Downloaded 11 times

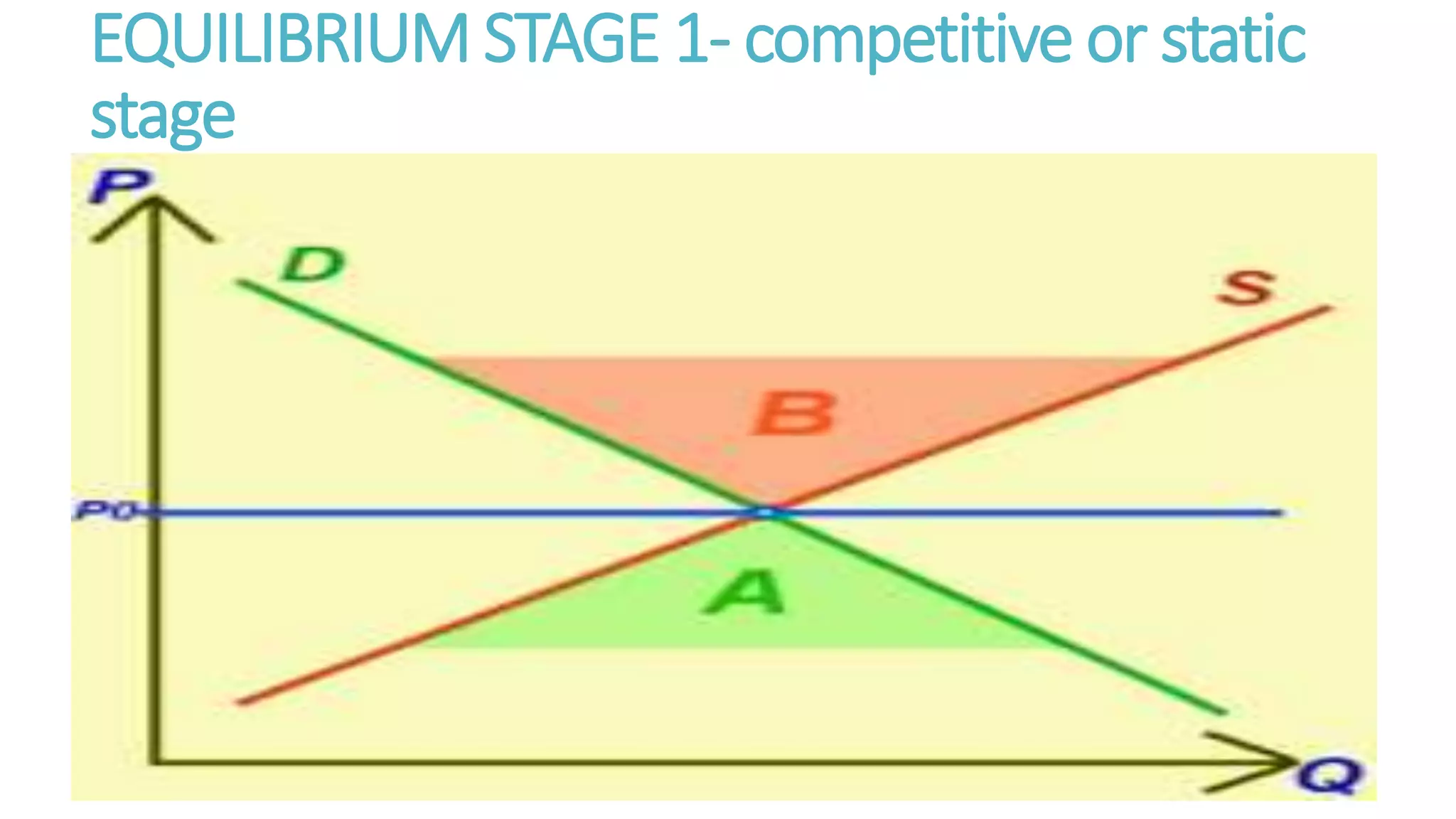

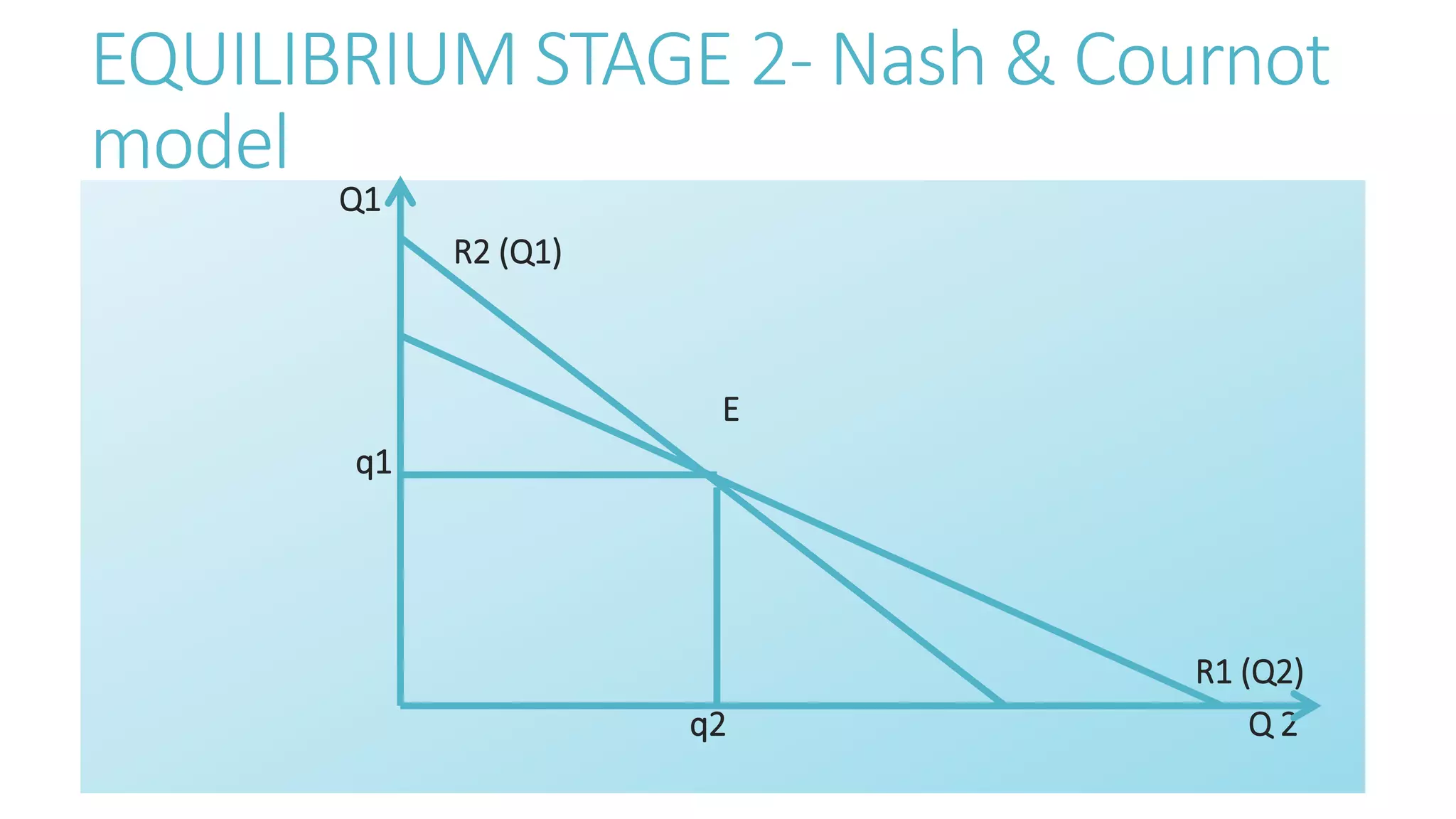

The document discusses the concept of economic equilibrium, which occurs when supply and demand are balanced, leading to maximum consumer satisfaction and producer profit. It defines market equilibrium as the established price where quantity demanded equals quantity supplied and highlights the dynamic nature of equilibrium, including various models and exceptions. Key characteristics include consistent agent behavior and a lack of incentive for change in equilibrium conditions.

![Lesson 8--equilibrium[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-8-equilibrium1-130409201835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)