Downloaded 48 times

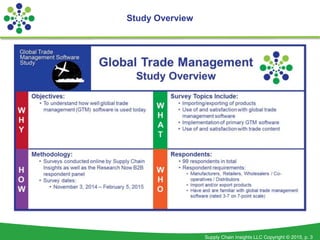

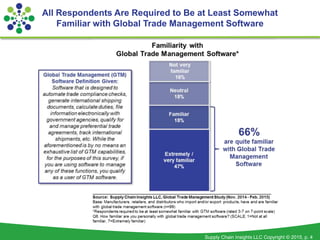

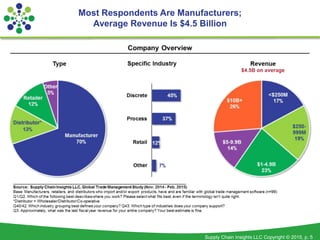

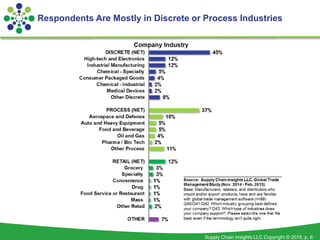

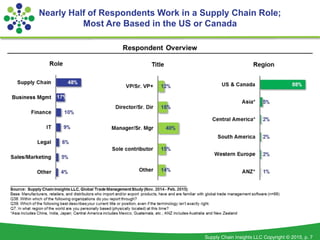

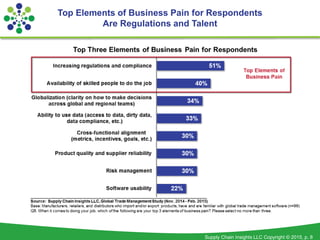

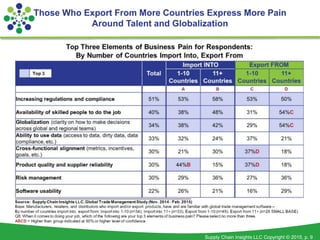

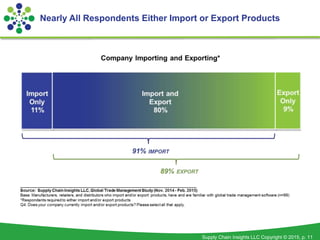

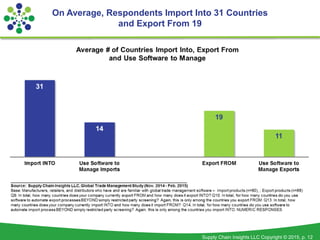

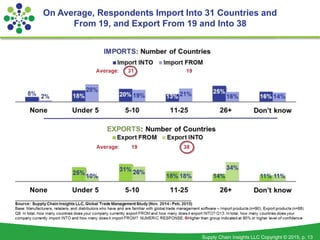

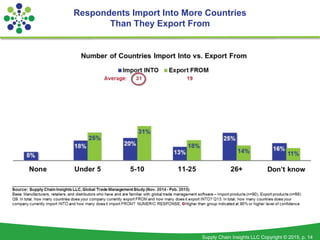

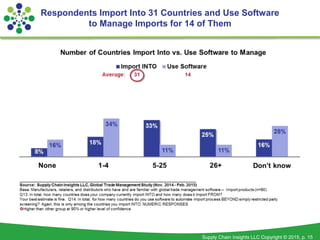

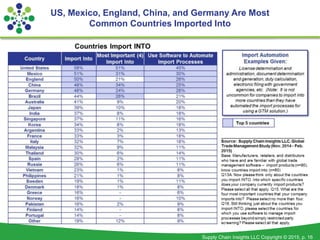

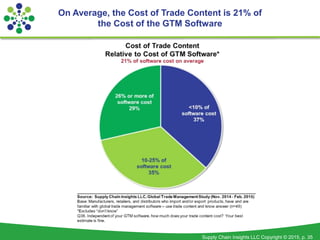

The document summarizes a study on global trade management software, focusing on insights gathered from manufacturers with an average revenue of $4.5 billion. Key findings indicate that nearly all respondents import or export products, with specific countries being most common for trade, and that satisfaction levels with GTM solutions vary based on revenue and application capabilities. The study also highlights business pain points related to regulations and talent, as well as the implementation and cost dynamics of GTM software.