Downloaded 39 times

HDFC is a leading financial services group in India that was founded in 1977 with a mission to promote home ownership. It has expanded to include companies providing banking, insurance, asset management, securities, and other financial services. The document provides an overview of HDFC's various subsidiaries and their roles in promoting its mission. It describes the history and objectives of HDFC and each of its major subsidiary companies.

Introduction to the project on comparison of HDFC Equity Schemes with competitors, focusing on the importance of mutual funds in investment.

Details about HDFC's history, objectives, key companies like HDFC Bank and HDFC Mutual Fund, and their impact on the housing finance sector.

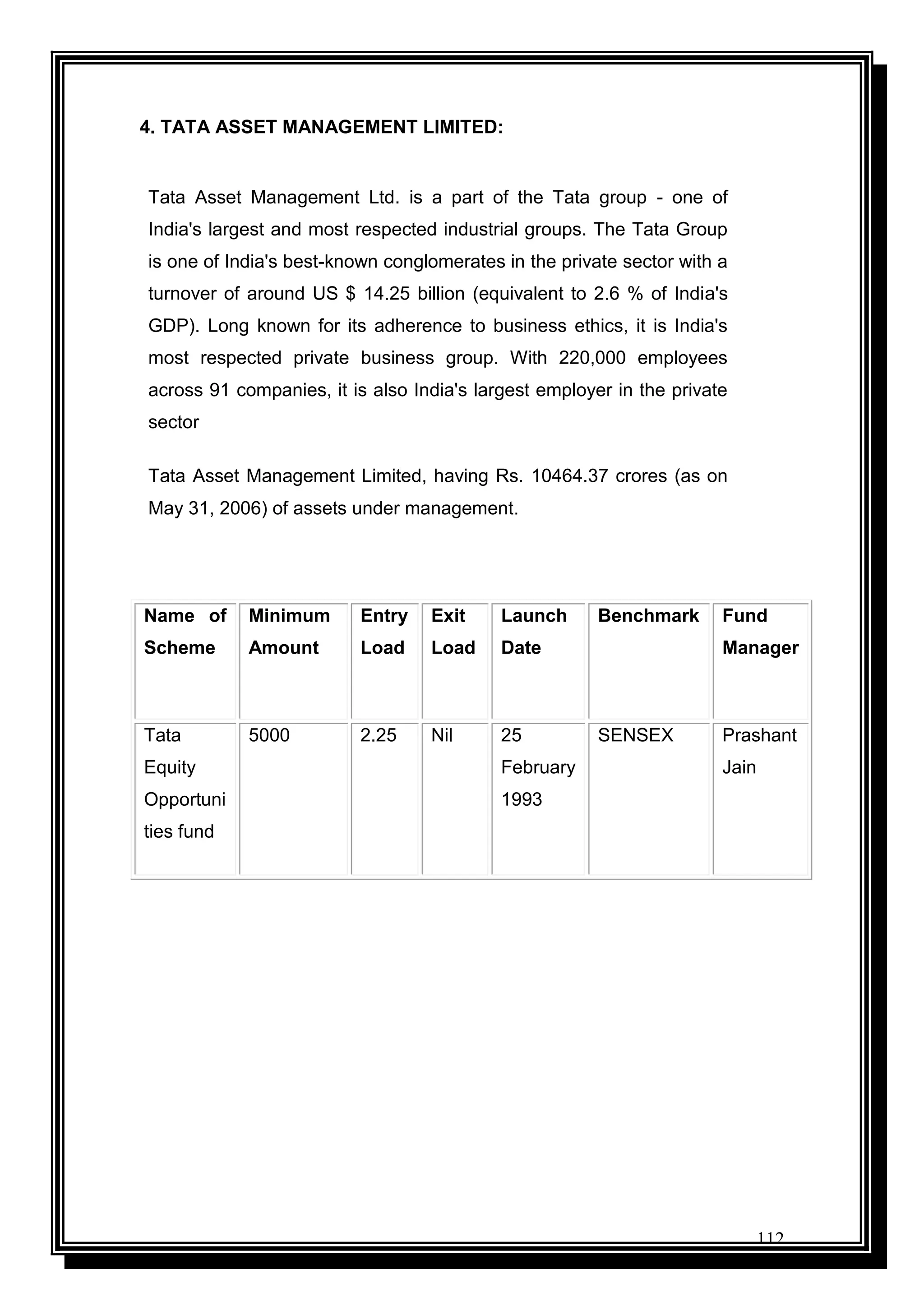

Information on HDFC's various financial services and subsidiaries, highlighting their roles in the market.

