The document discusses ensuring effective implementation of oversight committee recommendations in Ghana. It covers the following key points:

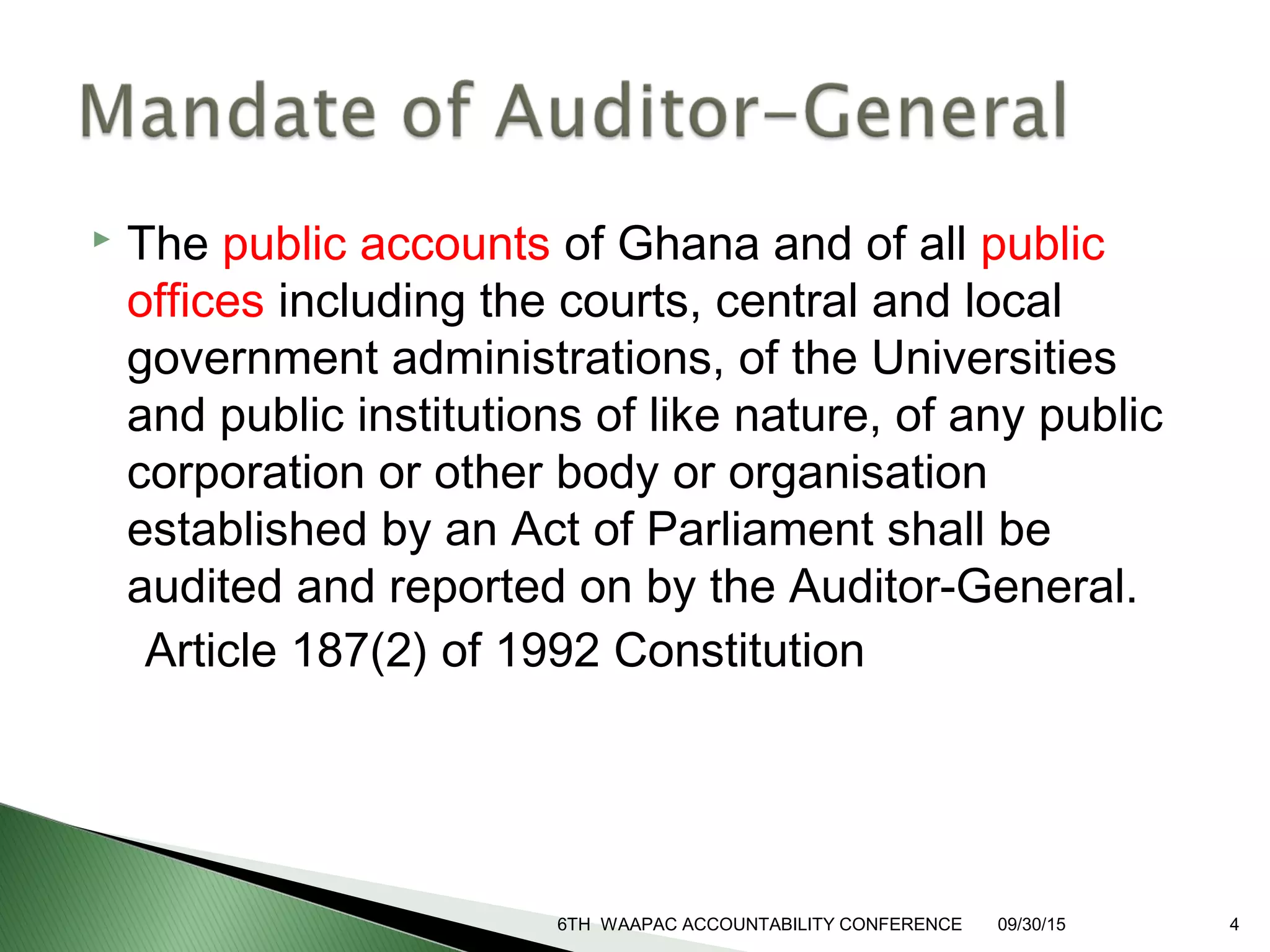

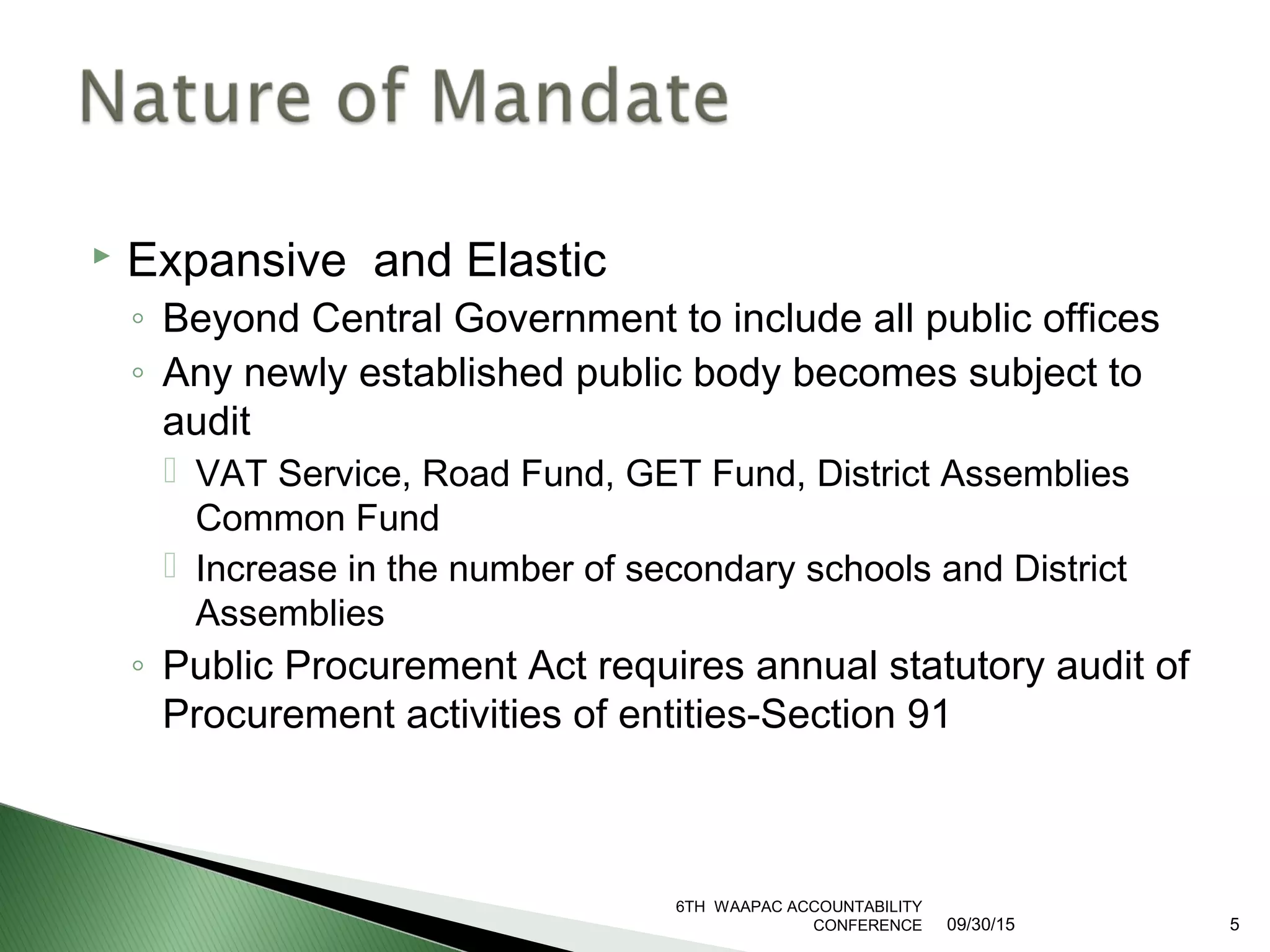

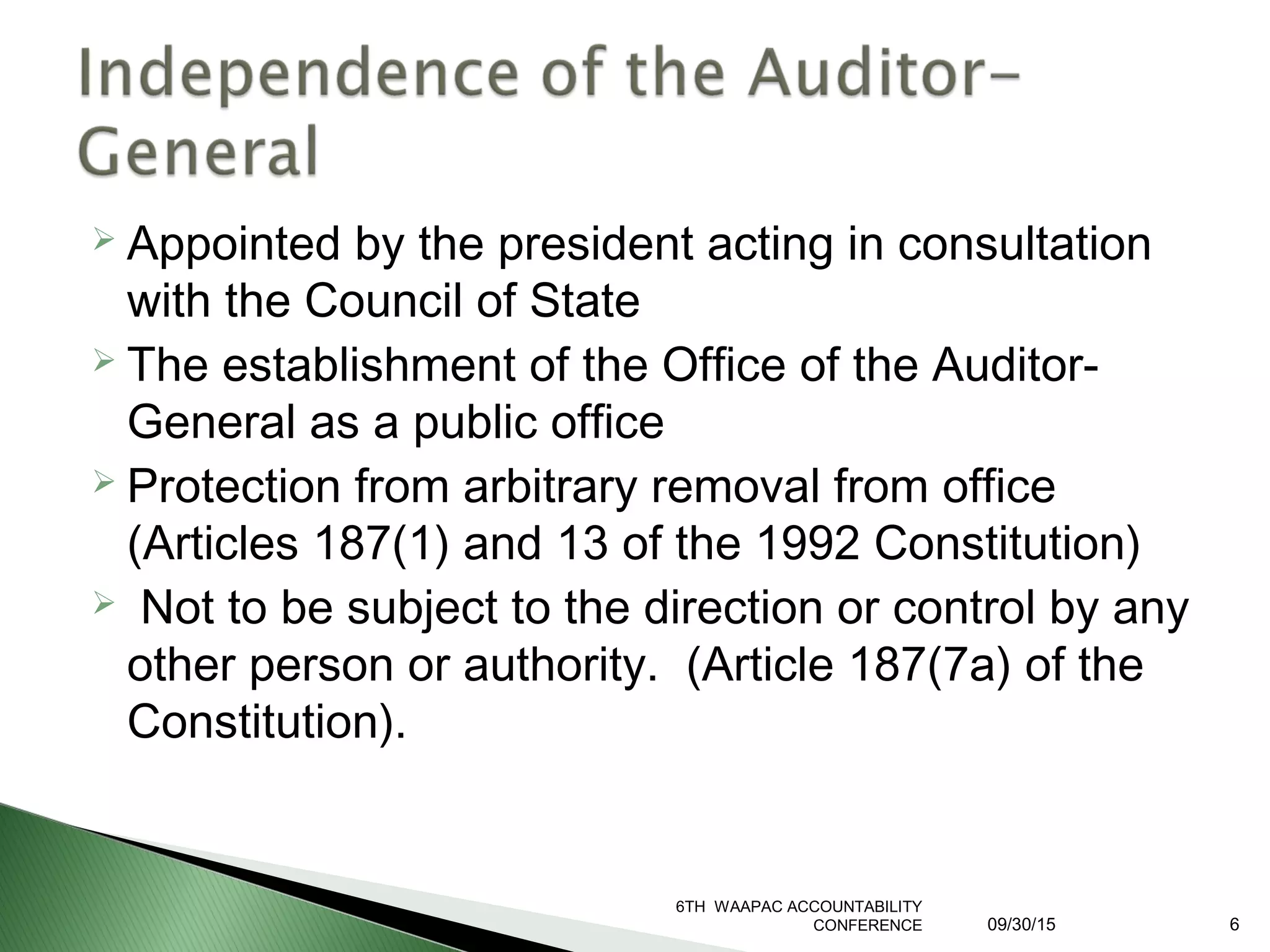

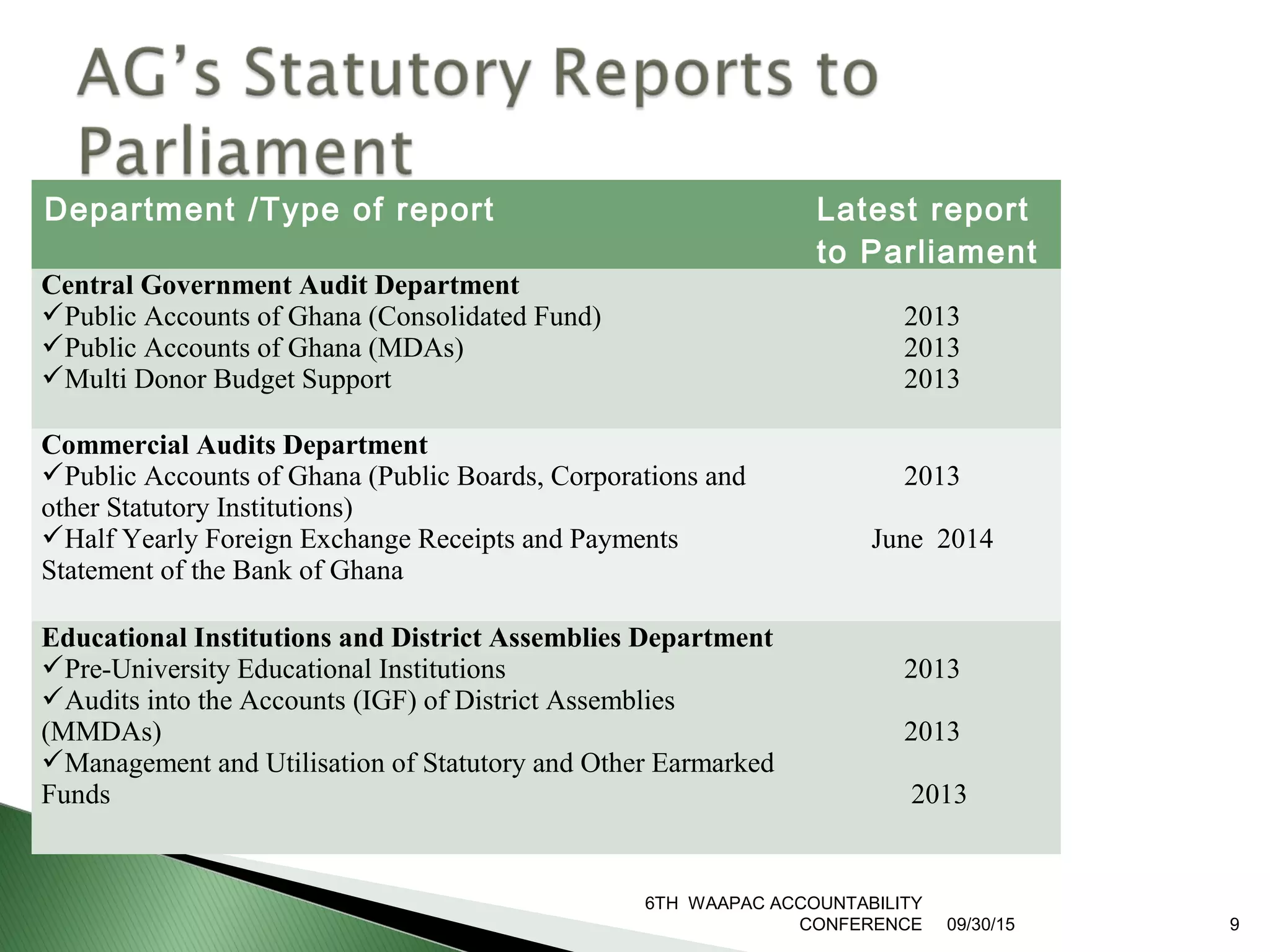

