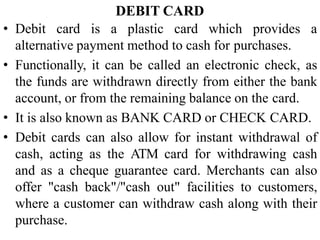

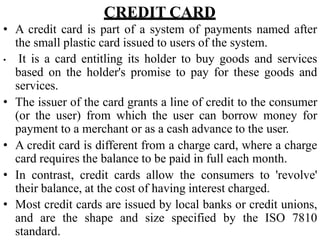

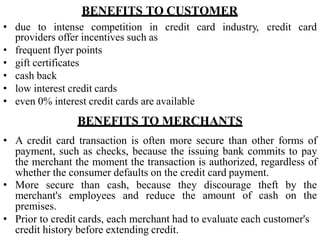

The document discusses electronic banking and differences between debit cards and credit cards. It provides details on debit cards, how they function as electronic checks withdrawing funds directly from a bank account. Credit cards are also discussed, how they allow users to revolve a balance and are charged interest. Benefits of credit cards for customers and merchants are outlined, such as incentives for customers and security compared to cash for merchants.

![[Slideshare] Evolution of B2B Payments](https://cdn.slidesharecdn.com/ss_thumbnails/slideshareevolutionofb2bpayments-150327100722-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Electronic fund trasfer [Mahak Dhakar]500048604](https://cdn.slidesharecdn.com/ss_thumbnails/electronicfundtrasfermahakdhakar500048604-171121150058-thumbnail.jpg?width=640&height=640&fit=bounds)