Downloaded 13 times

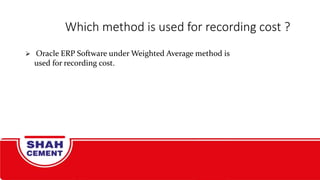

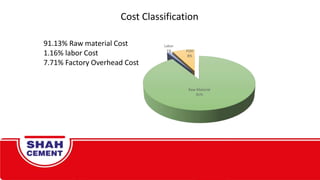

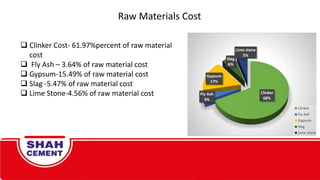

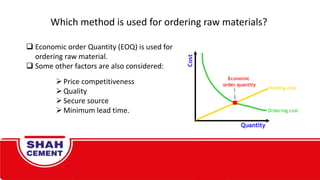

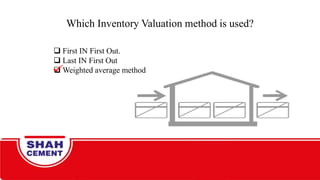

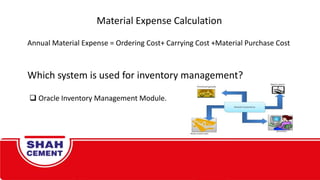

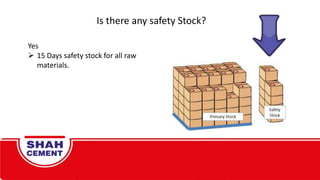

The document discusses cost accounting methods used by a large cement manufacturing company in Bangladesh. It details how the company calculates its cost of goods sold using a weighted average method in an Oracle ERP system. The major cost components are raw materials (91%), labor (1%), and factory overhead (8%). Raw material costs are further broken down by type of material. The company uses economic order quantity and safety stock principles for raw material inventory management. Factory overhead is allocated using primary and secondary distribution methods before being absorbed into finished goods.

![Chapter 3.pptbghtyuiooplmkjl;p[-=]\'4541](https://cdn.slidesharecdn.com/ss_thumbnails/chapter3-250406090922-a5426289-thumbnail.jpg?width=640&height=640&fit=bounds)