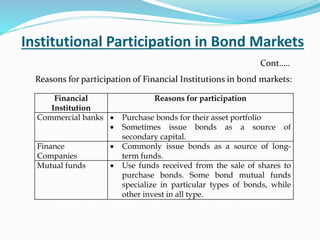

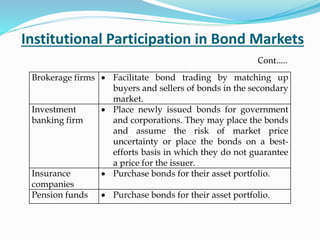

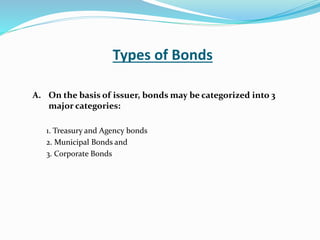

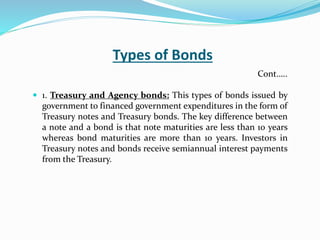

Downloaded 38 times

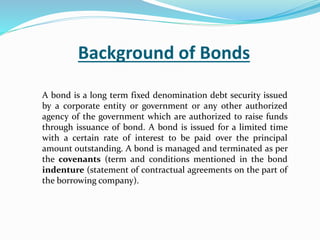

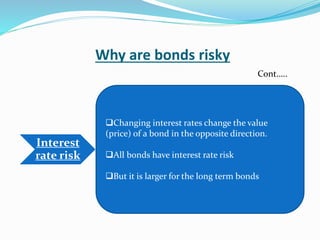

![Termination or Retirement of a Bond

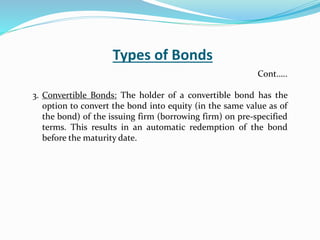

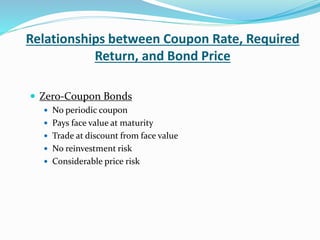

For example, in the above case if 80% of Faith 11 (BD) Ltd bonds

were converted (80% of Tk. 2000 or Tk. 1600 in this example)

into the common stocks of the firm, then the bond holders

would have received stocks of the firm in as per the market price

of the stock at the time of conversion. Therefore, if the market

price is Tk. 120 per share, the bond holders will receive

(1600/120) 13 share of the firm plus Tk. 440 [Tk. 400 + (Tk. 1600

– Tk. 120*13)] in cash.

Cont…..](https://image.slidesharecdn.com/bondmarkets-171218085852/85/Bond-markets-15-320.jpg)

This document provides an overview of bond markets, including definitions and key features of bonds. Some main points: - Bonds are long-term debt securities issued by governments or corporations to raise funds. They pay a fixed rate of interest over a set period of time. - Key features of bonds include their long-term nature, fixed face value, fixed interest payments, and indenture outlining terms. Additional features can include trustees, covenants, and repayment procedures. - Bonds are typically retired at maturity when the principal is repaid, but can also be terminated through conversion to equity or gradual withdrawal over time using methods like sinking funds or serial bonds.