Job Order and

JobOrder and Process

Process Costing Methods

Costing Methods

o Job-Order Costing vs. Process Costing

Job-Order Costing vs. Process Costing

o Job-order costing

Job-order costing is used for companies that

produce different products each period

produce different products each period.

• Costs are accumulated

accumulated for each job.

o Process costing

Process costing is used for companies that

produce many identical units of a single product

produce many identical units of a single product

for long periods of time

for long periods of time.

• Costs are accumulated

accumulated for each manufacturing

department.

04/06/25

By Megersa H. 2023 2

3.

Key Job-Order CostingDocuments

Key Job-Order Costing Documents

Material requisitions:

Material requisitions: request materials for

production and support direct materials costs

charged to each job.

Time cards or time tickets:

Time cards or time tickets: record direct labour

hours used in production and support direct

labour costs charged to each job.

Job cost sheets

Job cost sheets are the most important job

costing document.

• They summarize all of the key information

key information about the

job and accumulate

accumulate total direct materials costs,

total direct labour costs and overhead costs applied

to the job to determine the total costs for

total costs for the job.

04/06/25

By Megersa H. 2023 3

4.

Distinguish B/n

Distinguish B/nProcess

Process and Job-order Costing

and Job-order Costing

a)

a) Process Costing;

Process Costing;

• A company produces many units of a single

product.

• One unit of product is indistinguishable

indistinguishable from other

units of product.

• The identical nature

identical nature of each unit of product

enables assigning the same average cost

assigning the same average cost per

unit.

b)

b) Job Order Costing

Job Order Costing

• Many different products

different products are produced each period.

• Products are manufactured to order

manufactured to order.

• The unique nature of each order requires tracing

tracing or

allocating

allocating costs to each job, and maintaining cost

maintaining cost

records

records for each job. 04/06/25

By Megersa H. 2023 4

5.

Job Ordering Costing- overview

Job Ordering Costing - overview

04/06/25

By Megersa H. 2023 5

Job

Job

No.1

No.1

Job

Job

No.2

No.2

Job

Job

No.3

No.3

Charge

Charge

direct

direct

material

material

and

and direct

direct

labor costs

labor costs

to each job

to each job

as work is

as work is

performed.

performed.

MOH

MOH

Direct

Direct

Labor

Labor

Direct

Direct

Material

Material

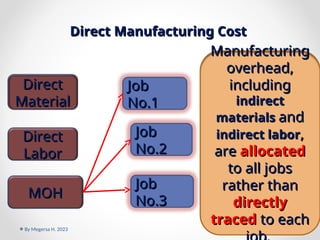

6.

Direct Manufacturing Cost

DirectManufacturing Cost

04/06/25

By Megersa H. 2023 6

Job

Job

No.1

No.1

Job

Job

No.2

No.2

Job

Job

No.3

No.3

Manufacturing

Manufacturing

overhead,

overhead,

including

including

indirect

indirect

materials

materials and

and

indirect labor

indirect labor,

,

are

are allocated

allocated

to all jobs

to all jobs

rather than

rather than

directly

directly

traced

traced to each

to each

MOH

MOH

Direct

Direct

Labor

Labor

Direct

Direct

Material

Material

7.

Features of JobOrder Costing System

Features of Job Order Costing System

• Each Job is treated as a cost unit

• All costs are accumulated and ascertained for

each job

• Each job is unique

• Each job is executed as per customer’s

specifications.

• A separate Job cost sheet or Job card is used for

each job and is assigned a certain number by

which the job is identified.

04/06/25

By Megersa H. 2023 7

8.

Job Costing inManufacturing Firms

Job Costing in Manufacturing Firms

• Job Cost Sheet

Job Cost Sheet

• It is a document that records

records and accumulates

accumulates

all costs assigned to a specific job, starting when

work begins.

• The job may be a product

product, service

service or batch

batch of

products.

• The job cost sheet can be in paper

in paper or electronic

electronic

form.

• A simplified job cost sheet follows:

04/06/25

By Megersa H. 2023 8

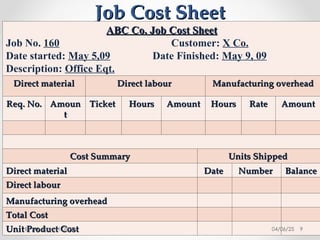

9.

