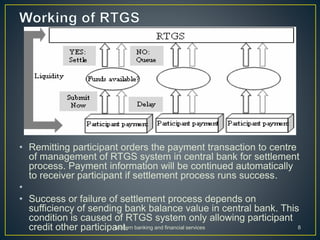

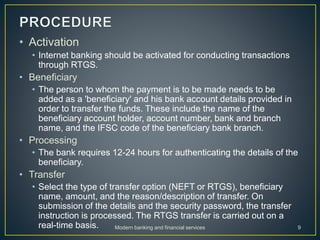

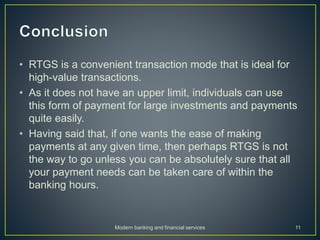

This document discusses Real Time Gross Settlement (RTGS) systems. It begins with background on RTGS, including that the first system was launched in the US in 1970. It then defines RTGS as a funds transfer mechanism that allows for real-time money transfers between banks on a gross basis, without aggregation. The document outlines why RTGS is used, how payments are made through RTGS including required information, how the settlement process works, key features of RTGS transactions, and concludes with references.

![Electronic fund trasfer [Mahak Dhakar]500048604](https://cdn.slidesharecdn.com/ss_thumbnails/electronicfundtrasfermahakdhakar500048604-171121150058-thumbnail.jpg?width=640&height=640&fit=bounds)