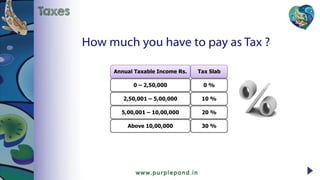

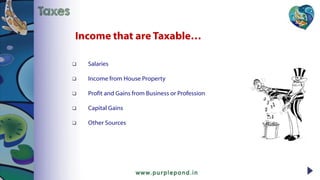

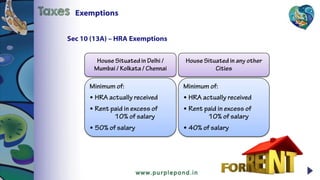

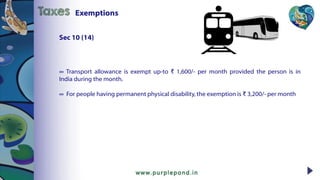

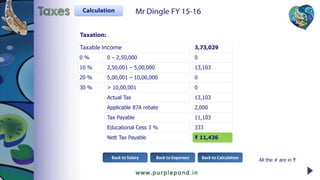

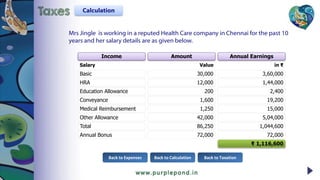

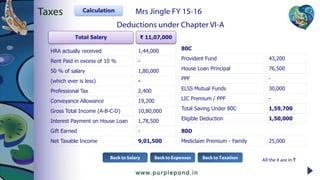

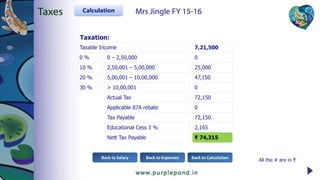

The document provides an extensive overview of tax regulations, including tax slabs, exemptions, and deductions available to taxpayers in India. It outlines various categories of income and expenses that can affect taxable income, as well as detailed explanations of deduction sections (like 80C and 80D) for specific investments and expenditures. The document also presents example calculations for two individuals, illustrating how different salaries and expenses impact tax liabilities.