Job Cost Sheet

JobCost Sheet

ABC Co. Job Cost Sheet

ABC Co. Job Cost Sheet

Job No. 160 Customer: X Co.

Date started: May 5,09 Date Finished: May 9, 09

Description: Office Eqt.

Direct material

Direct material Direct labour

Direct labour Manufacturing overhead

Manufacturing overhead

Req. No.

Req. No. Amoun

Amoun

t

t

Ticket

Ticket Hours

Hours Amount

Amount Hours

Hours Rate

Rate Amount

Amount

Cost Summary

Cost Summary Units Shipped

Units Shipped

Direct material

Direct material Date

Date Number

Number Balance

Balance

Direct labour

Direct labour

Manufacturing overhead

Manufacturing overhead

Total Cost

Total Cost

Unit Product Cost

Unit Product Cost 04/06/25 9

By Megersa H. 2023

10.

Measuring Direct MaterialCost

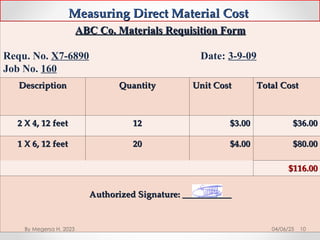

Measuring Direct Material Cost

ABC Co. Materials Requisition Form

ABC Co. Materials Requisition Form

Requ. No. X7-6890 Date: 3-9-09

Job No. 160

Description

Description Quantity

Quantity Unit Cost

Unit Cost Total Cost

Total Cost

2 X 4, 12 feet

2 X 4, 12 feet 12

12 $3.00

$3.00 $36.00

$36.00

1 X 6, 12 feet

1 X 6, 12 feet 20

20 $4.00

$4.00 $80.00

$80.00

$116.00

$116.00

Authorized Signature: ___________

Authorized Signature: ___________

04/06/25 10

By Megersa H. 2023

11.

Measuring Direct MaterialCost

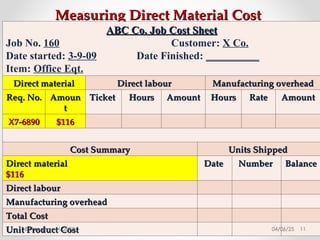

Measuring Direct Material Cost

ABC Co. Job Cost Sheet

ABC Co. Job Cost Sheet

Job No. 160 Customer: X Co.

Date started: 3-9-09 Date Finished: __________

Item: Office Eqt.

Direct material

Direct material Direct labour

Direct labour Manufacturing overhead

Manufacturing overhead

Req. No.

Req. No. Amoun

Amoun

t

t

Ticket

Ticket Hours

Hours Amount

Amount Hours

Hours Rate

Rate Amount

Amount

X7-6890

X7-6890 $116

$116

Cost Summary

Cost Summary Units Shipped

Units Shipped

Direct material

Direct material

$116

$116

Date

Date Number

Number Balance

Balance

Direct labour

Direct labour

Manufacturing overhead

Manufacturing overhead

Total Cost

Total Cost

Unit Product Cost

Unit Product Cost 04/06/25 11

By Megersa H. 2023

12.

Measuring Direct LabourCost

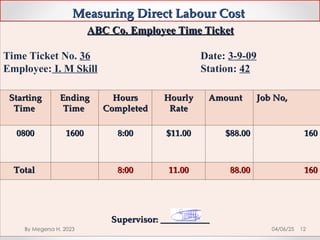

Measuring Direct Labour Cost

ABC Co. Employee Time Ticket

ABC Co. Employee Time Ticket

Time Ticket No. 36 Date: 3-9-09

Employee: I. M Skill Station: 42

Starting

Starting

Time

Time

Ending

Ending

Time

Time

Hours

Hours

Completed

Completed

Hourly

Hourly

Rate

Rate

Amount

Amount Job No,

Job No,

0800

0800 1600

1600 8:00

8:00 $11.00

$11.00 $88.00

$88.00 160

160

Total

Total 8:00

8:00 11.00

11.00 88.00

88.00 160

160

Supervisor: ___________

Supervisor: ___________

04/06/25 12

By Megersa H. 2023

13.

