1. MRV provides a corporate presentation covering its operational and financial results for April 2017.

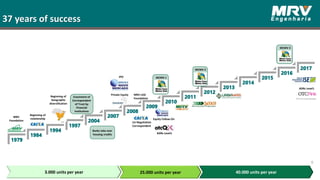

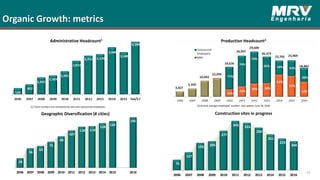

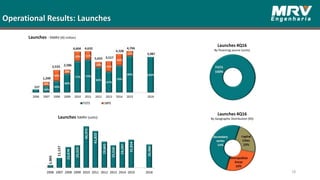

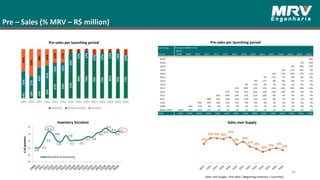

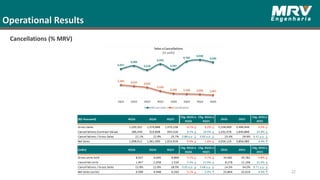

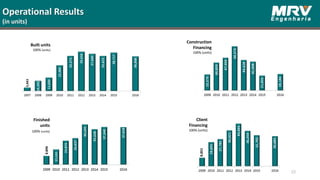

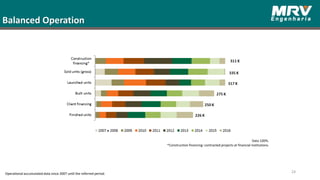

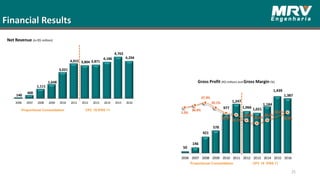

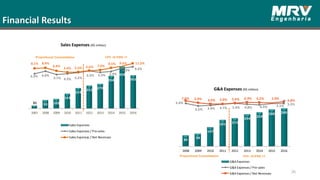

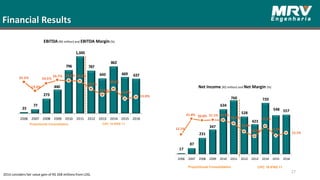

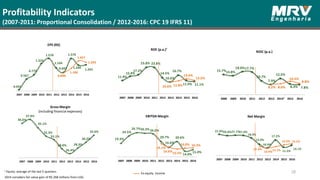

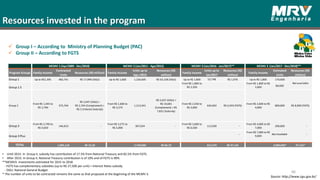

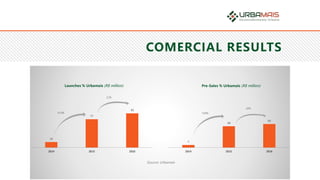

2. The presentation shows consistent growth in key metrics such as landbank, launches, pre-sales, revenue and earnings over several years from 2006 to 2016.

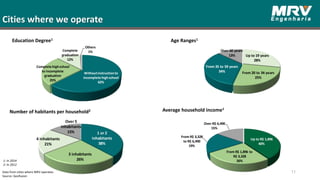

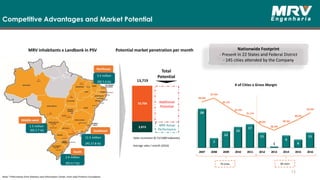

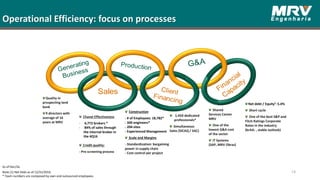

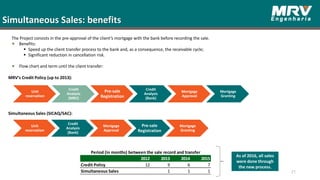

3. MRV has expanded its geographic footprint from 28 cities in 2006 to 145 cities currently, while maintaining operational efficiency through scale, standardization and cost control.