Downloaded 1,254 times

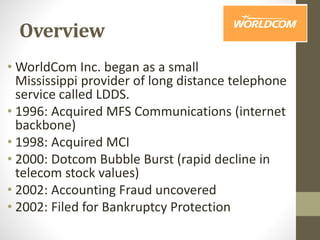

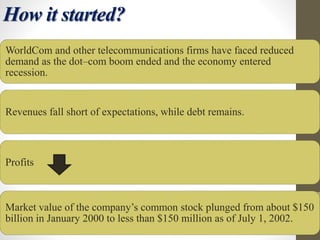

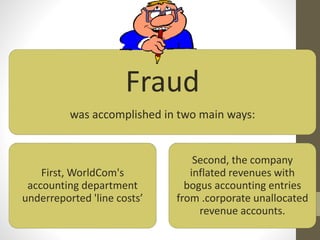

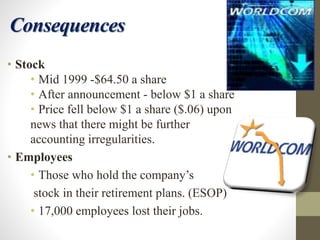

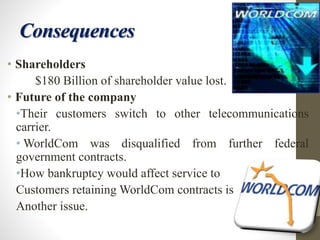

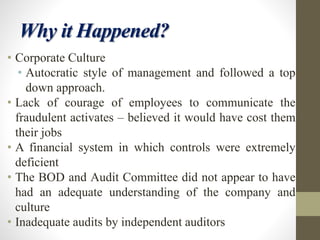

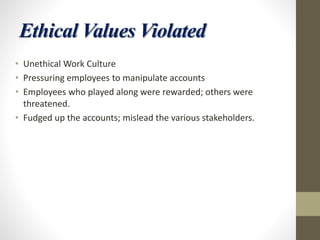

WorldCom engaged in fraudulent accounting practices that inflated revenues and hid expenses, which ultimately led to its bankruptcy. Top executives pressured employees to manipulate financial reports in order to meet expectations. When the fraud was uncovered, it resulted in massive job losses, the loss of $180 billion in shareholder value, and damage to the telecom industry. The fraudulent culture was driven by autocratic leadership, lack of transparency, and failure of oversight by the board and auditors.