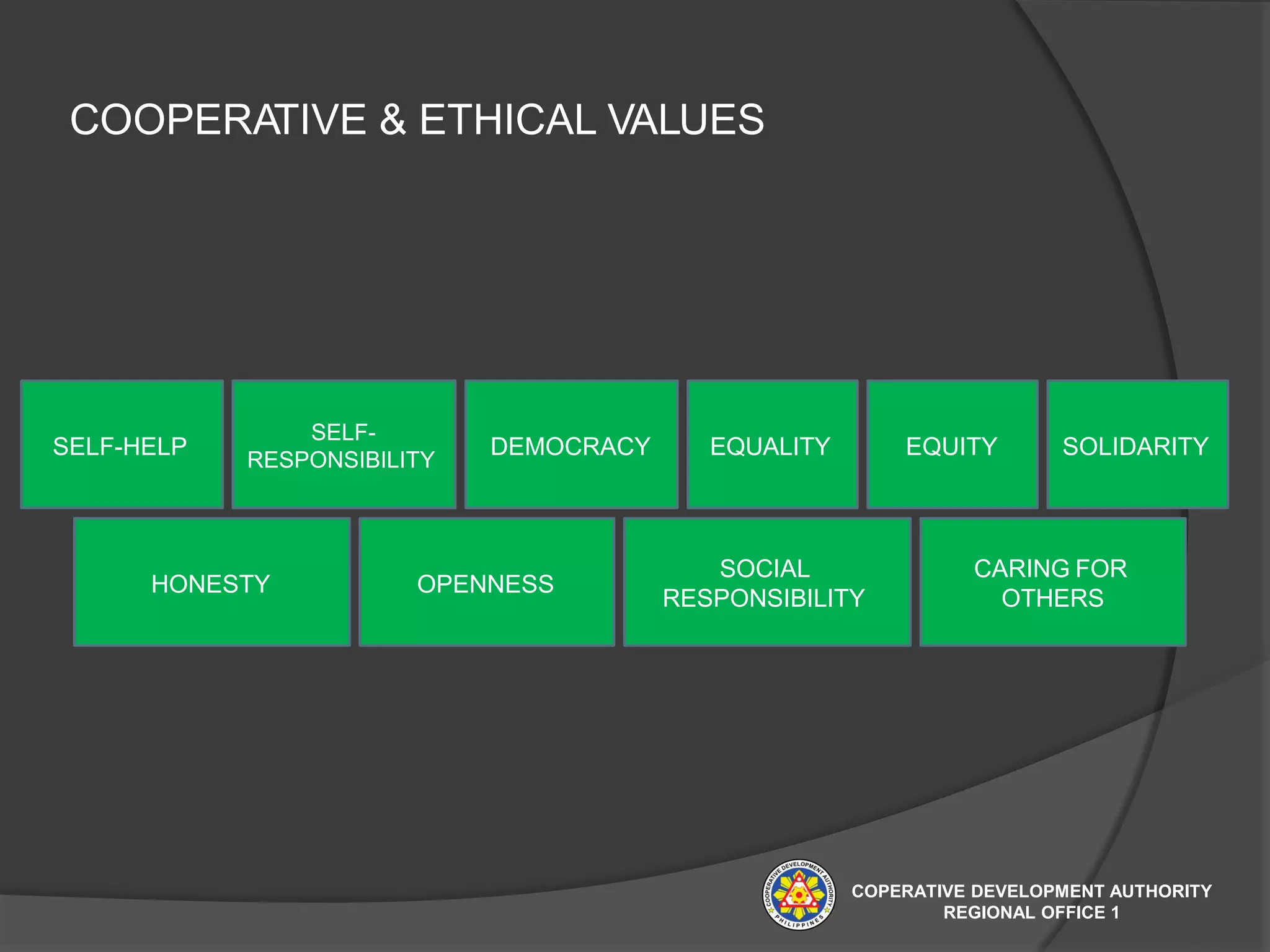

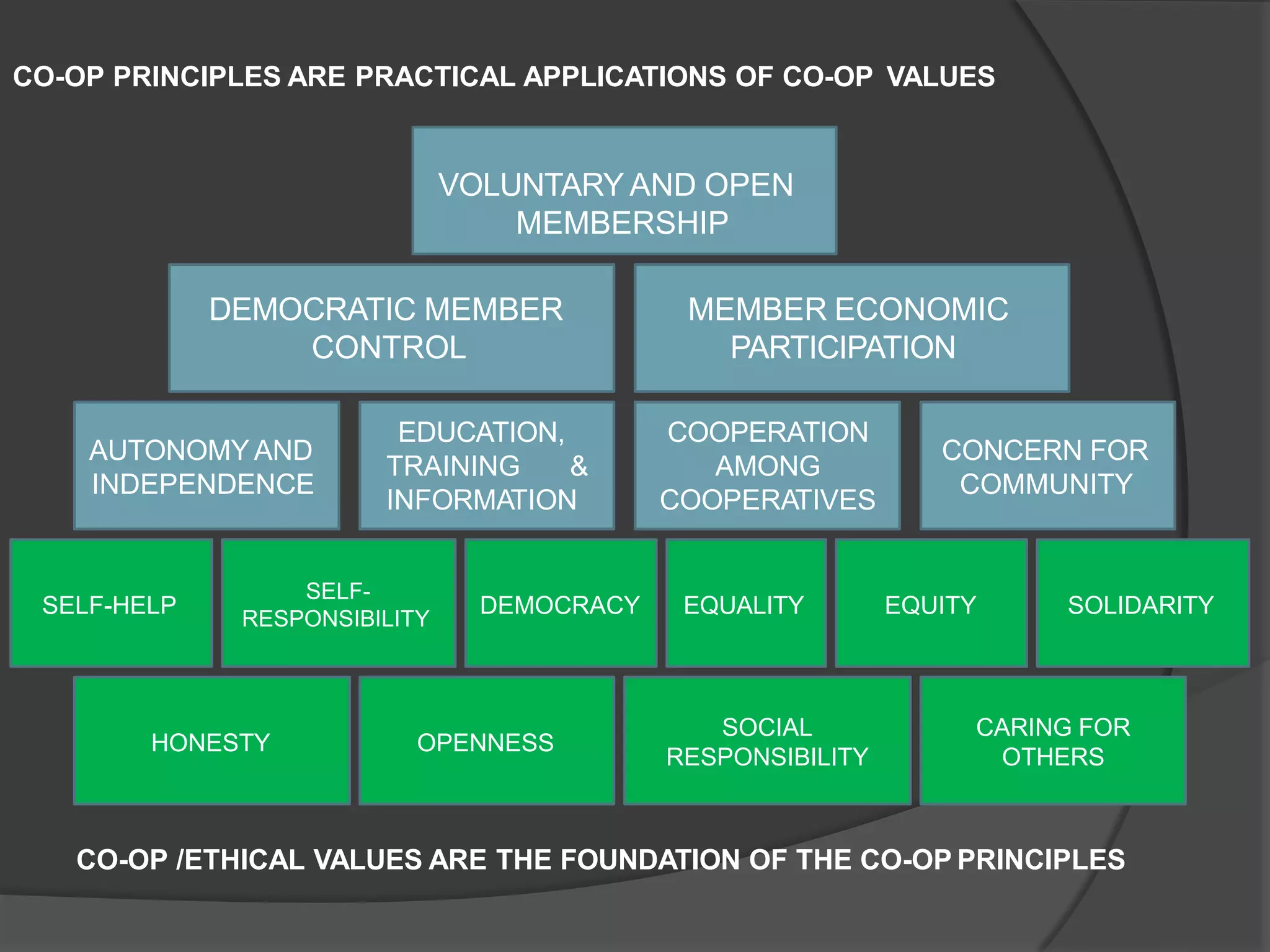

The document discusses key topics related to the operation and management of cooperatives, including financial management, personnel management, human resource management, production, marketing, technical aspects, ethical standards, and performance measurement. Specifically, it covers: 1. The importance of financial management for cooperatives to ensure availability of funds, optimum utilization of funds, safety of investments, and a sound capital structure. 2. The differences between personnel management, which focuses on routine employee functions, and human resource management, which treats employees as strategic assets. 3. The values and principles that cooperatives are based on like self-help, self-responsibility, democracy, equality, equity, and solidarity. 4. Common areas