1. The mandate of the Auditor-General of Ghana is to audit all public offices and institutions established by law. This includes central and local government as well as public universities.

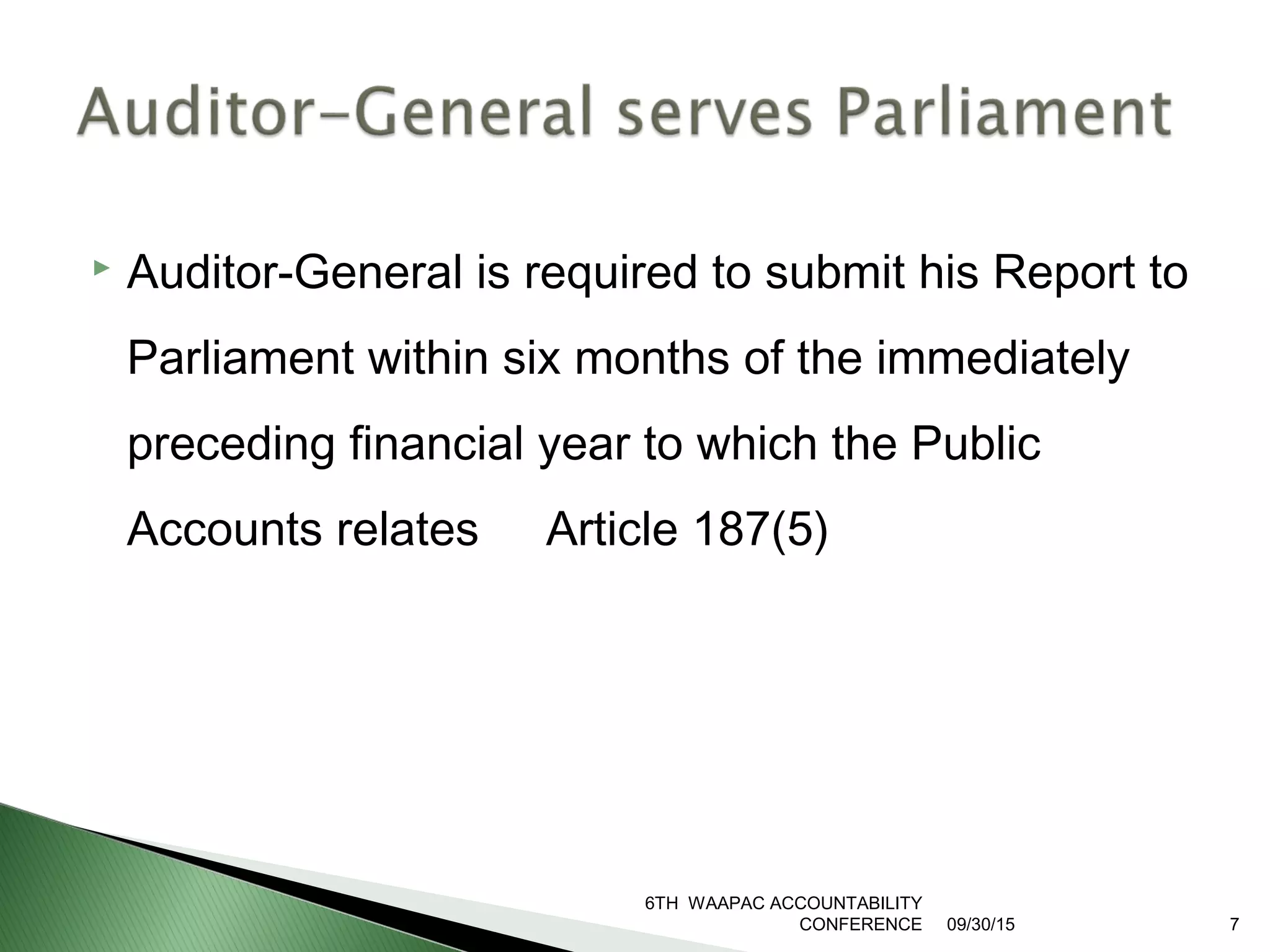

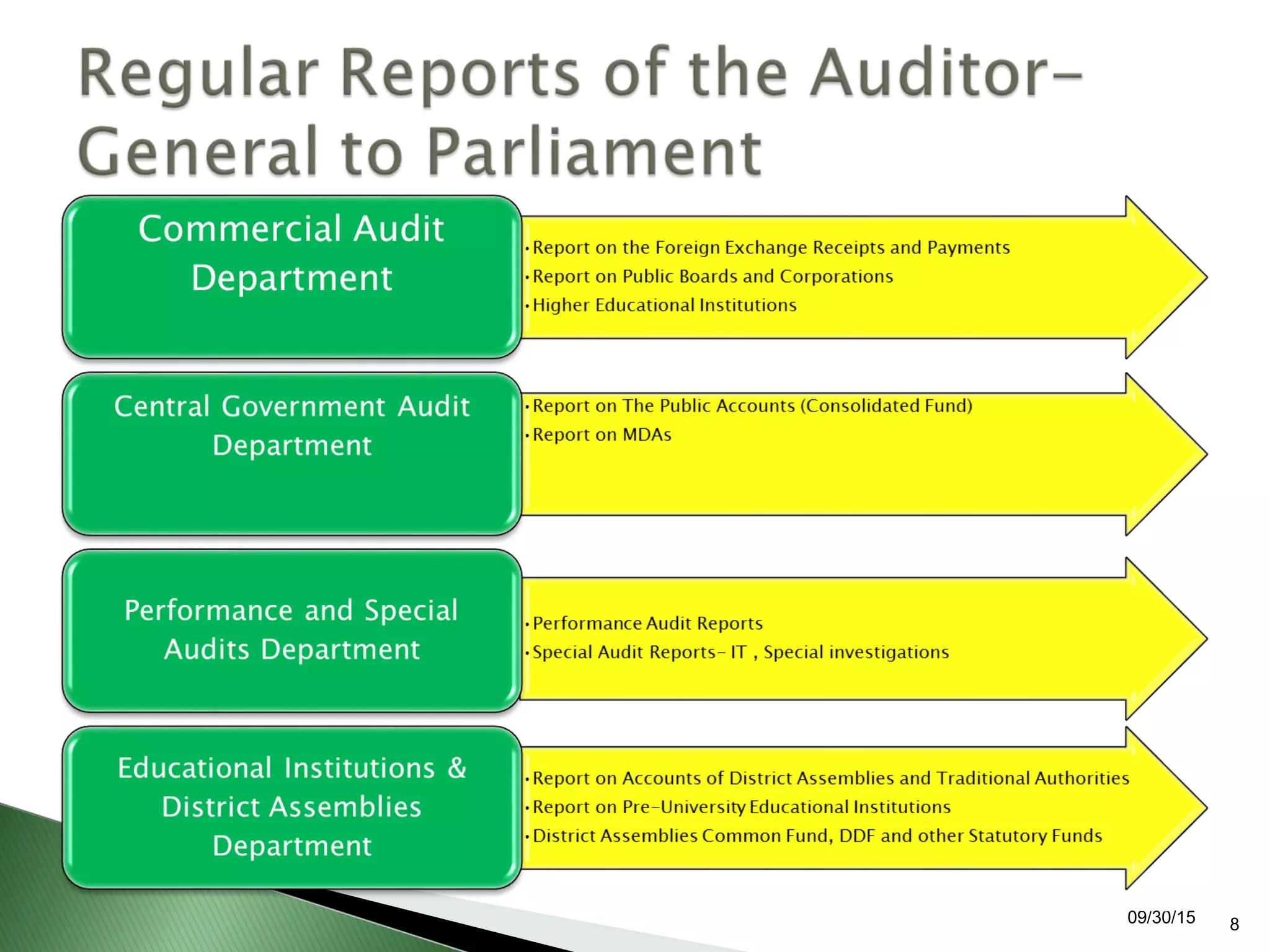

