Download as PPSX, PPTX

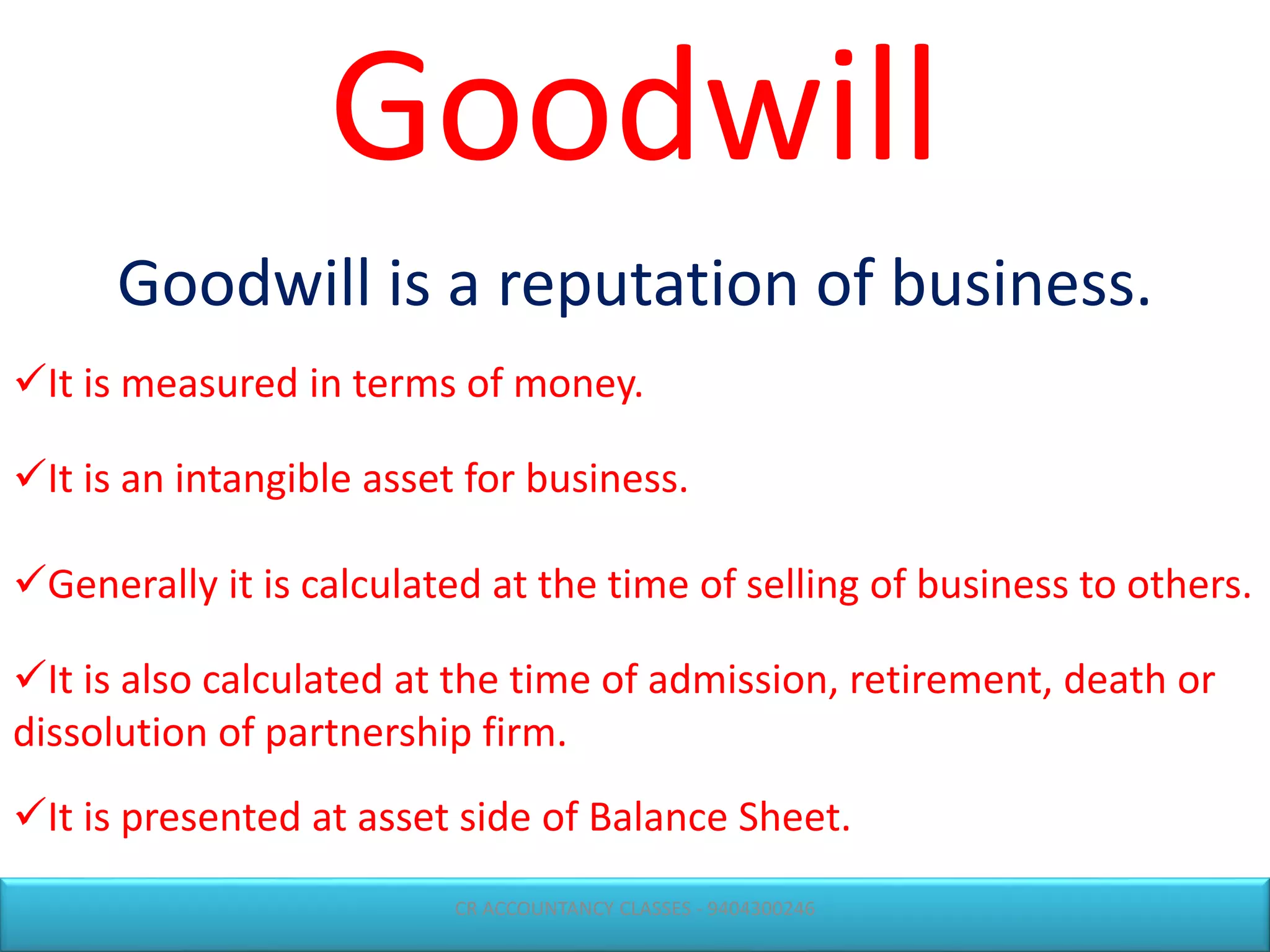

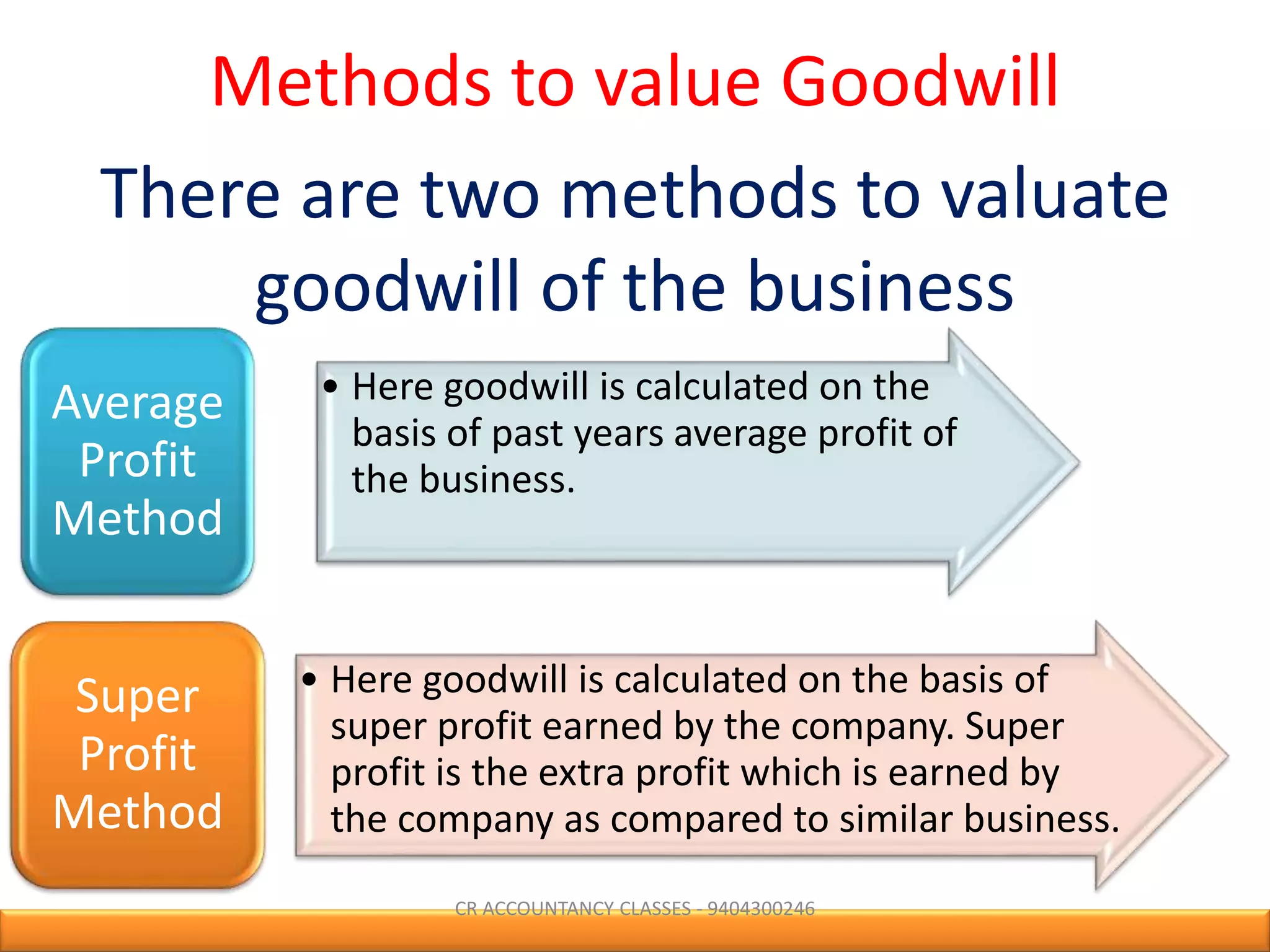

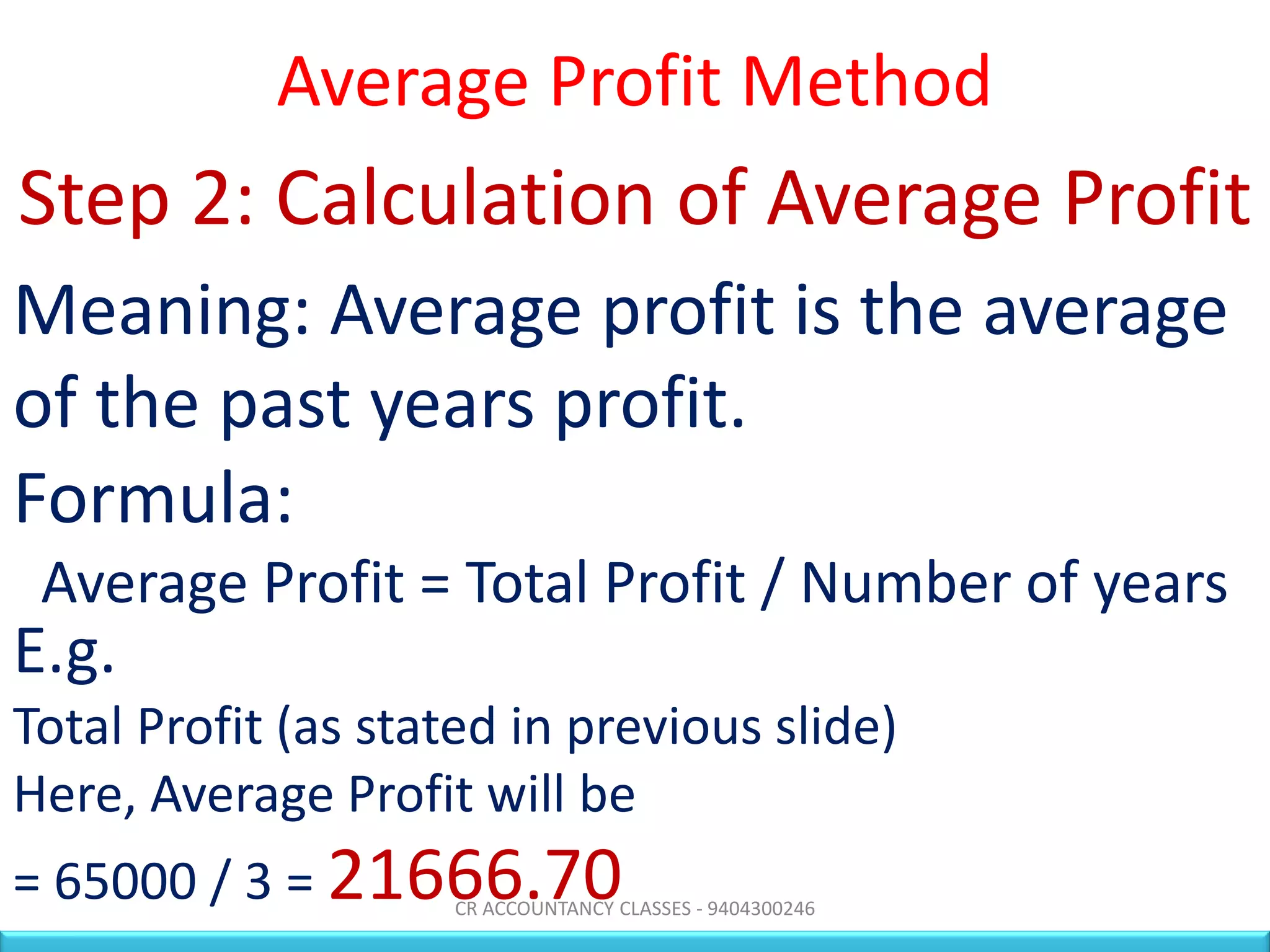

This document discusses methods for valuing goodwill, an intangible asset representing a business's reputation and future earning potential. It describes two methods: the average profit method and super profit method. The average profit method calculates goodwill based on the average profits of past years. It involves determining total profits, calculating the average profit, adjusting for any profit items, and multiplying the adjusted average profit by the number of purchase years. The super profit method calculates goodwill based on any extra "super profits" above what similar businesses earn.