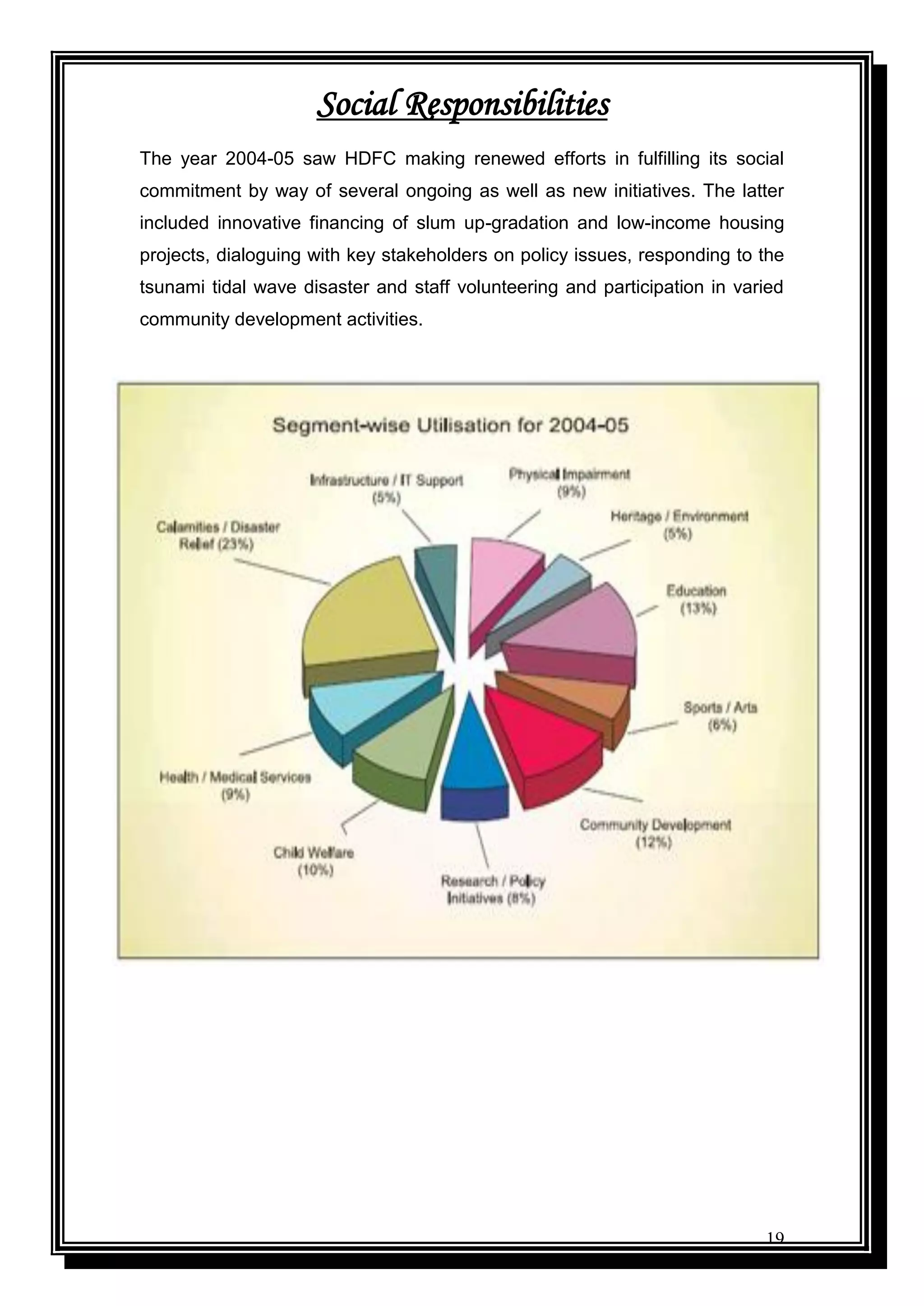

HDFC's efforts towards social initiatives, including financing low-income housing and community development projects.

