Downloaded 18 times

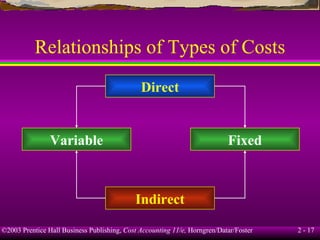

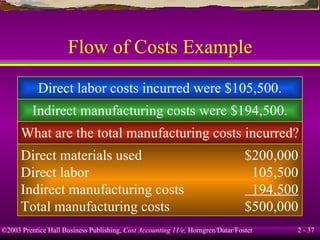

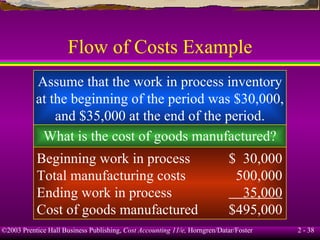

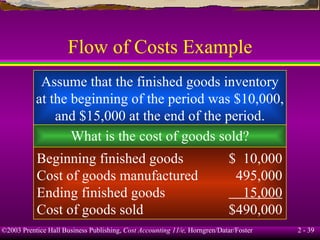

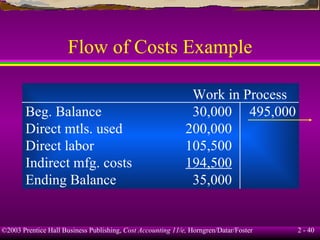

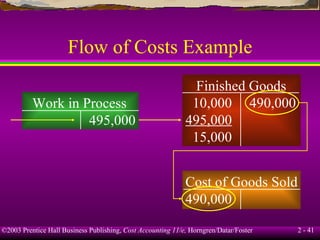

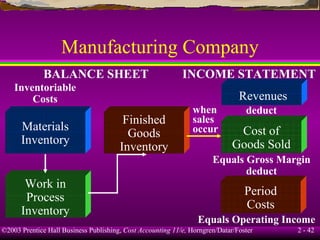

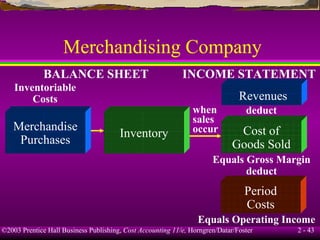

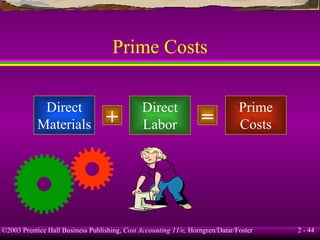

This chapter discusses key cost accounting concepts including defining costs, distinguishing between direct and indirect costs, explaining cost behavior patterns like variable and fixed costs, and differentiating inventoriable and period costs. It also covers how costs flow through manufacturing companies and are classified for financial reporting purposes versus internal decision making. The key purposes of cost accounting are to calculate product costs, obtain cost information, and analyze that information for managing business operations.