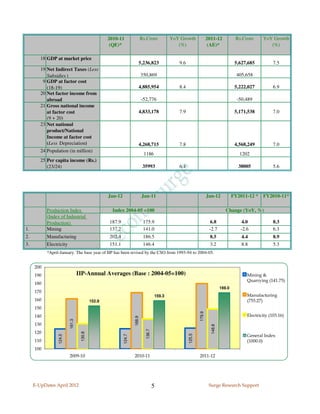

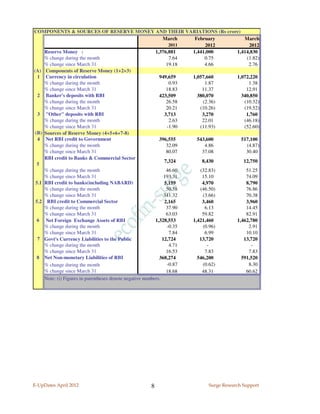

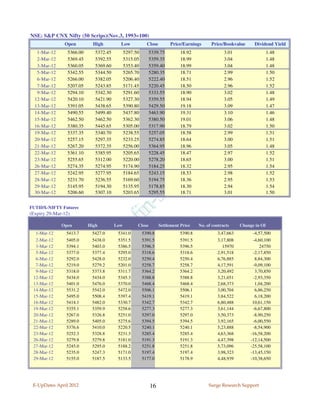

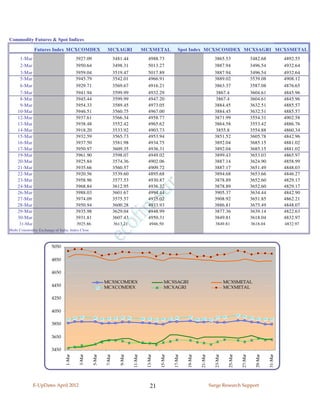

![Growth Indicators

GDP Growth Rates Q1 Q2 Q3 Q4 FY

2011-12 7.7* 6.9* 6.1 6.9 (AE)*

2010-11 8.5* 7.6* 8.3* 7.8 8.4 (QE)*

GDP[at Constant(2004-05) prices] Q3 Rs.Crore YoY Growth Q3 Rs.Crore YoY Growth

2010-11* (Share in 2011-12* (Share in

GDP) GDP)

(%) (%)

1 Agriculture, Forestry &

Fishing 224,044 11.0 230,168 2.7

2 Mining & Quarrying 28,200 6.1 27,334 -3.1

3 Manufacturing

194,435 7.8 195,228 0.4

4 Electricity, Gas & Water

Supply. 22,480 3.8 24,509 9.0

5 Construction

96,000 8.7 102,887 7.2

6 Trade, Hotels, Transport

and Communication 330,573 9.8 361,074 9.2

7 Financing, Insurance,

Real Estate & Business

Services. 214,205 11.2 233,537 9.0

8 Community, Social &

Personal Services. 152,857 -0.8 164,866 7.9

9 GDP at factor cost

(1 to 8) 1,262,794 8.3 1,339,603 6.1

10 Private final consumption

expenditure

818,122 7.6 (60.4) 869,193 6.2 (60.4)

11 Government final

consumption expenditure

168,576 4.7 (12.5) 175,952 4.4 (12.2)

12 Gross fixed capital

formation 437,564 11.1 (32.3) 432,169 -1.2 (30.0)

13 Changes in stocks 48,036 (3.5) 47,820 (3.3)

14 Valuables 29,981 (2.2) 32,909 (2.3)

15 Exports

316,694 28.1 (23.4) 358,160 13.1 (24.9)

16 Less Imports 401,587 14.2 (29.7) 471,062 17.3 (32.7)

17 Discrepancies -63,628 (-4.7) -6,222 (-0.4)

18 GDP at market price

(10 to 17) 1,353,757 10.1 (100) 1,438,918 6.2 (100)

*Estimates based on the New series of IIP. QE: Quick Estimates; AE: Advanced Estimates.

E-UpDates April 2012 4 Surge Research Support](https://image.slidesharecdn.com/eupdtsapr12-120605213753-phpapp02/85/E-Updates_Apr12-Indian-Global-Economic-Indicators-4-320.jpg)

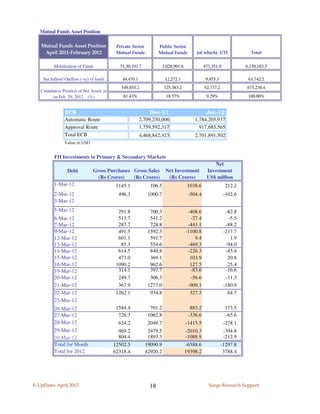

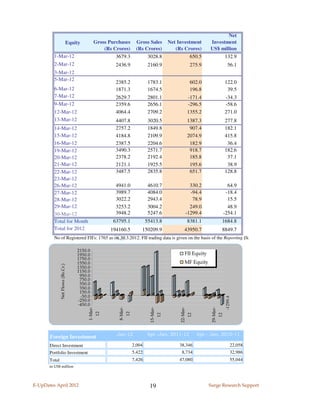

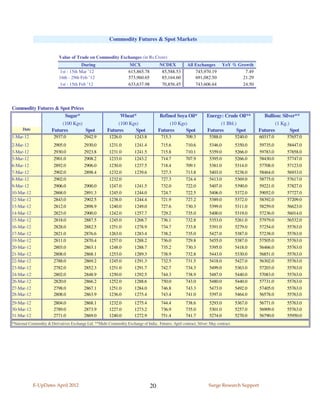

The document provides a comprehensive analysis of the Indian economy as of April 2012, detailing key growth, price, banking, and exchange rate indicators alongside global economic comparisons. It includes statistics such as GDP growth rates, inflation figures, and components of money supply, presenting advanced estimates for the fiscal year. Additionally, it features insights into the Union Budget for 2012-2013, highlighting important economic trends and metrics.