Examining HDFC's strengths, weaknesses, opportunities, and threats, especially pertaining to mutual fund operations.

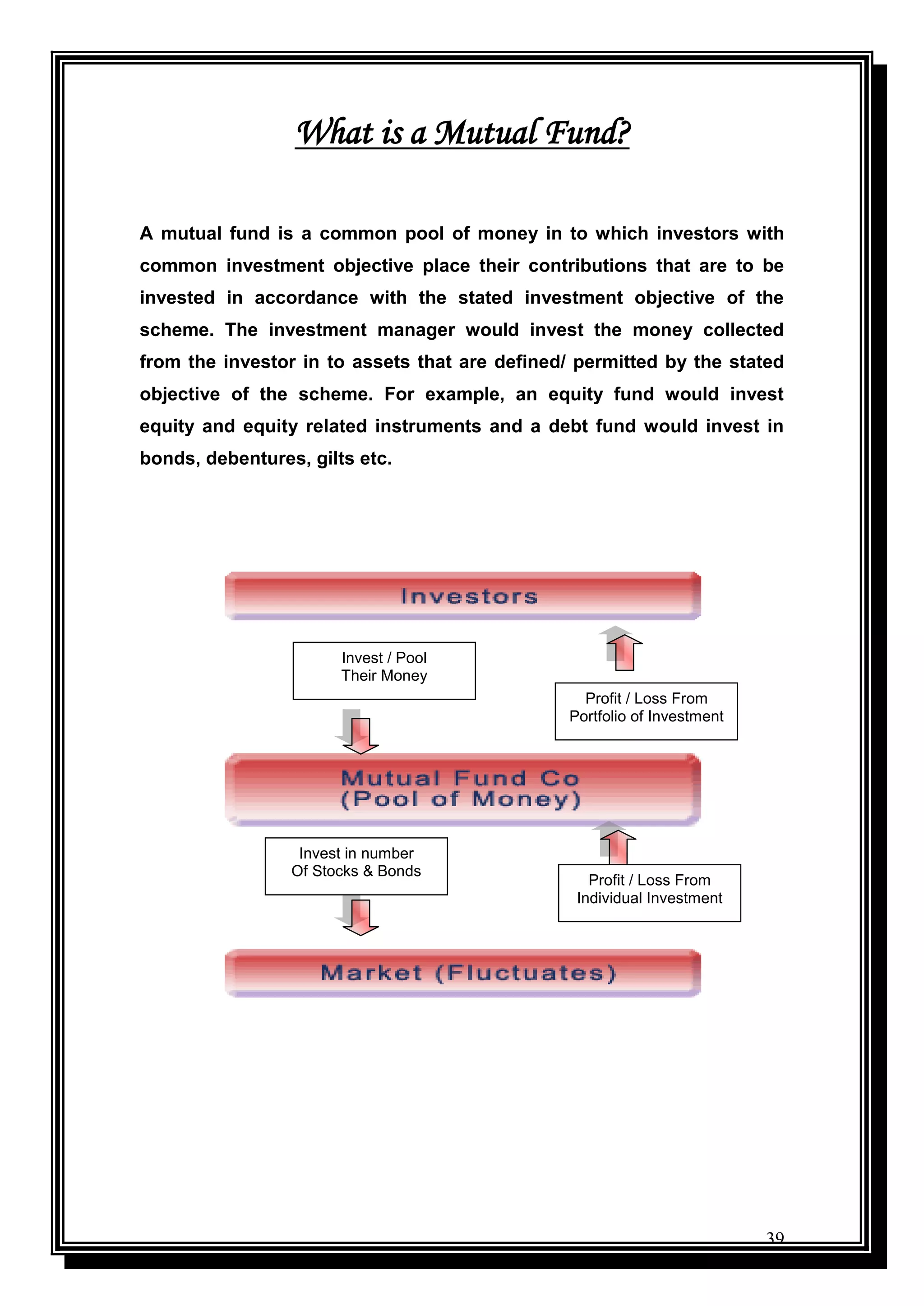

Discussion on the mutual fund sector's influence in financial markets and the emergence of mutual funds as key investment vehicles.

