Downloaded 84 times

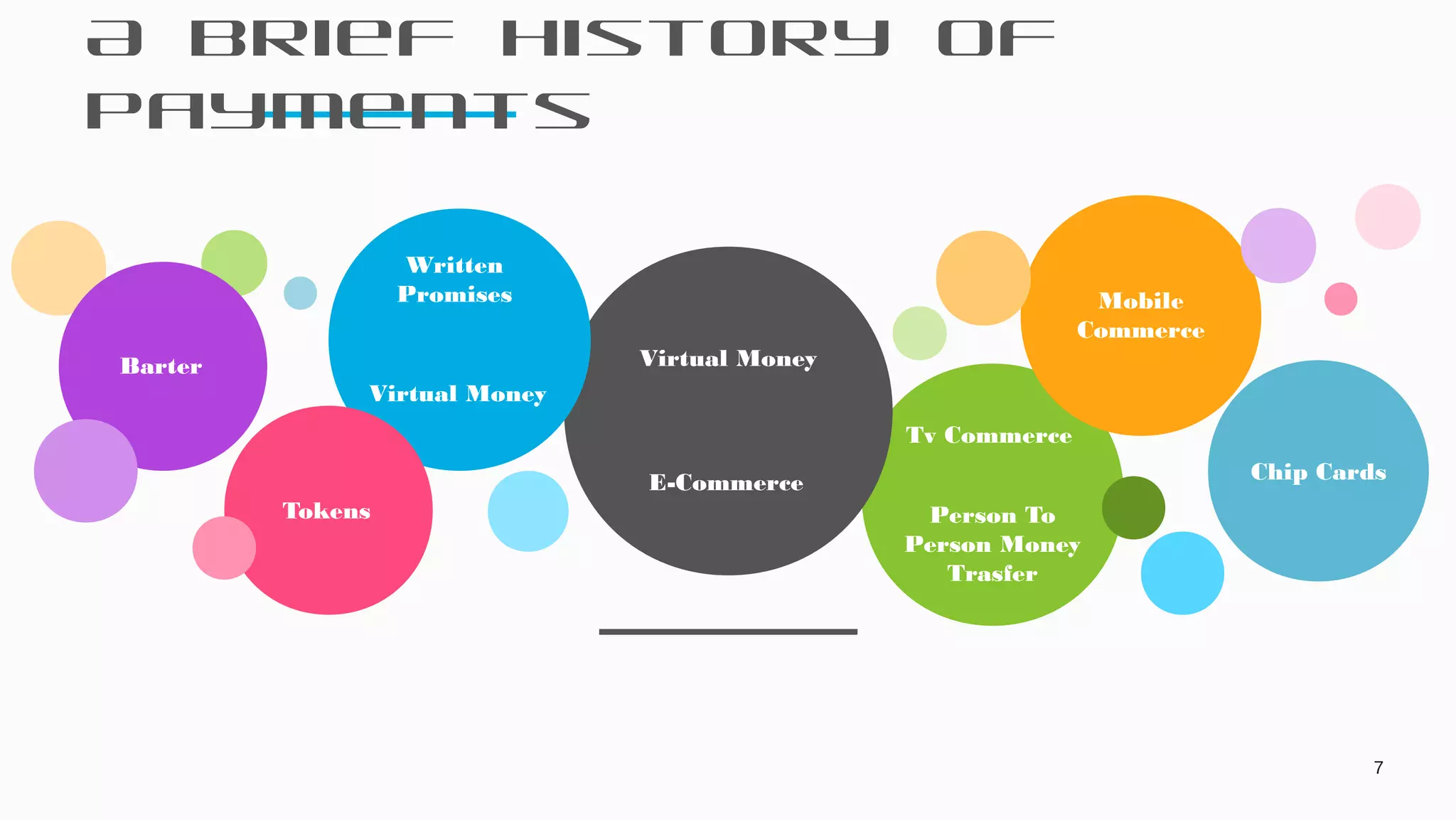

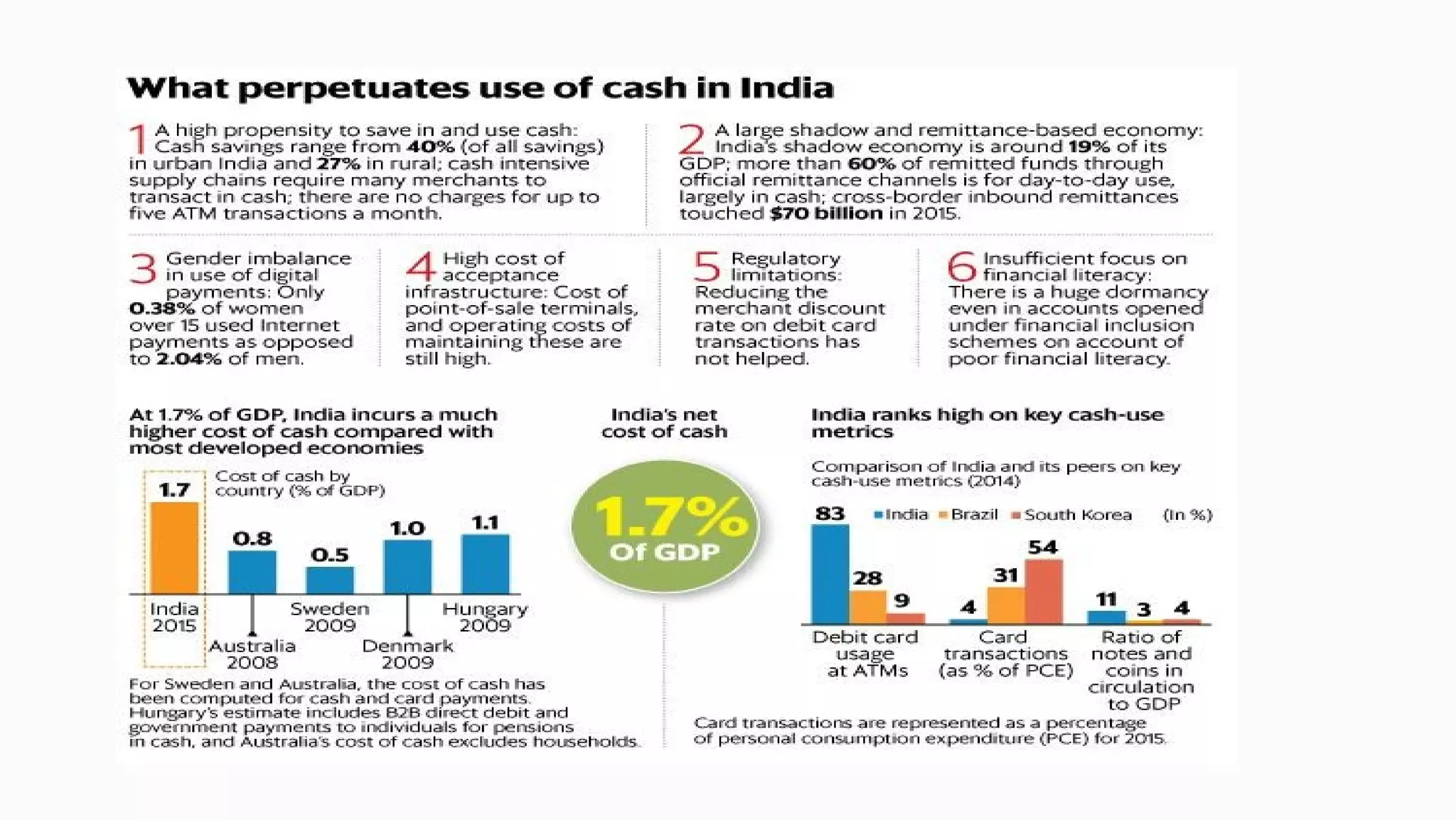

