STI Inventory Costing Methods

•

0 likes•305 views

Accounting Principles - Midterm 3rd year 1st sem

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to STI Inventory Costing Methods

Similar to STI Inventory Costing Methods (20)

More from Anne Lee

More from Anne Lee (20)

Recently uploaded

Recently uploaded (20)

STI Inventory Costing Methods

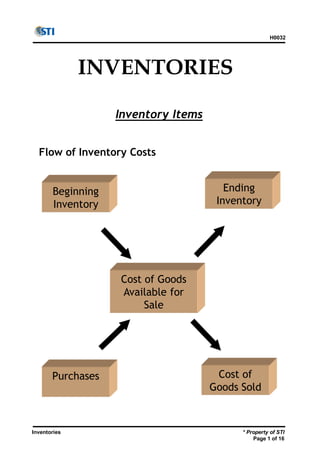

- 1. Inventories H0032 * Property of STI Page 1 of 16 INVENTORIES Inventory Items Flow of Inventory Costs Cost of Goods Available for Sale Ending Inventory Cost of Goods Sold Beginning Inventory Purchases

- 2. Inventories H0032 * Property of STI Page 2 of 16 Inventory Items (Amounts in millions) Beginning Inventory P 276 + Net purchases 1,348 = Cost of goods available for sale 1,624 - Ending inventory 317 = Cost of goods sold P 1,307 Types of companies o Merchandising company o Manufacturing company o Service organization

- 3. Inventories H0032 * Property of STI Page 3 of 16 Cost of Inventory 1. Determining the Quantity of Inventory o FOB (Free on Board) FOB Shipping Point FOB Destination o Consigned Goods 2. Determining the Unit Cost of Inventory Figuring the Cost of Inventory

- 4. Inventories H0032 * Property of STI Page 4 of 16 Inventory Costing Methods 1. Specific Unit Cost 2. Average Costs Method 3. First-in, First-out Cost 4. Last-in, First-out Cost Inventory & Cost of Goods Sold under Average, FIFO & LIFO Inventory Costing Methods

- 5. Inventories H0032 * Property of STI Page 5 of 16 Inventory Costing Methods

- 6. Inventories H0032 * Property of STI Page 6 of 16 Inventory Costing Methods

- 7. Inventories H0032 * Property of STI Page 7 of 16 EffectofFIFO,LIFOandAverageCostonIncome&Income Tax EffectonIncome

- 8. Inventories H0032 * Property of STI Page 8 of 16 EffectofFIFO,LIFOandAverageCostonIncome&Income Tax EffectonIncomeTax

- 9. Inventories H0032 * Property of STI Page 9 of 16 SampleProblem

- 10. Inventories H0032 * Property of STI Page 10 of 16 Accounting Conservatism Lower-of-Cost or Market (LCM) Effects

- 11. Inventories H0032 * Property of STI Page 11 of 16 Lower-of-CostorMarket(LCM)Effects AccountingConservatism

- 12. Inventories H0032 * Property of STI Page 12 of 16 EffectofInventoryErrors

- 13. Inventories H0032 * Property of STI Page 13 of 16 Methods of Estimating Inventory 1. Gross Margin (Gross Profit) Method Beginning inventory + Net purchases = Cost of goods available for sale - Cost of goods sold = Ending inventory Gross Margin Method of Estimating Inventory (amounts assumed) Beginning inventory ……………………………. P 140,000 Net purchases ……………………………………… 660,000 Cost of goods available for sale …………. 800,000 Cost of goods sold: Net sales revenue…………………………….. P 1,000,000 Less estimated gross margin of 40%... 400,000 Estimated cost of goods sold …………… 600,000 Estimated cost of ending inventory ……. P 200,000

- 14. Inventories H0032 * Property of STI Page 14 of 16 Methods of Estimating Inventory 2.Retail Method Retail Method of Estimating Inventory (amounts assumed)

- 15. Inventories H0032 * Property of STI Page 15 of 16 Periodic and Perpetual Inventory System Periodic Inventory System Perpetual Inventory System

- 16. Inventories H0032 * Property of STI Page 16 of 16 Internal Control over Inventory 1. Physically counting inventory at least once a year. 2. Maintaining efficient purchasing, receiving & shipping procedures. 3. Storing inventory to prevent against theft, damage & decay. 4. Limiting access to personnel. 5. Keeping perpetual inventory records for high- unit-cost merchandise. 6. Purchasing inventory in economical quantities. 7. Keeping enough inventories on hand. 8. Avoid tying up money in items that are not needed.