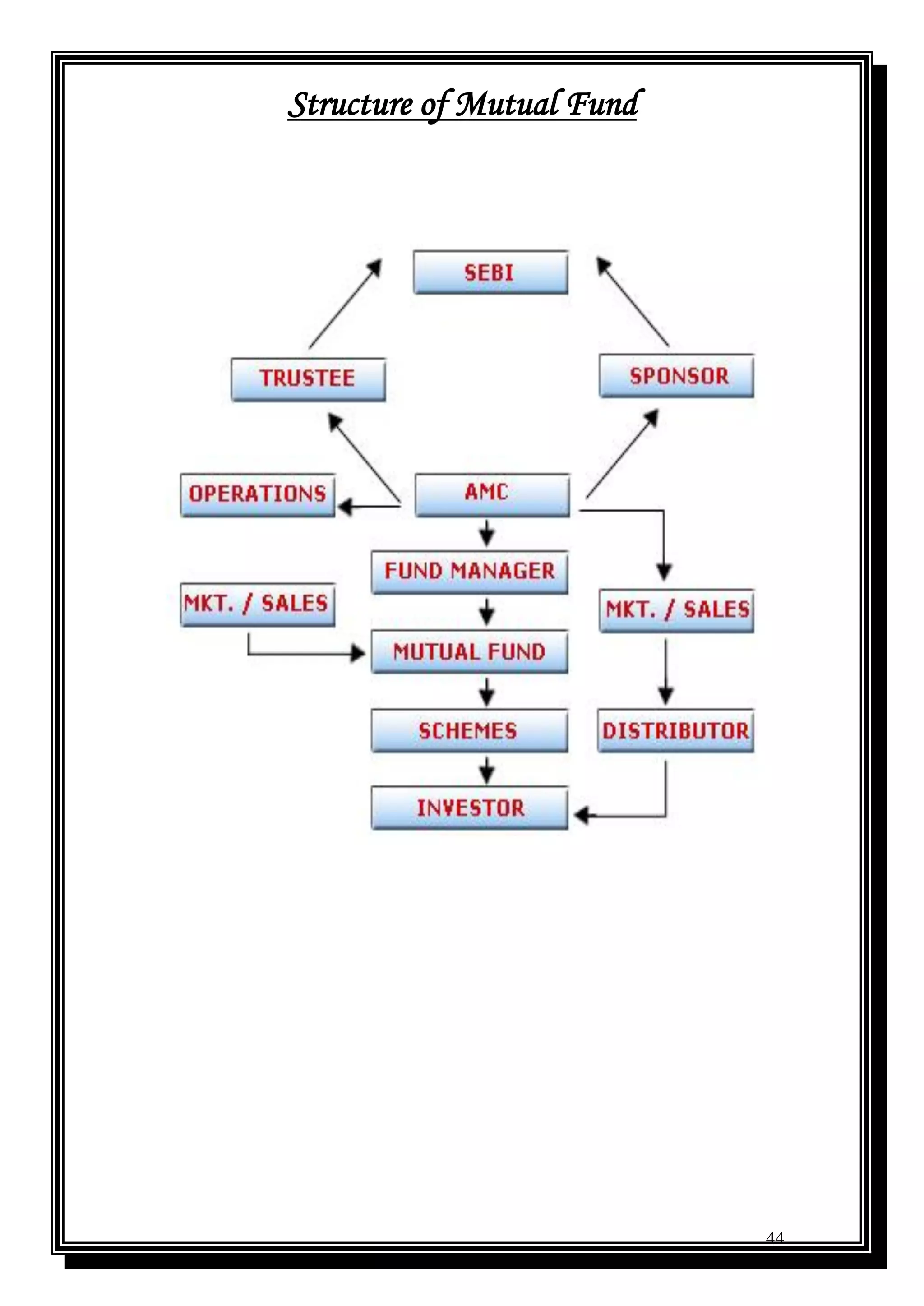

The structure and characteristics of mutual funds, alongside competitor analysis within the Indian mutual fund landscape.