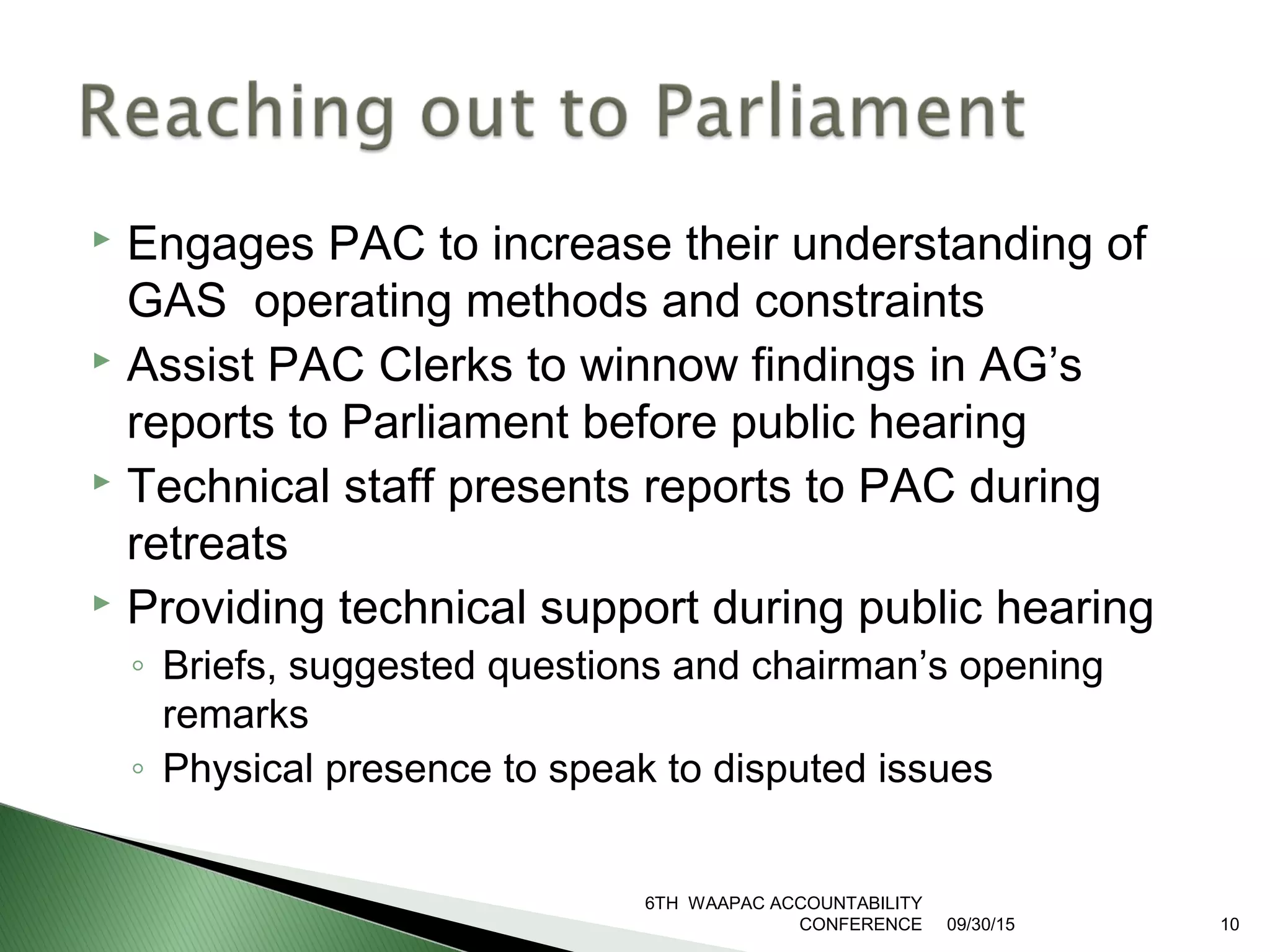

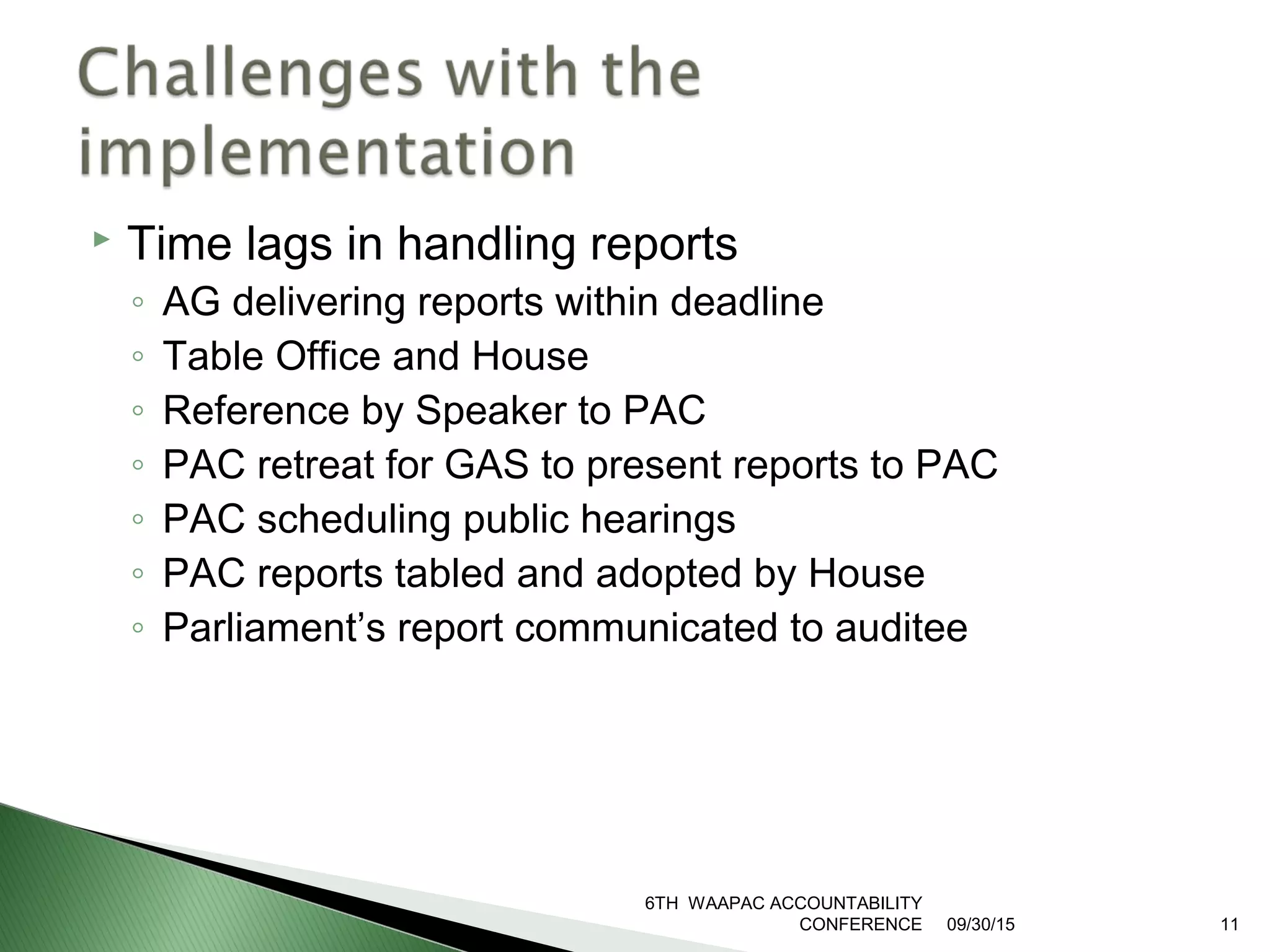

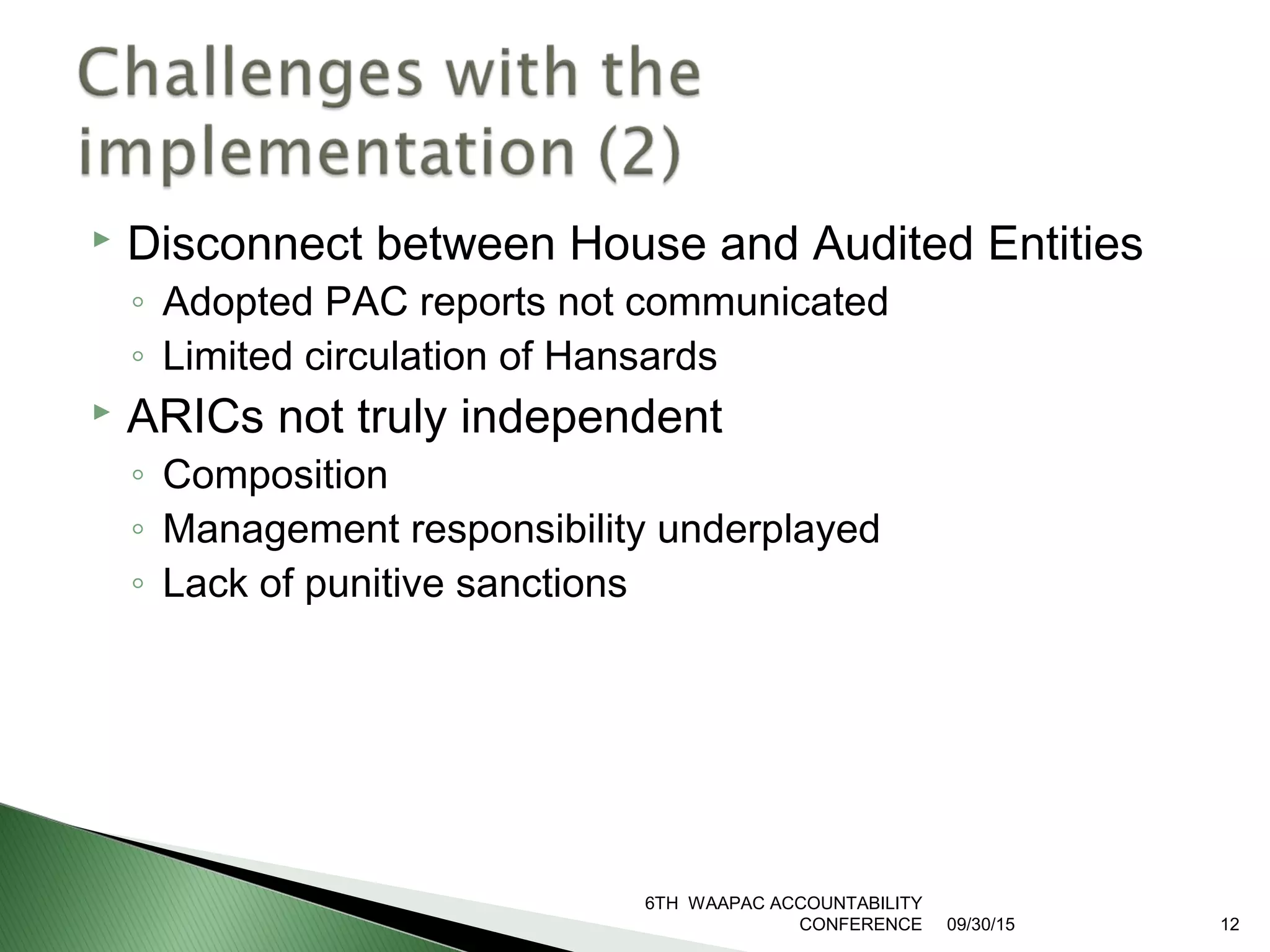

2. The Auditor-General submits audit reports to Parliament within 6 months of the previous fiscal year. However, there are challenges with the time it takes for reports to be reviewed by committees and for audited entities to implement recommendations.

3. Strategies are suggested to enhance implementation, including making Action Implementation Plans mandatory, establishing a special committee to address AG report findings, and improving collaboration between the AG office and oversight