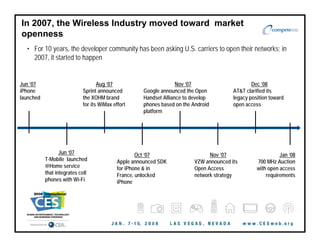

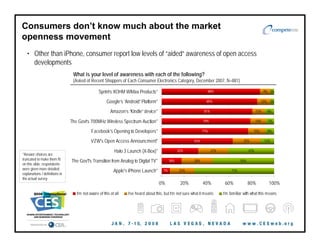

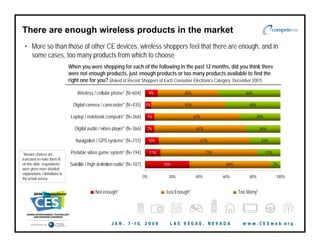

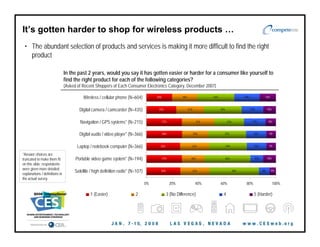

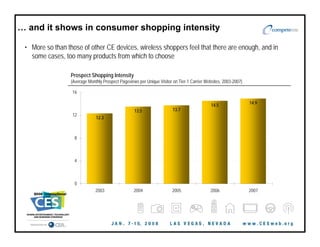

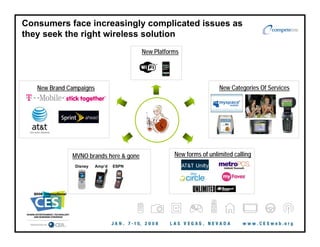

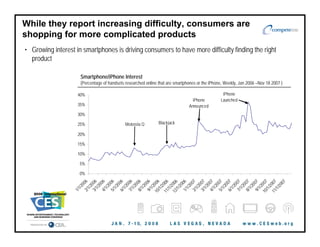

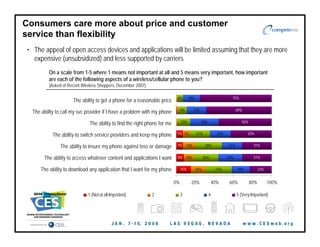

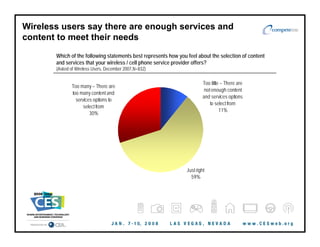

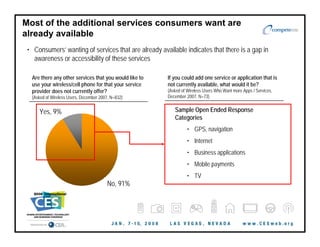

The document discusses market openness in the wireless industry and highlights consumer demand for more connectivity and options in wireless technology, particularly in 2007. It presents findings from a study of consumer behaviors and attitudes, showing that while shoppers appreciate available services, they struggle with finding the right products and prioritize price and customer service over flexibility. Key developments include the opening of networks by U.S. carriers, yet awareness remains low among consumers about these movements and their implications.