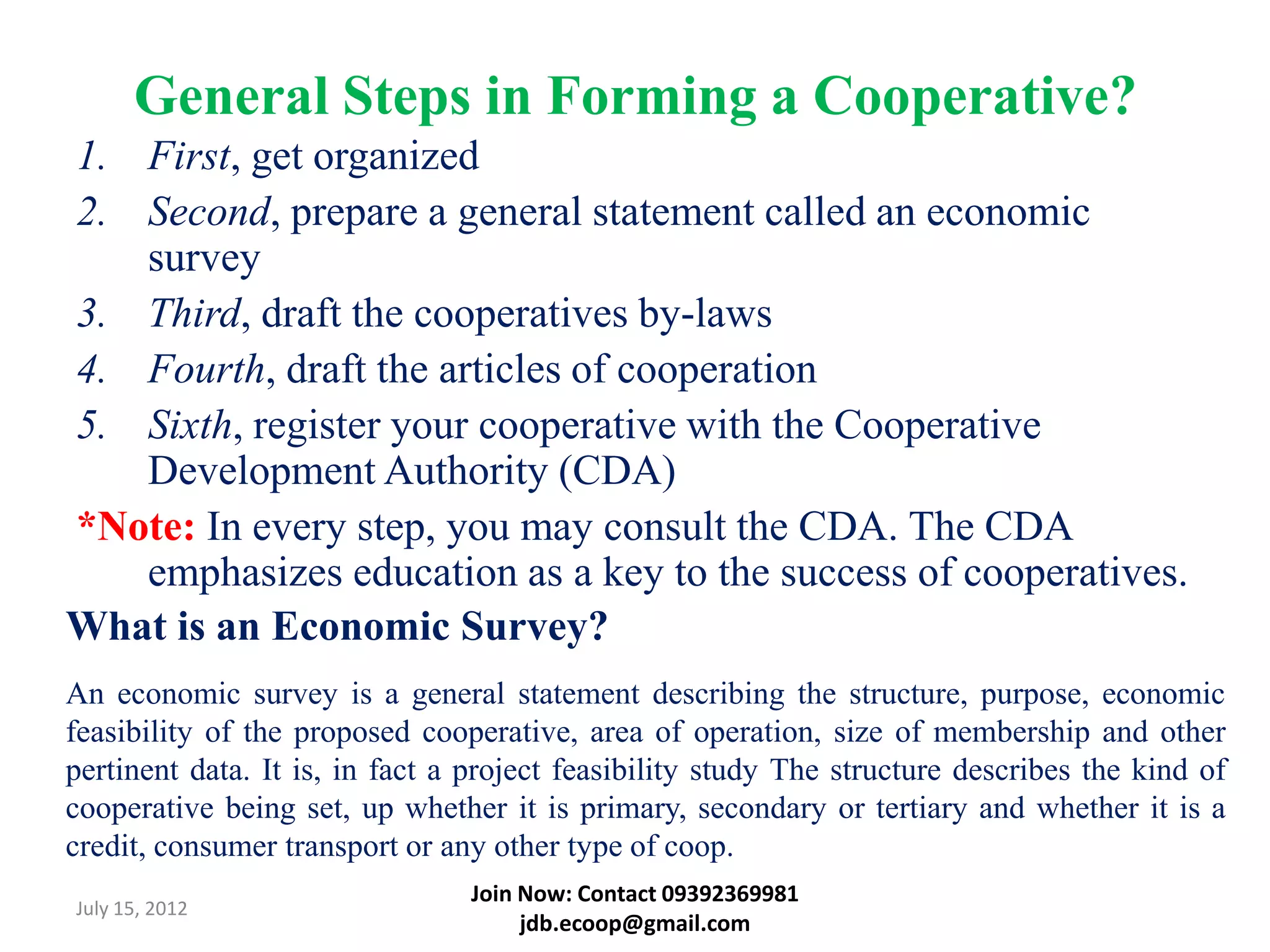

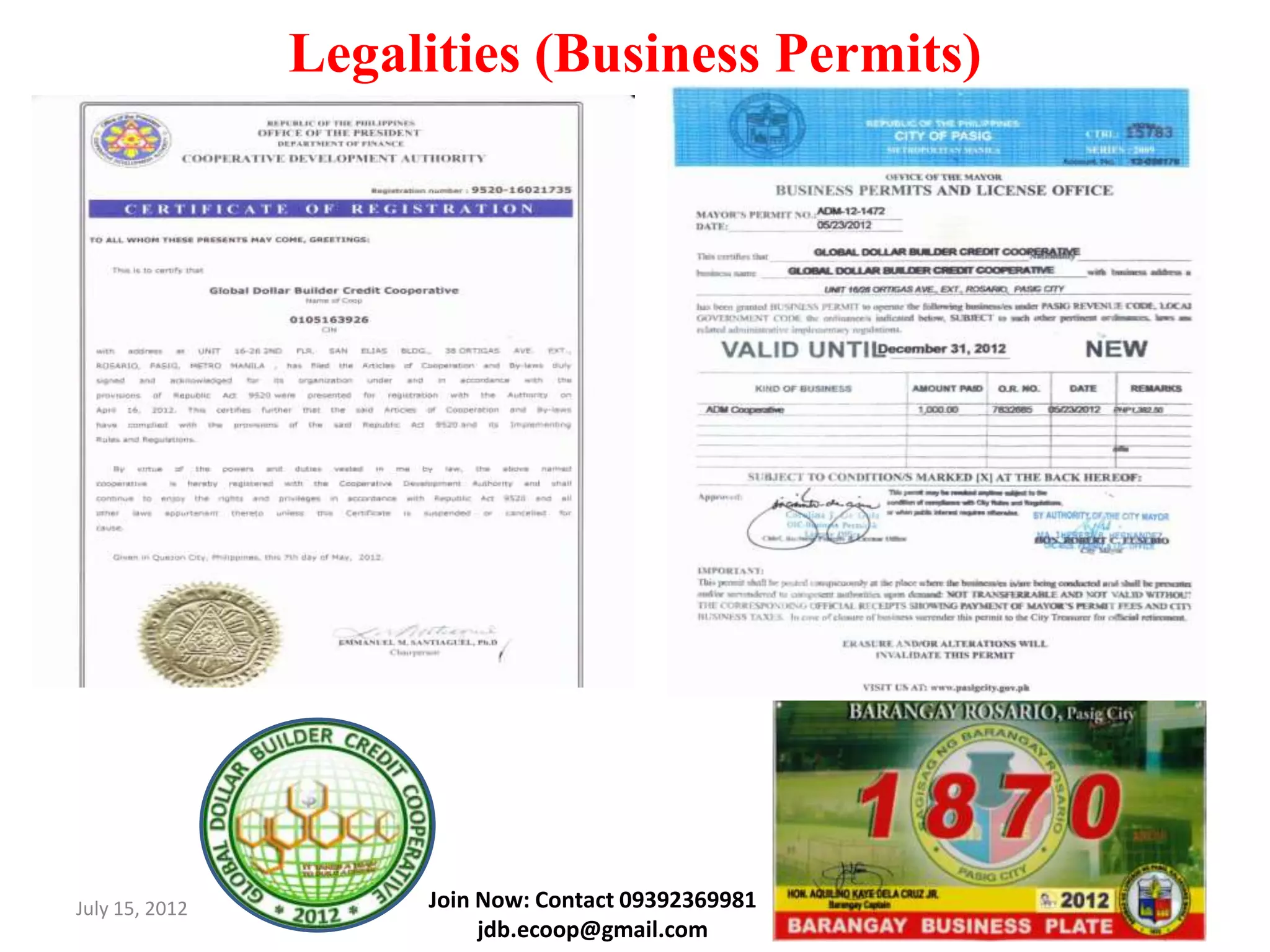

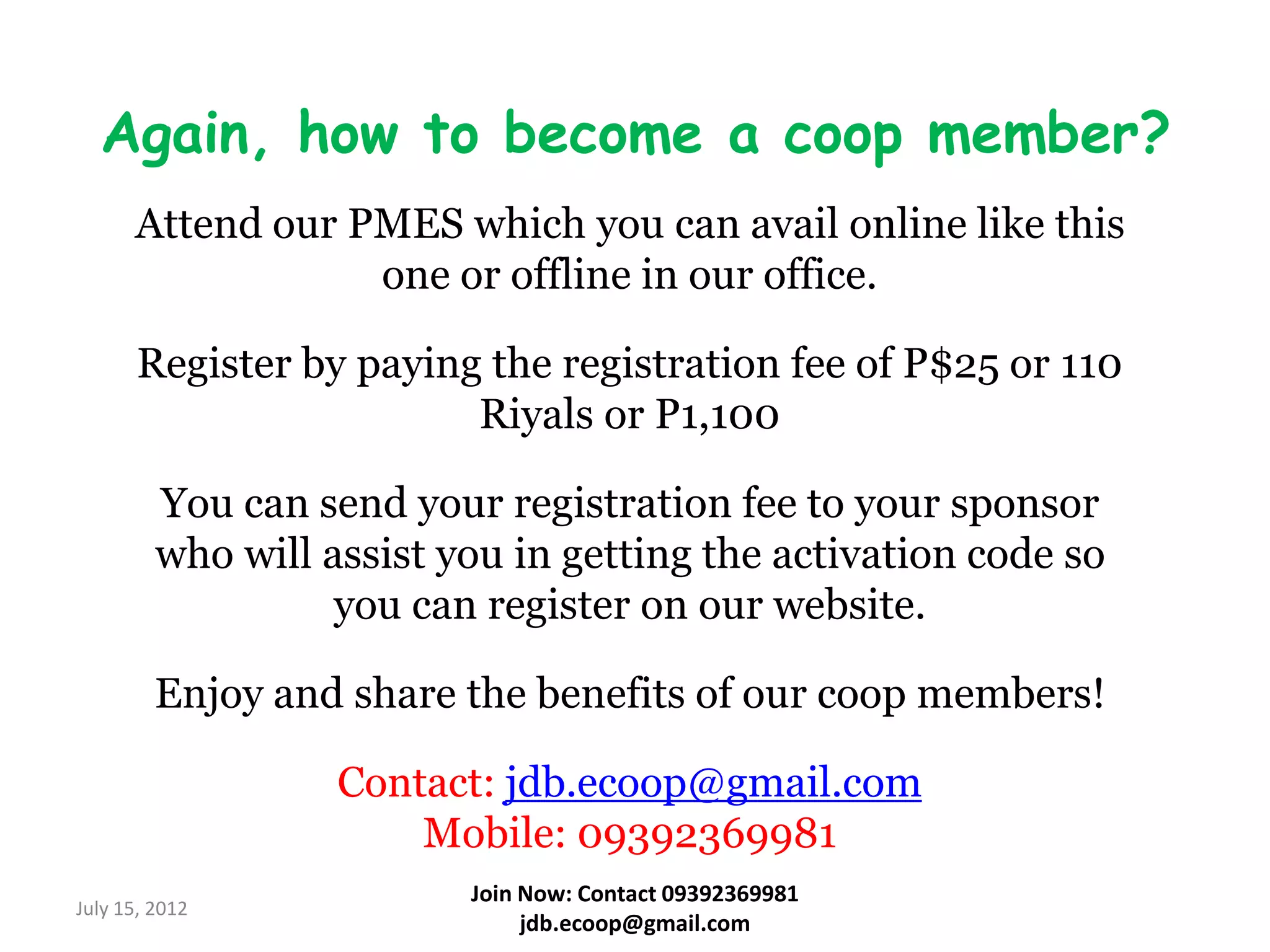

The document provides information about joining the Global Dollar Builder Credit Cooperative (GDBCC). It discusses the requirements for becoming a member, including undergoing a Pre-Membership Education Seminar (PMES). The PMES covers basic concepts of cooperatives and details about GDBCC, its products/services, and how members can earn income and benefits. All cooperatives must register with the Cooperative Development Authority according to Philippine law.