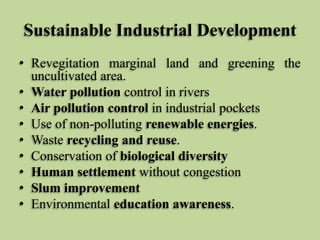

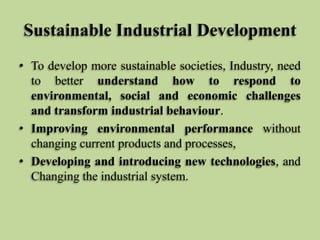

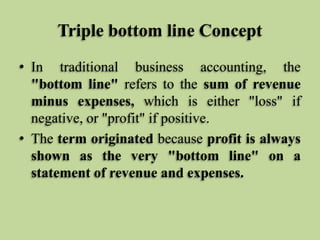

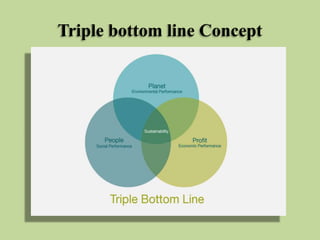

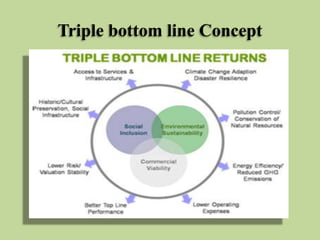

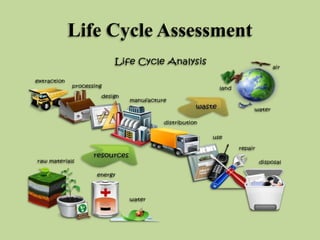

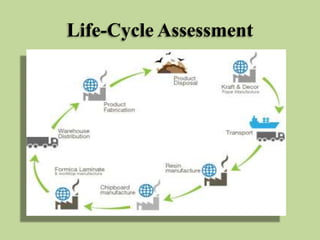

This document discusses concepts related to corporate environmental management strategies. It covers topics like strategic environmental management, sustainable industrial development, the triple bottom line concept, cleaner technologies, life cycle analysis, and green marketing. For sustainable industrial development, it emphasizes the importance of factors like population stabilization, integrated land use planning, and use of non-polluting renewable energies. The triple bottom line concept involves considering social, environmental and economic factors. Life cycle analysis assesses environmental impacts across a product's entire lifecycle. Green marketing involves marketing environmentally-friendly products and emphasizing environmental aspects in promotion.