Download to read offline

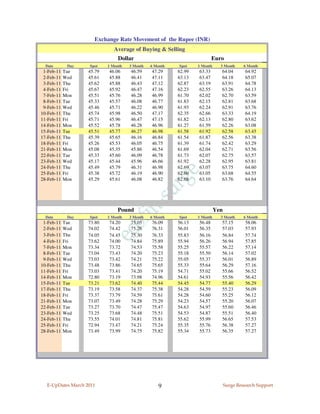

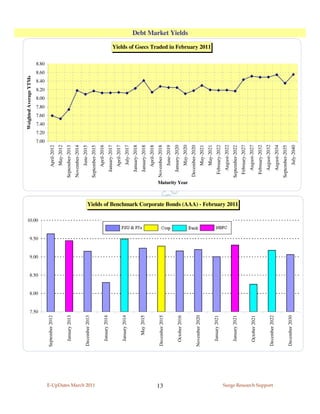

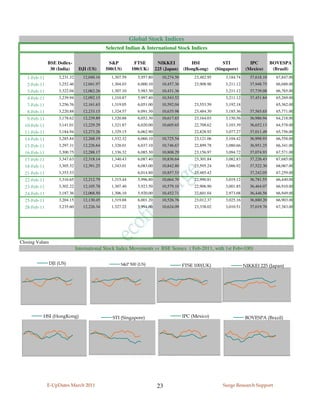

![Growth Indicators

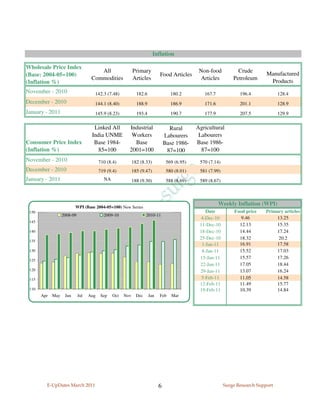

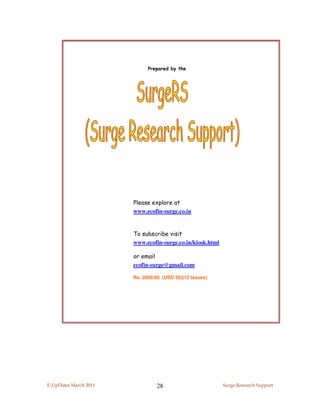

GDP Growth Rates Q1 Q2 Q3 Q4 FY

2010-11 8.9 8.9 8.2 8.6

2009-10 6.3 8.6 7.3 7.4

GDP[at Constant(2004-05) prices] Q2-2010-11 Rs.Crore YoY Growth Q3-2010-11 Rs.Crore YoY Growth

(Jul-Sep) (Share in (Oct-Dec) (Share in

GDP) GDP)

(%) (%)

1 Agriculture, Forestry &

Fishing 130,335 4.4 219,494 8.9

2 Mining & Quarrying 25,444 7.9 28,118 6.0

3 Manufacturing

188,919 9.8 190,767 5.6

4 Electricity, Gas & Water

Supply. 23,036 3.4 23,151 6.4

5 Construction

93,294 8.7 94,566 8.0

6 Trade, Hotels, Transport

and Communication 317,716 12.1 330,032 9.4

7 Financing, Insurance,

Real Estate & Business

Services. 205,253 8.2 214,716 11.2

8 Community, Social &

Personal Services. 168,620 7.4 160,819 4.8

9 GDP at factor cost

(1 to 8) 1,152,618 8.9 1,261,664 8.2

10 Private final consumption

expenditure

744,033 8.6 (59.2) 827,021 9.0 (60.1)

11 Government final

consumption expenditure

140,521 10.4 (11.2) 159,579 -3.0 (11.6)

12 Gross fixed capital

formation 428,033 17.8 (34.1) 410,767 5.6 (29.8)

13 Changes in stocks 44,903 (3.6) 45,295 (3.3)

14 Valuables 27,591 (2.2) 29,482 (2.1)

15 Exports

271,075 13.8 (21.6) 281,157 16.2 (20.4)

16 Less Imports 364,755 13.8 (29.0) 325,419 -7.3 (23.6)

17 Discrepancies -34,625 (-2.8) -51,641 (-3.8)

18 GDP at market price

(10 to 17) 1,256,776 10.4 (100) 1,376,242 9.7 (100)

E-UpDates March 2011 4 Surge Research Support](https://image.slidesharecdn.com/eupdtsmar11-1310897222-phpapp02-110717051509-phpapp02/85/E-UpDates_Mar11-4-320.jpg)

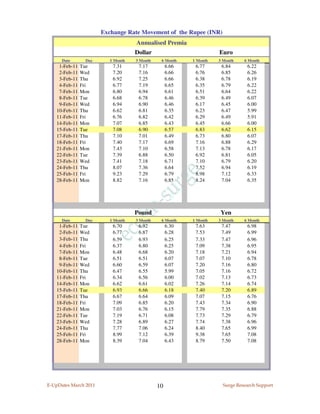

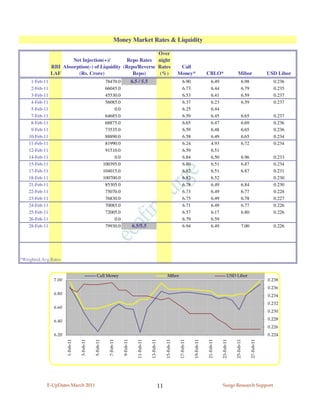

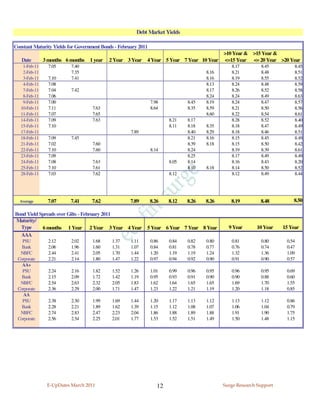

The document presents a comprehensive overview of Indian and global economic and financial market indicators as of March 2011, detailing key metrics such as GDP growth rates, inflation, exchange rates, and banking indicators. It highlights important statistics related to various sectors, consumer price indices, and government expenditures, reflecting the economic performance and trends during that period. Additionally, it covers components of money stock, reserve money, and various financial ratios relevant to understanding the economic landscape.