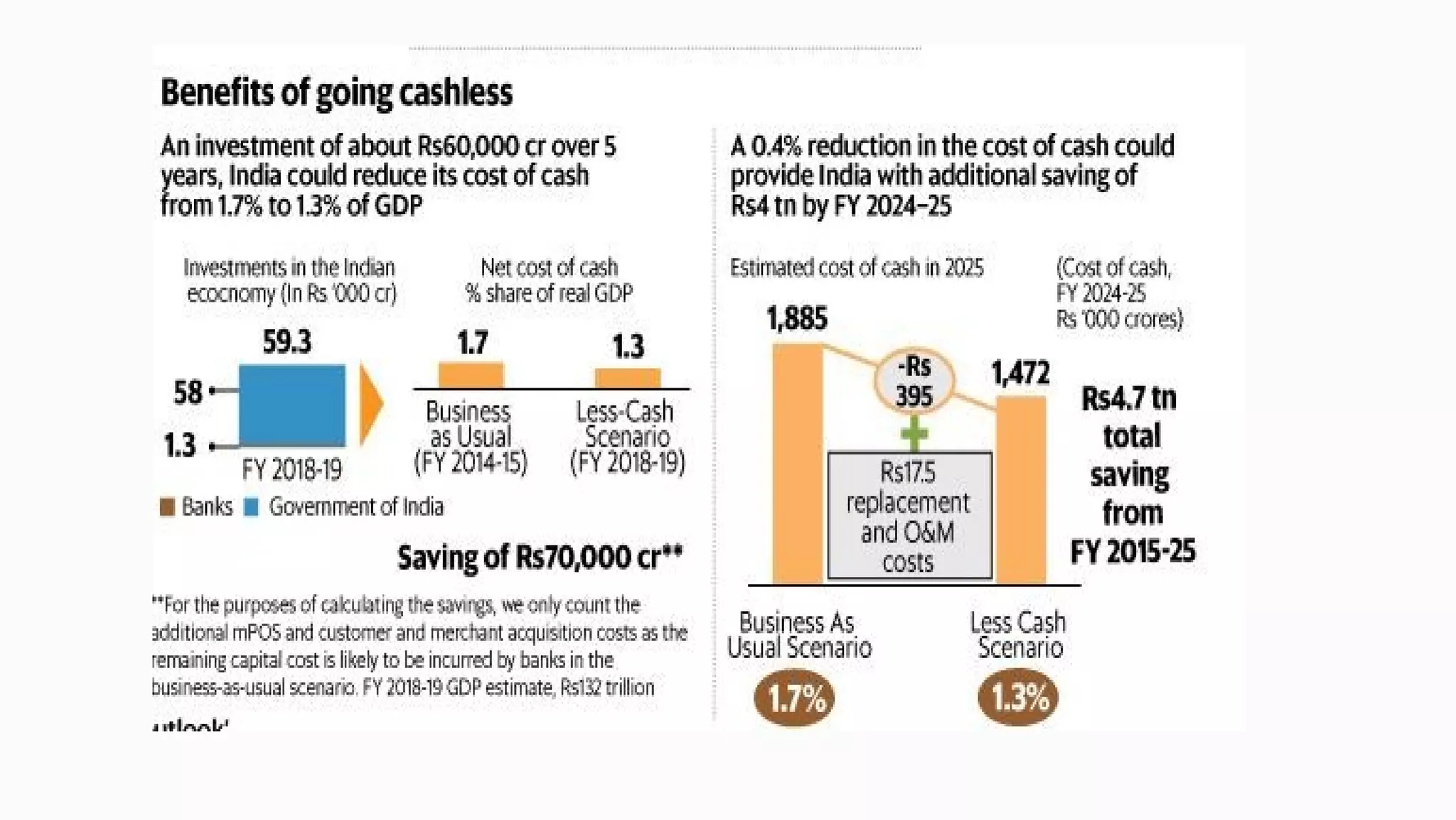

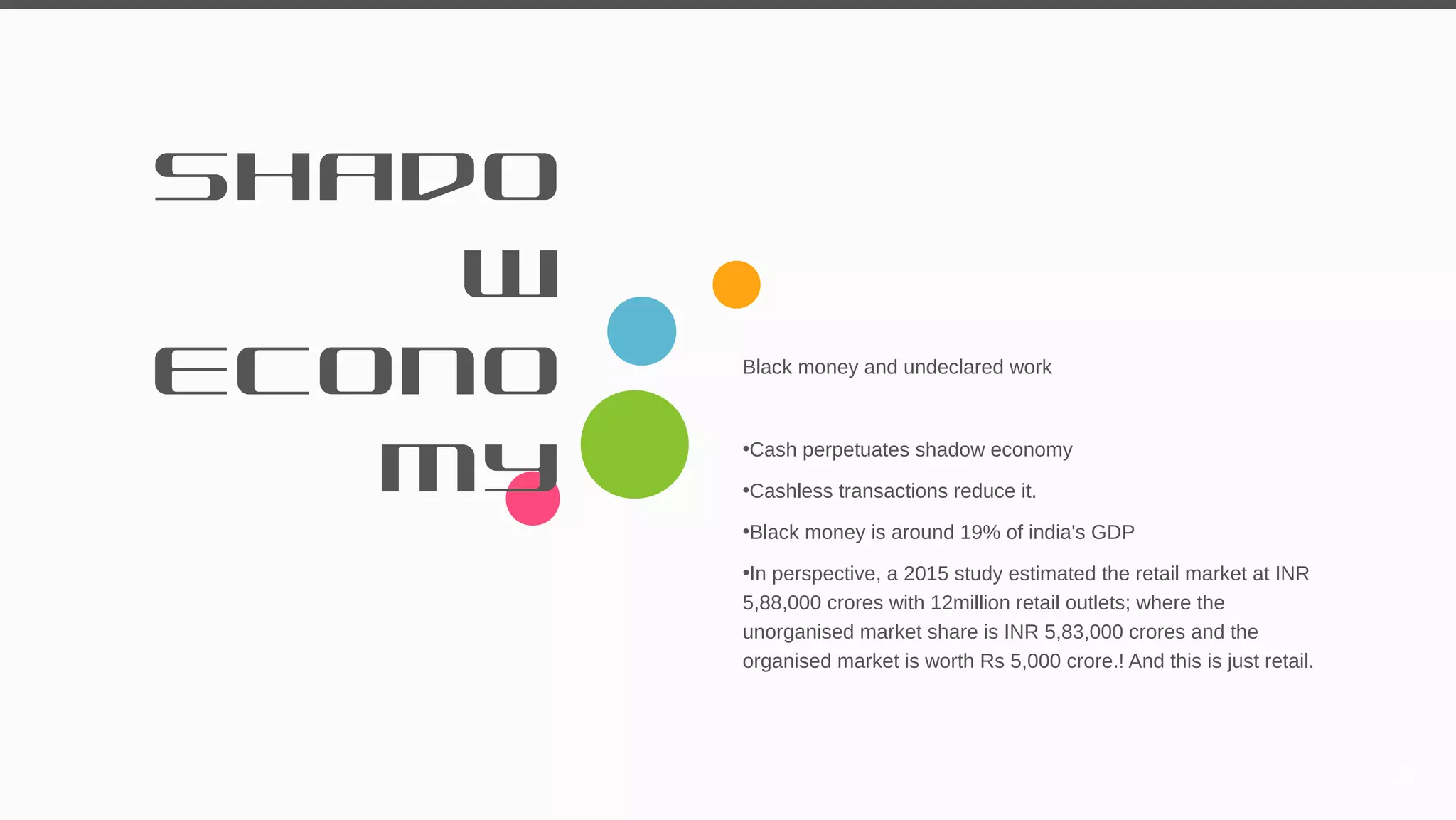

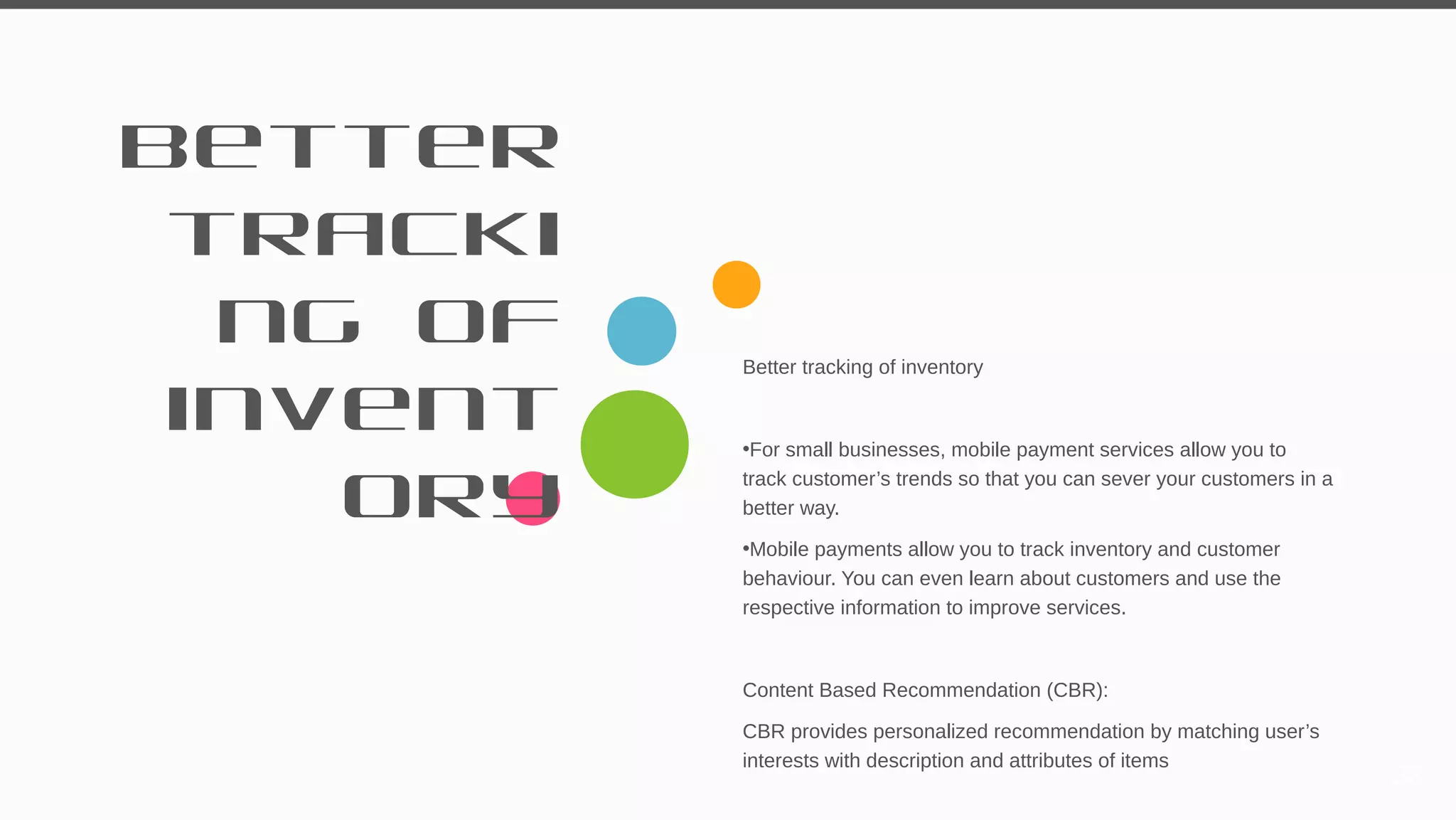

