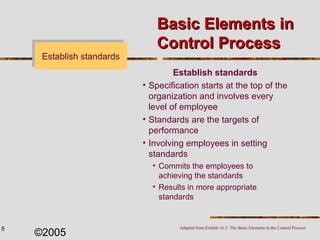

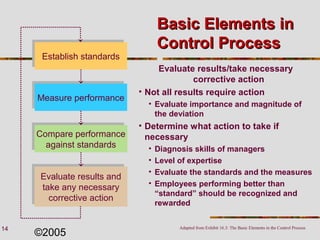

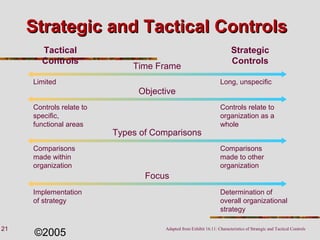

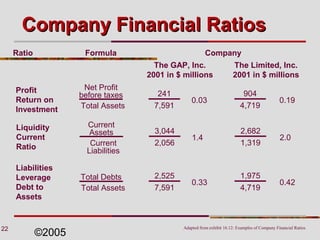

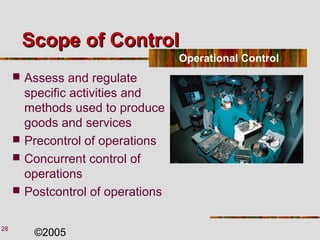

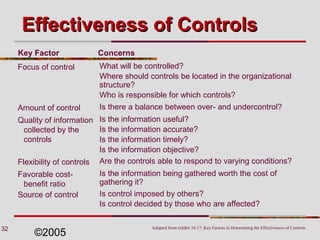

This document discusses control in organizations. It covers the basic elements of the control process, which are establishing standards, measuring performance, comparing performance to standards, and evaluating results to take corrective action if needed. It also discusses different types of control, including strategic control to assess long-term goals, tactical control to regulate day-to-day functions, and operational control to regulate specific activities. Key factors that determine control effectiveness are the focus, amount, quality, flexibility, cost-benefit ratio, and source of control. Different control approaches are needed depending on the stability of the environment.