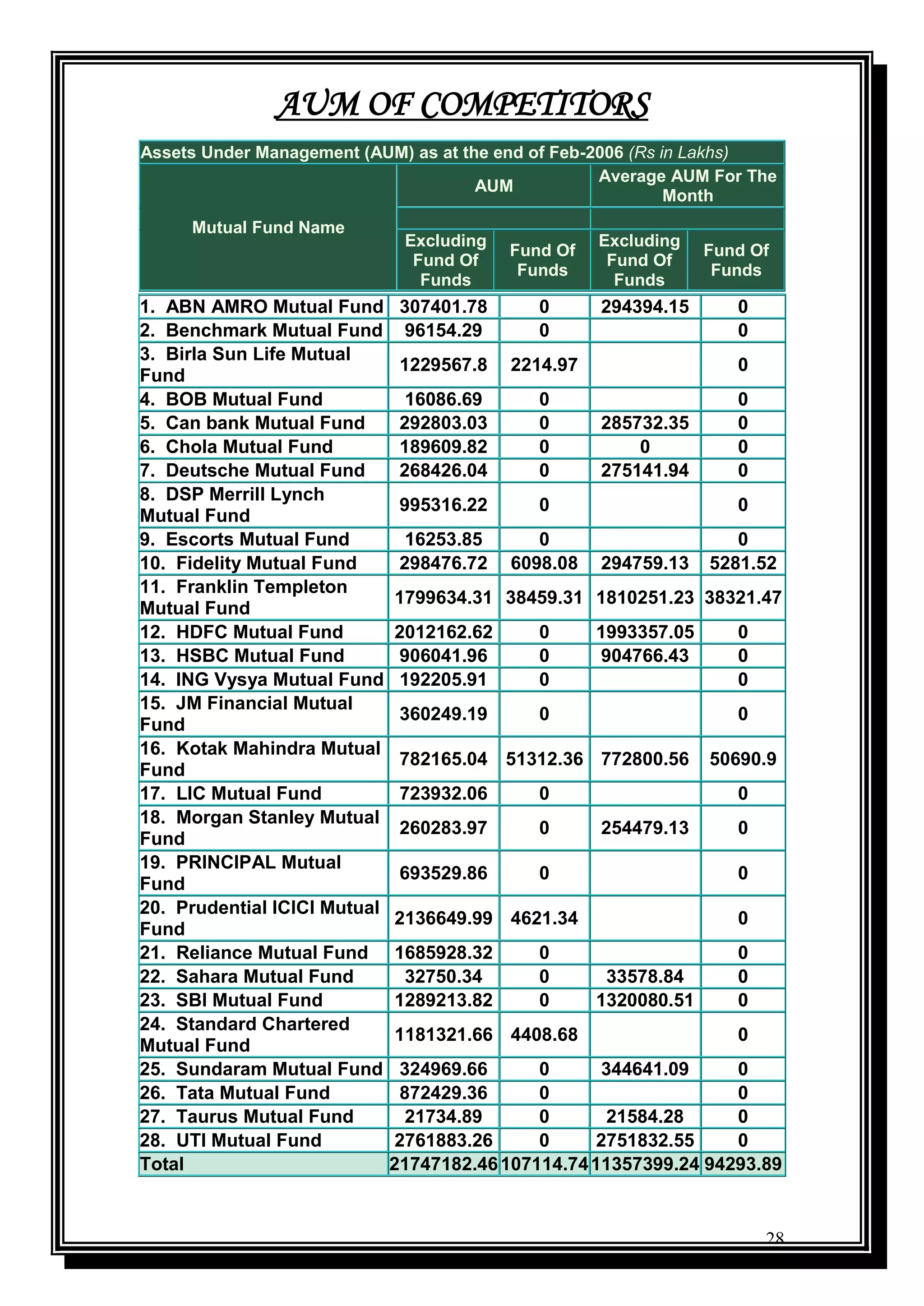

