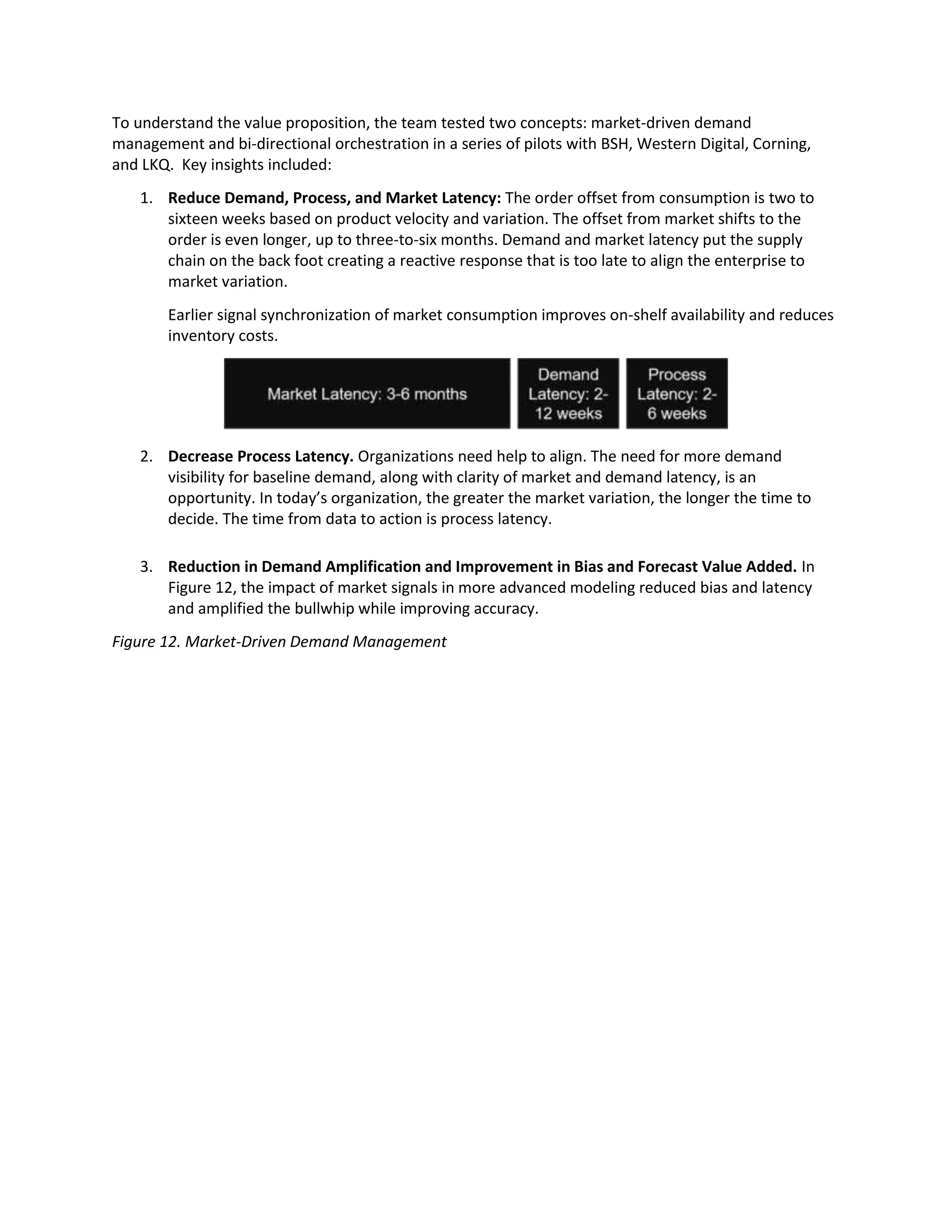

Downloaded 20 times

The document discusses defining and testing new "outside-in" supply chain planning processes that use market data rather than just internal data. It summarizes the results of workshops and pilots with various companies testing these new approaches. The key ideas are: 1) Traditional "inside-out" supply chain planning focuses only on internal data and is insufficient for today's disrupted environment. 2) New "outside-in" processes would use a wider range of market data signals to improve demand sensing and supply chain response times. 3) Workshops and pilots identified 9 new potential planning models and tested concepts like market-driven demand management and bi-directional orchestration. 4) The results showed these new approaches