![A Changing World Al Pipkin, controller for Coors Brewing Company, observes that IT is: . . . bringing about a total transformation of the controller’s [accounting] staff, and a re‑definition of the overall financial system. Technology is changing the culture of the controller’s organization just as it is impacting the entire business. In the 21st century, there will be fewer accountants on the controller’s staff, but they will perform in totally new and exciting ways. Controller The individual or function responsible for using, designing, and evaluating an organizations financial information system. The controller is typically an accounting executive responsible for developing and maintaining an organizations financial records.](https://image.slidesharecdn.com/computerised-accounting-system-1221833559903867-9/85/Computerised-Accounting-System-7-320.jpg)

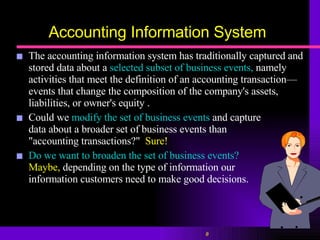

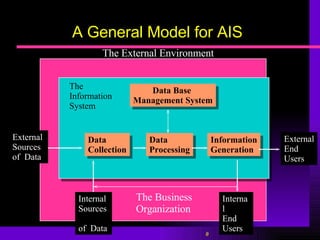

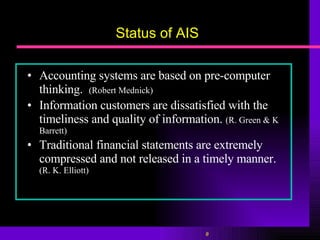

The document discusses the need for changes to accounting information systems to better meet the needs of modern businesses and information users. It notes that the current systems were designed based on pre-computer thinking and that information customers are dissatisfied with the quality and timeliness of information provided. The accounting profession must reinvent how information is gathered, stored, and provided or risk being replaced. The document advocates broadening the types of business events captured beyond just accounting transactions to provide more relevant information to decision makers.

![accounting_information_system[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountinginformationsystem1-231215144622-b88f4649-thumbnail.jpg?width=640&height=640&fit=bounds)