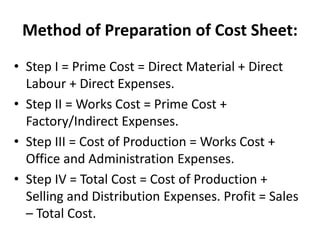

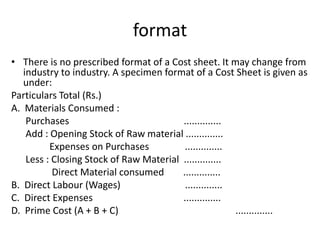

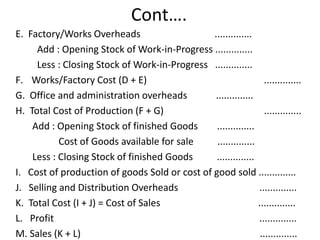

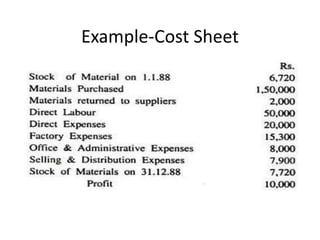

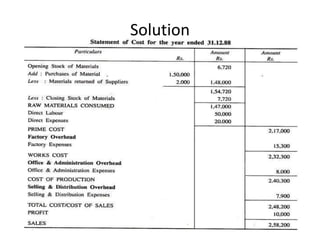

Unit or output costing is used when standard products are produced through a common process and units are similar. A cost sheet is prepared to show the detailed cost of total output for a period. It assembles estimated costs for a cost center and helps management fix selling prices, submit tenders, and formulate production policies by providing cost per unit. A cost sheet calculates prime cost as direct materials + direct labor + direct expenses, then adds factory overheads for works cost, office expenses for cost of production, and selling/distribution costs for total cost.

![Understanding Cost sheet - Kiruba Sorna Mary[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/understandingcostsheet-kirubasornamary1-250701093812-e86fb0f7-thumbnail.jpg?width=640&height=640&fit=bounds)

![cost sheet element [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/costsheetelementautosaved-231002114359-14338e3e-thumbnail.jpg?width=640&height=640&fit=bounds)