Job Order CostAccounting

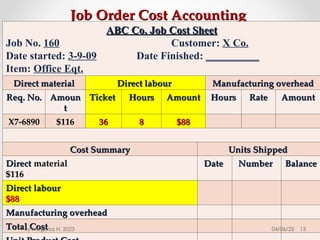

Job Order Cost Accounting

ABC Co. Job Cost Sheet

ABC Co. Job Cost Sheet

Job No. 160 Customer: X Co.

Date started: 3-9-09 Date Finished: __________

Item: Office Eqt.

Direct material

Direct material Direct labour

Direct labour Manufacturing overhead

Manufacturing overhead

Req. No.

Req. No. Amoun

Amoun

t

t

Ticket

Ticket Hours

Hours Amount

Amount Hours

Hours Rate

Rate Amount

Amount

X7-6890

X7-6890 $116

$116 36

36 8

8 $88

$88

Cost Summary

Cost Summary Units Shipped

Units Shipped

Direct

Direct material

material

$116

$116

Date

Date Number

Number Balance

Balance

Direct labour

Direct labour

$88

$88

Manufacturing overhead

Manufacturing overhead

Total Cost

Total Cost 04/06/25 13

By Megersa H. 2023

14.

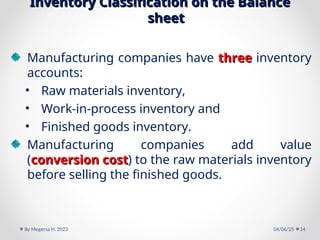

Inventory Classification onthe Balance

Inventory Classification on the Balance

sheet

sheet

Manufacturing companies have three

three inventory

accounts:

• Raw materials inventory,

• Work-in-process inventory and

• Finished goods inventory.

Manufacturing companies add value

(conversion cost

conversion cost) to the raw materials inventory

before selling the finished goods.

04/06/25

By Megersa H. 2023 14

Actual Manufacturing Overheadand

Actual Manufacturing Overhead and

Manufacturing Overhead Applied

Manufacturing Overhead Applied

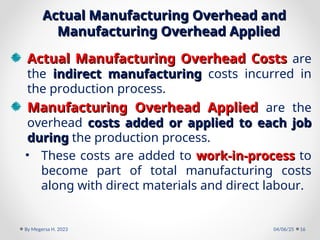

Actual Manufacturing Overhead Costs

Actual Manufacturing Overhead Costs are

the indirect manufacturing

indirect manufacturing costs incurred in

the production process.

Manufacturing Overhead Applied

Manufacturing Overhead Applied are the

overhead costs added or applied to each job

costs added or applied to each job

during

during the production process.

• These costs are added to work-in-process

work-in-process to

become part of total manufacturing costs

along with direct materials and direct labour.

04/06/25

By Megersa H. 2023 16

17.

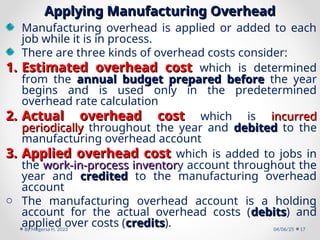

Applying Manufacturing Overhead

ApplyingManufacturing Overhead

Manufacturing overhead is applied or added to each

job while it is in process.

There are three kinds of overhead costs consider:

1.

1. Estimated overhead cost

Estimated overhead cost which is determined

from the annual budget prepared before

annual budget prepared before the year

begins and is used only in the predetermined

overhead rate calculation

2.

2. Actual overhead cost

Actual overhead cost which is incurred

incurred

periodically

periodically throughout the year and debited

debited to the

manufacturing overhead account

3.

3. Applied overhead cost

Applied overhead cost which is added to jobs in

the work-in-process inventor

work-in-process inventory account throughout the

year and credited

credited to the manufacturing overhead

account

o The manufacturing overhead account is a holding

account for the actual overhead costs (debits

debits) and

applied over costs (credits

credits). 04/06/25

By Megersa H. 2023 17

18.

Cont…

Cont…

Actual overhead costsincurred are now flow

through the Manufacturing Overhead account

instead of directly into the work-in-process

inventory.

The balance in the manufacturing

balance in the manufacturing overhead

account may be a debit or credit, depending on

whether:

1)

1) Debit

Debit if the overhead applied is less than

less than the

actual overhead costs incurred (under-applied)

2)

2) Credit

Credit if overhead applied is more than

more than the

actual overhead costs incurred (over-applied).

