Download to read offline

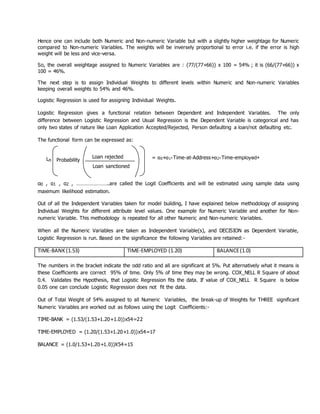

This document discusses using a hybrid modeling approach combining decision trees and logistic regression to develop a credit scoring model for retail loans. It presents a case study where this approach was tested on real loan data. Key points: - A decision tree was first used to identify important borrower characteristics and assign initial weights. Logistic regression was then used to compute odds ratios and assign refined weights within each characteristic. - This iterative process determined weights for both numeric factors like time at bank and non-numeric factors like occupation. Binning of numeric variables was done automatically using additional decision trees. - When tested on loan application data, the hybrid model achieved a classification accuracy of around 80%, higher than single models. This approach provides an

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)