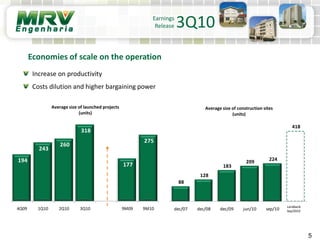

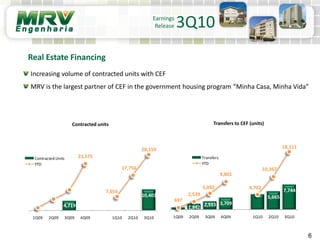

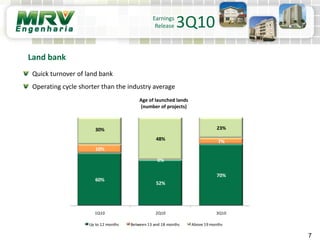

MRV reported its strongest third quarter results in the company's history in terms of net revenue, EBITDA, and net income. Key metrics such as EBITDA margin and net margin increased compared to the prior year. The company also saw increases in average project size, allowing for economies of scale. MRV maintained its position as the largest operator in Brazil's government housing program "Minha Casa Minha Vida" and operator with the largest number of contracted units.