04/06/25

By Megersa H. 2023 18

19.

Cont…

Cont…

Some companies mayuse departmental

predetermined overhead rates rather than the

single plant-wide predetermined overhead rate

single plant-wide predetermined overhead rate

shown here in an effort to make the overhead

application process more accurate.

The balance in the overhead account is:

• A favourable variance if it is over-applied

• An unfavourable variance if it is under-applied

04/06/25

By Megersa H. 2023 19

20.

The journal entriesto record the flow of costs

The journal entries to record the flow of costs

through the inventory accounts are:

through the inventory accounts are:

A.

A. Purchase of raw materials

Purchase of raw materials

• Raw material inventory------------------- xxx

• Accounts payable------------------------------------- xxx

B.

B. Issue raw materials

Issue raw materials

• Work-in-process inventory (direct) -------xxx

• Manufacturing overhead (indirect)-------- xxx

• Raw materials inventory------------------------------xxx

o Labour costs incurred

Labour costs incurred

• Work-in-process inventory (direct)--------- xxx

• Manufacturing overhead (indirect)--------- xxx

• Wages and salaries payable---------------------------

xxx 04/06/25

By Megersa H. 2023 20

Cont…

Cont…

E) Manufacturing overheadapplied

E) Manufacturing overhead applied

• Work-in-process inventory----------------- xxx

• Manufacturing overhead------------------------------- xxx

F) Goods are completed

F) Goods are completed

• Finished goods inventory------------------- xxx

• Work-in-process inventory ---------------------------xxx

G) Finished goods are sold

G) Finished goods are sold

• Cash or accounts receivable ----------------xxx

• Sales ----------------------------------------------------xxx

• Cost of goods sold ----------------------------XXX

• Finished goods inventory ------------------------------xxx

04/06/25

By Megersa H. 2023 22

23.

Cont…

Cont…

H) Close balancein overhead account

H) Close balance in overhead account

i.

i.Under-applied

Under-applied

• Cost of goods sold -----------------------xxx

• Manufacturing overhead ------------------------xxx

OR

ii.Over-applied

• Manufacturing overhead-------------------- xxx

• Cost of goods sold-------------------------------------

xxx

04/06/25

By Megersa H. 2023 23

24.

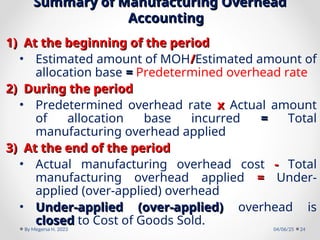

Summary of ManufacturingOverhead

Summary of Manufacturing Overhead

Accounting

Accounting

1)

1) At the beginning of the period

At the beginning of the period

• Estimated amount of MOH/

/Estimated amount of

allocation base =

= Predetermined overhead rate

2)

2) During the period

During the period

• Predetermined overhead rate x

x Actual amount

of allocation base incurred =

= Total

manufacturing overhead applied

3)

3) At the end of the period

At the end of the period

• Actual manufacturing overhead cost -

- Total

manufacturing overhead applied =

= Under-

applied (over-applied) overhead

• Under-applied (over-applied)

Under-applied (over-applied) overhead is

closed

closed to Cost of Goods Sold.

04/06/25

By Megersa H. 2023 24

25.

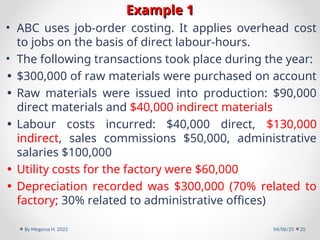

Example 1

Example 1

•ABC uses job-order costing. It applies overhead cost

to jobs on the basis of direct labour-hours.

• The following transactions took place during the year:

• $300,000 of raw materials were purchased on account

• Raw materials were issued into production: $90,000

direct materials and $40,000 indirect materials

• Labour costs incurred: $40,000 direct, $130,000

indirect, sales commissions $50,000, administrative

salaries $100,000

• Utility costs for the factory were $60,000

• Depreciation recorded was $300,000 (70% related to

factory; 30% related to administrative offices)

04/06/25

By Megersa H. 2023 25

26.

