Downloaded 204 times

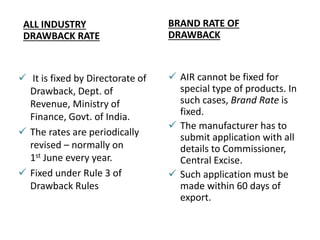

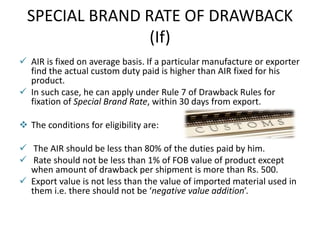

This document discusses India's duty drawback procedures. Duty drawback allows exporters to obtain a refund of customs duties paid on imported goods that are later exported or incorporated into exported goods. It is governed by the Customs Act of 1962 and aims to promote exports. There are two categories of duty drawback: drawback on re-exported imported goods and drawback on goods manufactured from imported materials for export. Exporters must follow certain procedures to claim duty drawback, including endorsing shipping bills and retaining claims, and there are also rules around payment and recovery of drawback amounts.