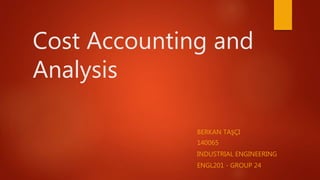

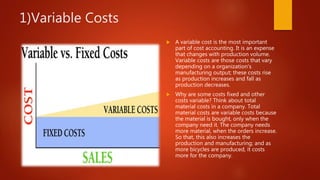

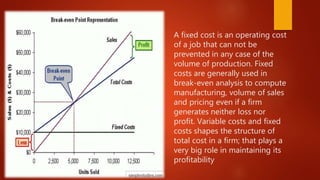

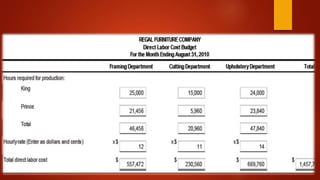

Cost accounting is a process that collects, records, analyzes, and evaluates costs to advise management on the most cost-efficient course of action. It originated during the Industrial Revolution to help managers understand complex business costs. Costs are classified as either variable, meaning they change with production volume, or fixed, remaining constant regardless of production levels. Key cost objects include direct materials, direct labor, and manufacturing overhead. Analyzing these cost objects allows for more accurate cost calculation and identification of inefficient activities to improve cost efficiency.

![7_C's_OF_COMMUNIOCATION[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7csofcommuniocation1-230801063320-9af405b3-thumbnail.jpg?width=640&height=640&fit=bounds)