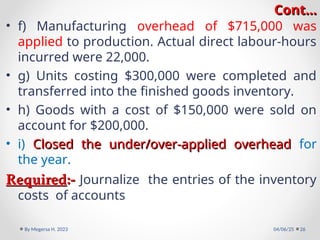

Cont…

Cont…

• f) Manufacturingoverhead of $715,000 was

applied to production. Actual direct labour-hours

incurred were 22,000.

• g) Units costing $300,000 were completed and

transferred into the finished goods inventory.

• h) Goods with a cost of $150,000 were sold on

account for $200,000.

• i) Closed the under/over-applied overhead

Closed the under/over-applied overhead for

the year.

Required

Required:-

:- Journalize the entries of the inventory

costs of accounts

04/06/25

By Megersa H. 2023 26

27.

Cont…

Cont…

Solutions

Solutions

a)Raw materials ------------------------300,000

oAccounts payable ---------------------------------300,000

b)Work in process-------------------- 90,000

a)Manufacturing overhead-------- 40,000

40,000

b)Raw materials ------------------------------------130,000

•Work in process----------------------- 40,000

o Manufacturing overhead ----------130,000

130,000

o Sales commission expense--------- 50,000

o Administrative salaries expense ----100,000

o Salaries and wage payable-----------------------

320,000

04/06/25

By Megersa H. 2023 27

28.

Cont…

Cont…

d) Manufacturing overhead-------------------60,000

60,000

•Accounts payable --------------------------------------------60,000

e) Manufacturing overhead --------------------210,000

210,000

•Depreciation expense -------------------------90,000

•Accumulated depreciation ----------------------------------300,000

f) Work in process --------------------------------715,000

•Manufacturing overhead------------------------------- (1

1) 715,000

g) Finished goods ----------------------------------300,000

•Work in process ---------------------------------------------300,000

h) Accounts receivable------------------------------ 200,000

•Sales ----------------------------------------------------------200,000

•Cost of goods sold ---------------------------------150,000

•Finished goods---------------------------------------------- 150,000

04/06/25 28

By Megersa H. 2023

29.

Cont…

Cont…

i) Manufacturing overhead------------------275,000

• Cost of goods sold -------------------------------------------

275,000

Manufacturing Overhead

Manufacturing Overhead

Actual

Actual Applied

Applied

(

(b

b)

)40,000

40,000

(

(c

c)

)130,000

130,000 715,000(

715,000(f

f)

)

(

(d

d)

)60,000

60,000

(

(e

e)

)210,000

210,000

440,000 275,000

440,000 275,000 over-applied

over-applied

04/06/25

By Megersa H. 2023 29

30.

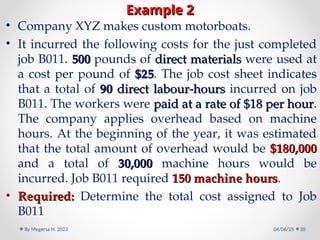

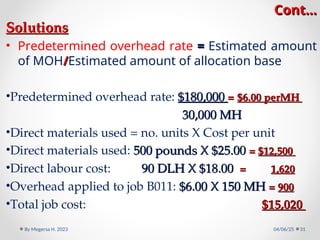

Example 2

Example 2

•Company XYZ makes custom motorboats.

• It incurred the following costs for the just completed

job B011. 500

500 pounds of direct materials

direct materials were used at

a cost per pound of $25

$25. The job cost sheet indicates

that a total of 90

90 direct labour-hours

direct labour-hours incurred on job

B011. The workers were paid at a rate of $18 per hour

paid at a rate of $18 per hour.

The company applies overhead based on machine

hours. At the beginning of the year, it was estimated

that the total amount of overhead would be $180,000

$180,000

and a total of 30,000

30,000 machine hours would be

incurred. Job B011 required 150 machine hours

150 machine hours.

• Required:

Required: Determine the total cost assigned to Job

B011

04/06/25

By Megersa H. 2023 30

31.

