Downloaded 80 times

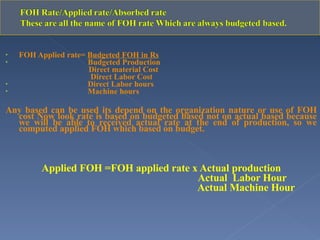

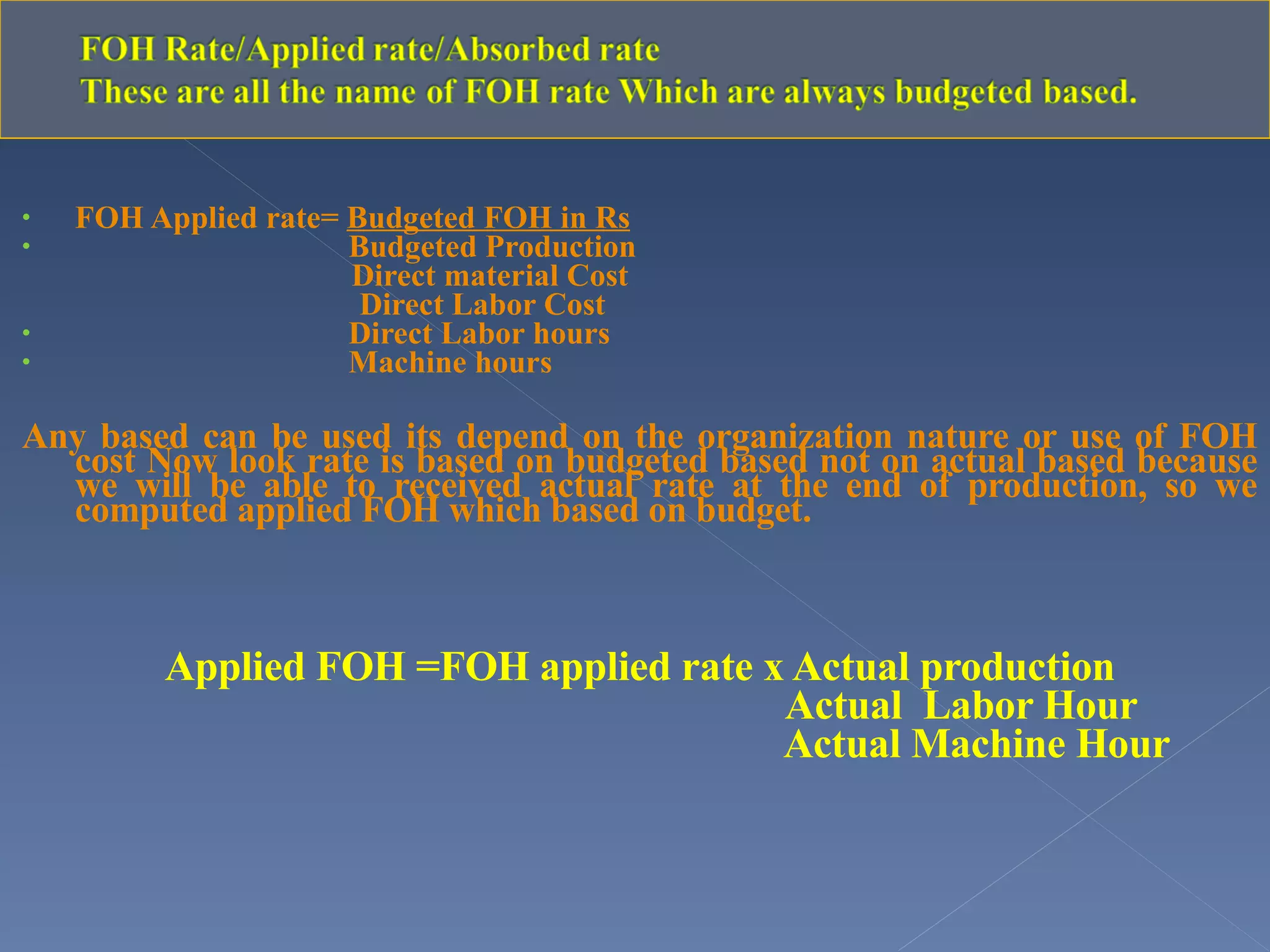

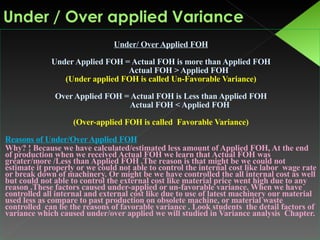

This document discusses the calculation of applied fixed overhead and variances from actual fixed overhead. It states that applied fixed overhead is calculated based on budgeted figures and is used until actual overhead is known. The variance between actual and applied fixed overhead is then identified, with actual overhead exceeding applied defined as an unfavorable variance and actual less than applied defined as a favorable variance. Reasons for variances include inaccurate estimation, inability to control internal costs like wages, and inability to control external costs like material prices.