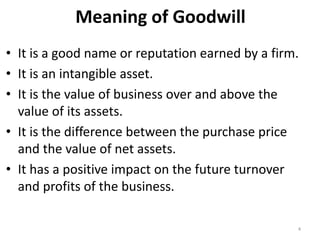

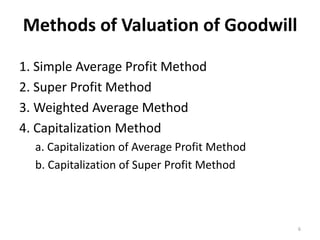

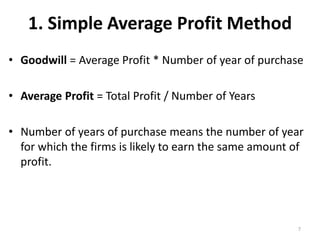

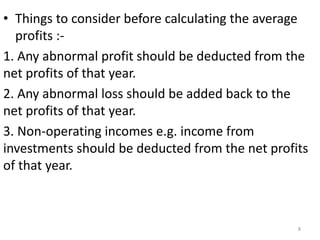

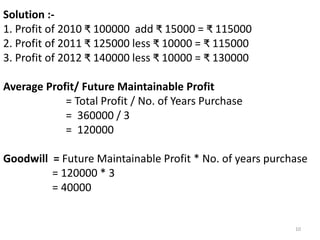

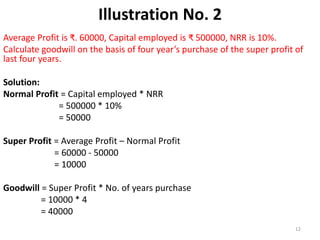

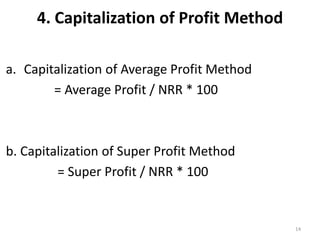

This document discusses various methods for valuing goodwill, including the simple average profit method, super profit method, weighted average profit method, and capitalization of profit method. The simple average profit method calculates goodwill as the average profit over multiple years multiplied by the number of years of purchase. The super profit method uses excess profits over normal profits to calculate goodwill. Weighted average and capitalization methods provide modified approaches. Examples are provided to illustrate the simple average and super profit methods.