Cont…

Cont…

Solutions

Solutions

• Predetermined overheadrate =

= Estimated amount

of MOH/

/Estimated amount of allocation base

•Predetermined overhead rate: $180,000

$180,000 =

= $6.00 perMH

$6.00 perMH

30,000 MH

30,000 MH

•Direct materials used = no. units X Cost per unit

•Direct materials used: 500 pounds X $25.00

500 pounds X $25.00 =

= $12,500

$12,500

•Direct labour cost: 90 DLH X $18.00

90 DLH X $18.00 =

= 1,620

1,620

•Overhead applied to job B011: $6.00 X 150 MH

$6.00 X 150 MH =

= 900

900

•Total job cost: $15,020

$15,020

04/06/25

By Megersa H. 2023 31

32.

Example - 3

Example- 3

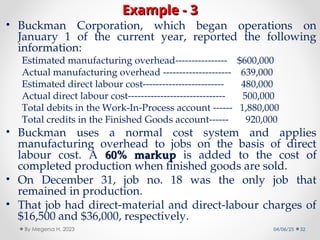

• Buckman Corporation, which began operations on

January 1 of the current year, reported the following

information:

Estimated manufacturing overhead---------------- $600,000

Actual manufacturing overhead --------------------- 639,000

Estimated direct labour cost------------------------- 480,000

Actual direct labour cost------------------------------ 500,000

Total debits in the Work-In-Process account ------ 1,880,000

Total credits in the Finished Goods account------ 920,000

• Buckman uses a normal cost system and applies

manufacturing overhead to jobs on the basis of direct

labour cost. A 60% markup

60% markup is added to the cost of

completed production when finished goods are sold.

• On December 31, job no. 18 was the only job that

remained in production.

• That job had direct-material and direct-labour charges of

$16,500 and $36,000, respectively.

04/06/25 32

By Megersa H. 2023

33.

Cont…

Cont…

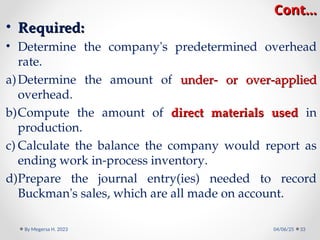

• Required:

Required:

• Determinethe company's predetermined overhead

rate.

a)Determine the amount of under- or over-applied

under- or over-applied

overhead.

b)Compute the amount of direct materials used

direct materials used in

production.

c) Calculate the balance the company would report as

ending work in-process inventory.

d)Prepare the journal entry(ies) needed to record

Buckman's sales, which are all made on account.

04/06/25

By Megersa H. 2023 33

34.

Cont…

Cont…

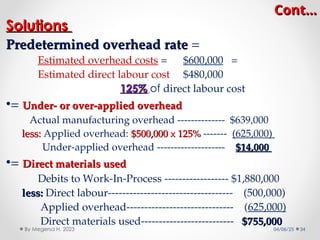

Solutions

Solutions

Predetermined overhead rate

Predeterminedoverhead rate =

Estimated overhead costs = $600,000 =

Estimated direct labour cost $480,000

125%

125% of direct labour cost

•= Under- or over-applied overhead

Under- or over-applied overhead

Actual manufacturing overhead -------------- $639,000

less:

less: Applied overhead: $500,000 x 125%

$500,000 x 125% ------- (625,000)

Under-applied overhead -------------------- $14,000

$14,000

•= Direct materials used

Direct materials used

Debits to Work-In-Process ------------------ $1,880,000

less:

less: Direct labour----------------------------------- (500,000)

Applied overhead------------------------------ (625,000)

Direct materials used-------------------------- $755,000

$755,000

04/06/25 34

By Megersa H. 2023

35.

Cont…

Cont…

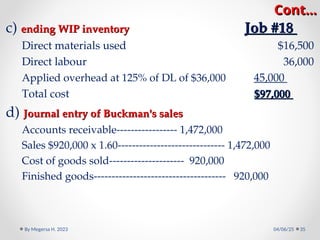

c) ending WIPinventory

ending WIP inventory Job #18

Job #18

Direct materials used $16,500

Direct labour 36,000

Applied overhead at 125% of DL of $36,000 45,000

Total cost $97,000

$97,000

d) Journal entry of Buckman's sales

Journal entry of Buckman's sales

Accounts receivable----------------- 1,472,000

Sales $920,000 x 1.60------------------------------ 1,472,000

Cost of goods sold--------------------- 920,000

Finished goods------------------------------------- 920,000

04/06/25

By Megersa H. 2023 35

36.

