Downloaded 16 times

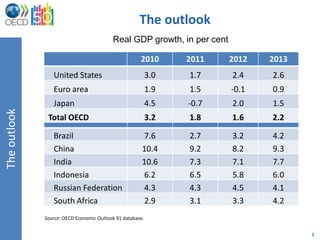

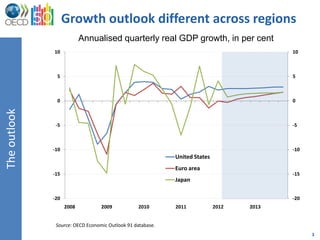

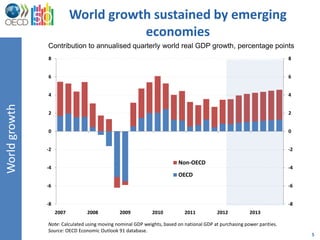

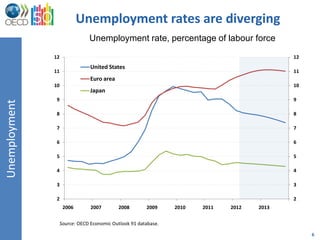

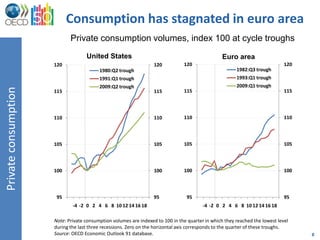

The economic outlook for OECD countries in 2012 shows moderate growth, with real GDP projected to increase by 1.6% across the total OECD region, while unemployment rates diverge significantly between member countries. Emerging economies are expected to sustain world growth, whereas the euro area continues to face weakened business confidence and stagnation in private consumption. Despite challenges, structural reforms and national policies aimed at boosting growth and competitiveness are underway to stabilize economic conditions.