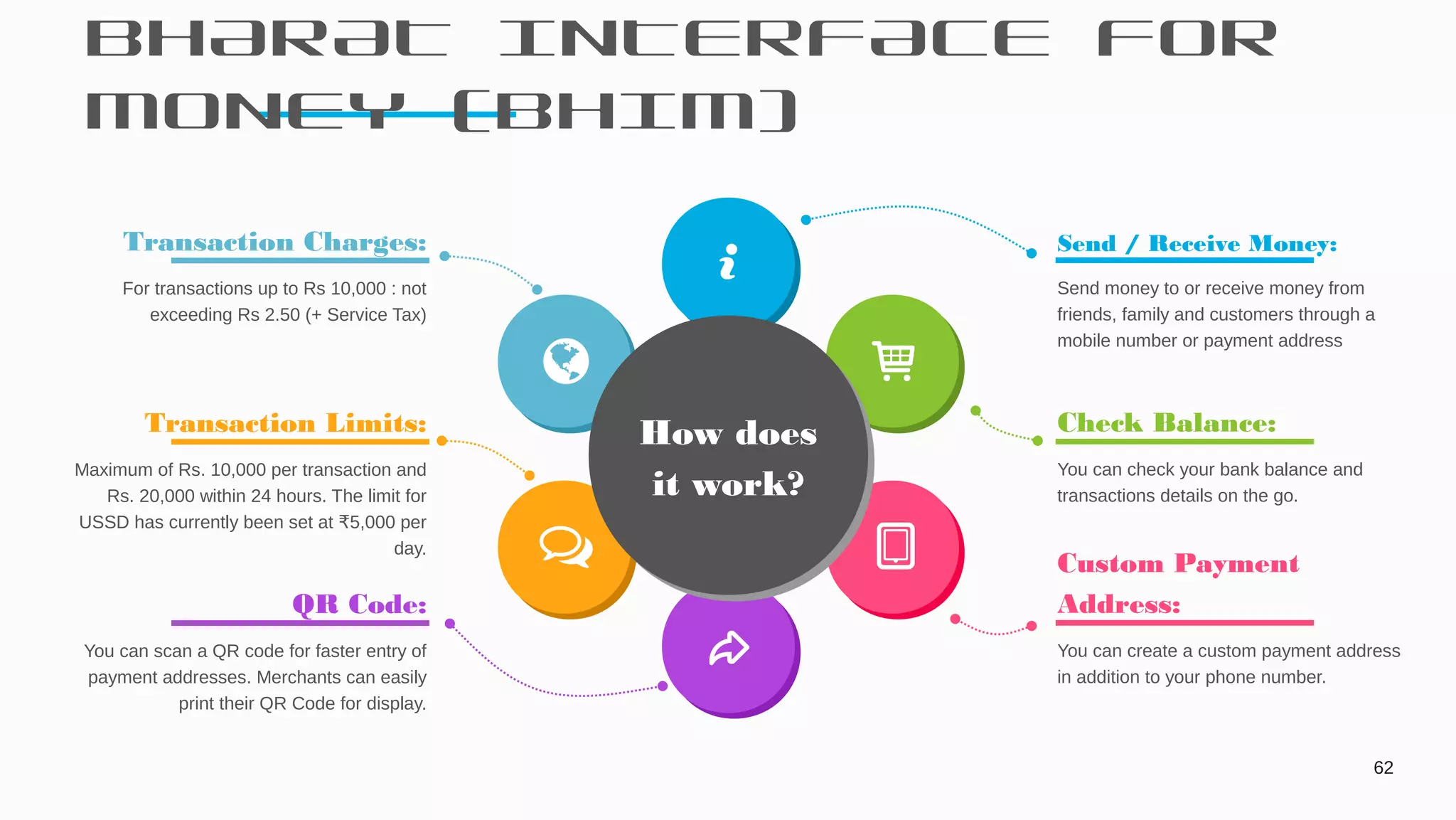

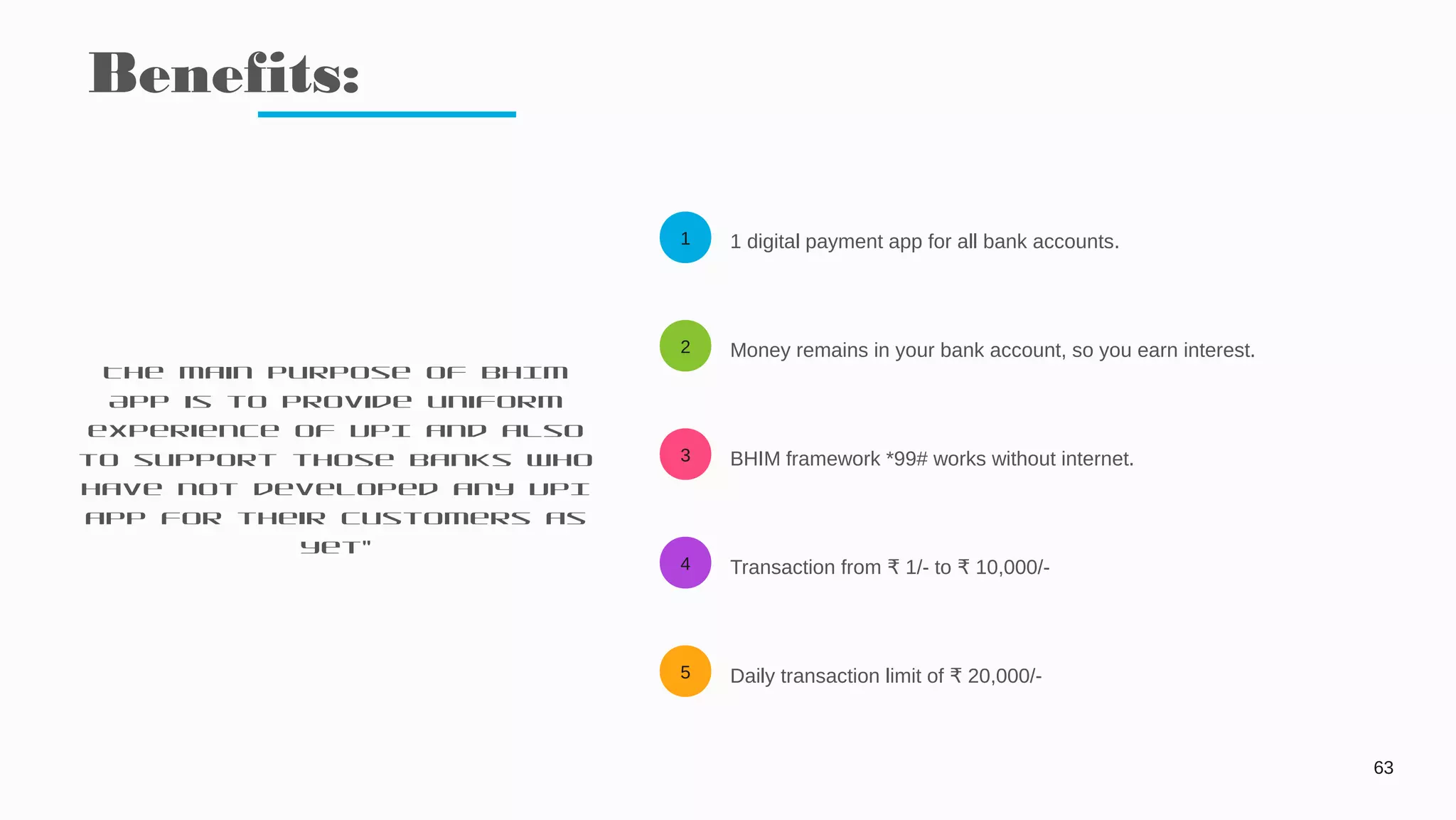

The document discusses the evolution of payment systems, highlighting the shift from traditional barter methods to digital payments, including mobile commerce and e-wallets. It emphasizes the benefits of a cashless economy in India, such as increased financial inclusion, tracking of transactions, and job creation, while also addressing challenges like cyber security and fraud. Additionally, it outlines initiatives and government programs aimed at promoting digital financial literacy and usage among citizens.