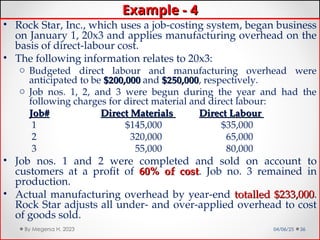

Example - 4

Example- 4

• Rock Star, Inc., which uses a job-costing system, began business

on January 1, 20x3 and applies manufacturing overhead on the

basis of direct-labour cost.

• The following information relates to 20x3:

o Budgeted direct labour and manufacturing overhead were

anticipated to be $200,000

$200,000 and $250,000

$250,000, respectively.

o Job nos. 1, 2, and 3 were begun during the year and had the

following charges for direct material and direct labour:

Job#

Job# Direct Materials

Direct Materials Direct Labour

Direct Labour

1 $145,000 $35,000

2 320,000 65,000

3 55,000 80,000

• Job nos. 1 and 2 were completed and sold on account to

customers at a profit of 60% of cost

60% of cost. Job no. 3 remained in

production.

• Actual manufacturing overhead by year-end totalled $233,000

totalled $233,000.

Rock Star adjusts all under- and over-applied overhead to cost

of goods sold.

04/06/25 36

By Megersa H. 2023

37.

Cont…

Cont…

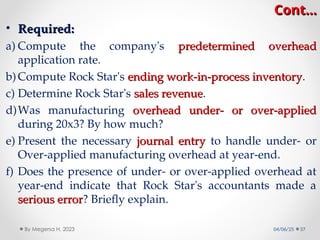

• Required:

Required:

a) Computethe company's predetermined overhead

predetermined overhead

application rate.

b) Compute Rock Star's ending work-in-process inventory

ending work-in-process inventory.

c) Determine Rock Star's sales revenue

sales revenue.

d)Was manufacturing overhead under- or over-applied

overhead under- or over-applied

during 20x3? By how much?

e) Present the necessary journal entry

journal entry to handle under- or

Over-applied manufacturing overhead at year-end.

f) Does the presence of under- or over-applied overhead at

year-end indicate that Rock Star's accountants made a

serious error

serious error? Briefly explain.

04/06/25 37

By Megersa H. 2023

38.

Cont…

Cont…

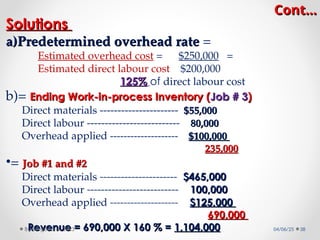

Solutions

Solutions

a)

a)Predetermined overhead rate

Predeterminedoverhead rate =

Estimated overhead cost = $250,000 =

Estimated direct labour cost $200,000

125%

125% of direct labour cost

b)= Ending Work-in-process Inventory (

Ending Work-in-process Inventory (Job # 3

Job # 3)

)

Direct materials ---------------------- $55,000

$55,000

Direct labour -------------------------- 80,000

80,000

Overhead applied -------------------- $100,000

$100,000

235,000

235,000

•= Job #1 and #2

Job #1 and #2

Direct materials ---------------------- $465,000

$465,000

Direct labour -------------------------- 100,000

100,000

Overhead applied -------------------- $125,000

$125,000

690,000

690,000

Revenue = 690,000 X 160 % =

Revenue = 690,000 X 160 % = 1,104,000

1,104,000 04/06/25 38

By Megersa H. 2023

39.

Cont…

Cont…

d)

d) = overheadunder- or over-applied

overhead under- or over-applied

Actual manufacturing overhead ------------- $233,000

$233,000

less: Applied manufacturing overhead ---- (225,000)

225,000)

Under applied Overhead------------------------ $8,000

$8,000

e)

e) = Journal Entry

Journal Entry

Cost of goods sold --------- 8,000

8,000

Manufacturing overhead --------------------- 8,000

8,000

f)

f) = No.

No. Companies use a predetermined application rate for

several reasons including the fact that manufacturing overhead is

not easily traced to jobs and products. The predetermined rate is

based on estimates of both overhead and an appropriate cost

driver, and these estimated rarely equal actual overhead incurred

or the actual cost driver activity. Under- or over-applied

overhead typically arises at year-end.

04/06/25 39

By Megersa H. 2023