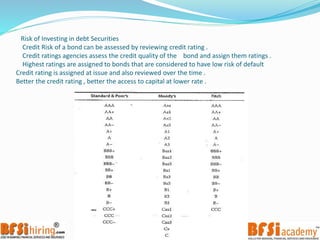

The document provides a comprehensive overview of debt securities, including definitions, types such as bonds and coupon rates, and key concepts like interest rates and risks associated with investing. It discusses various bond features, embedded provisions like callable and convertible bonds, and market dynamics in primary and secondary markets, as well as the valuation of debt securities. It also highlights the risks of investing in debt securities, including credit and interest rate risks, and explains the process of securitization and its implications.