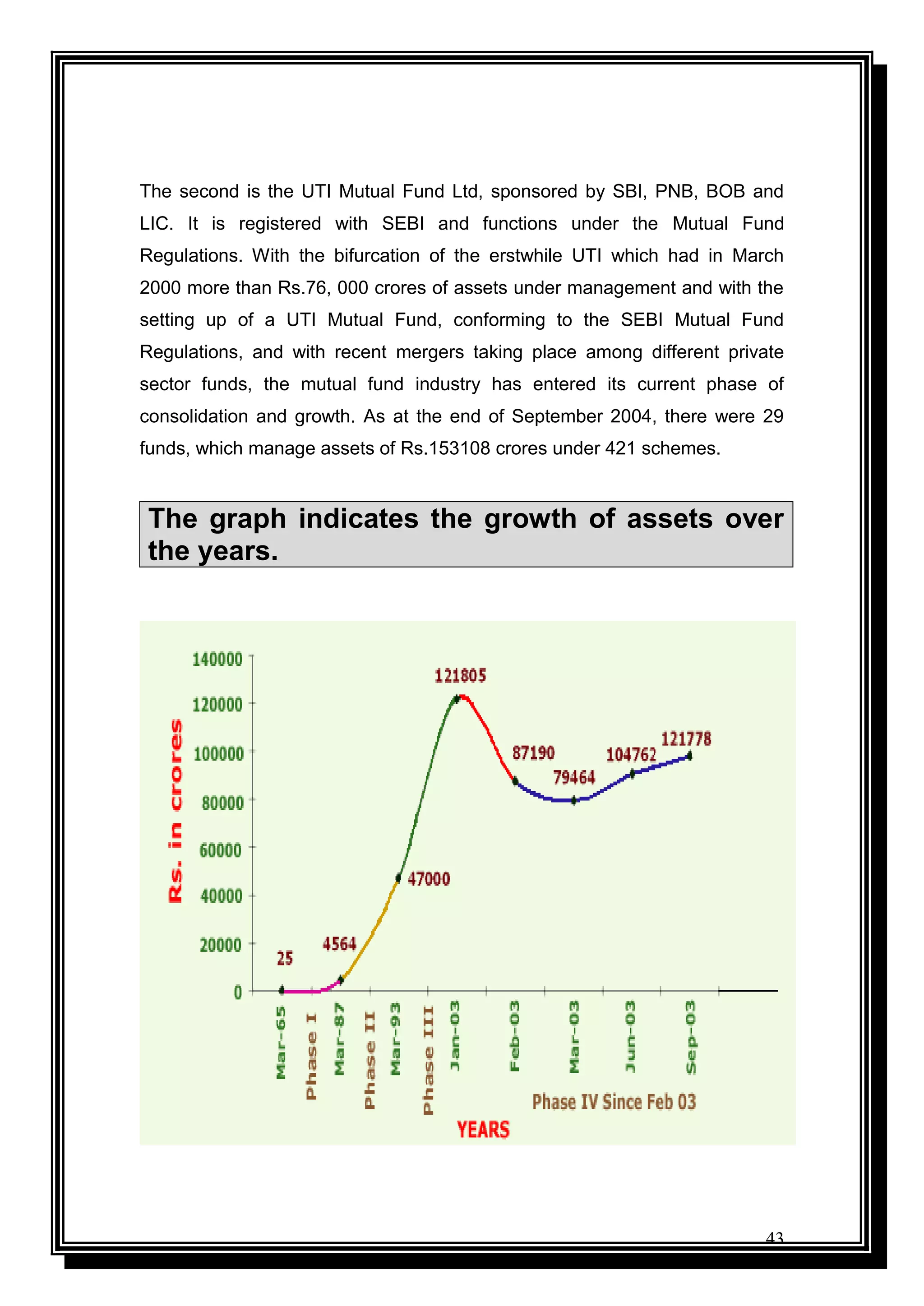

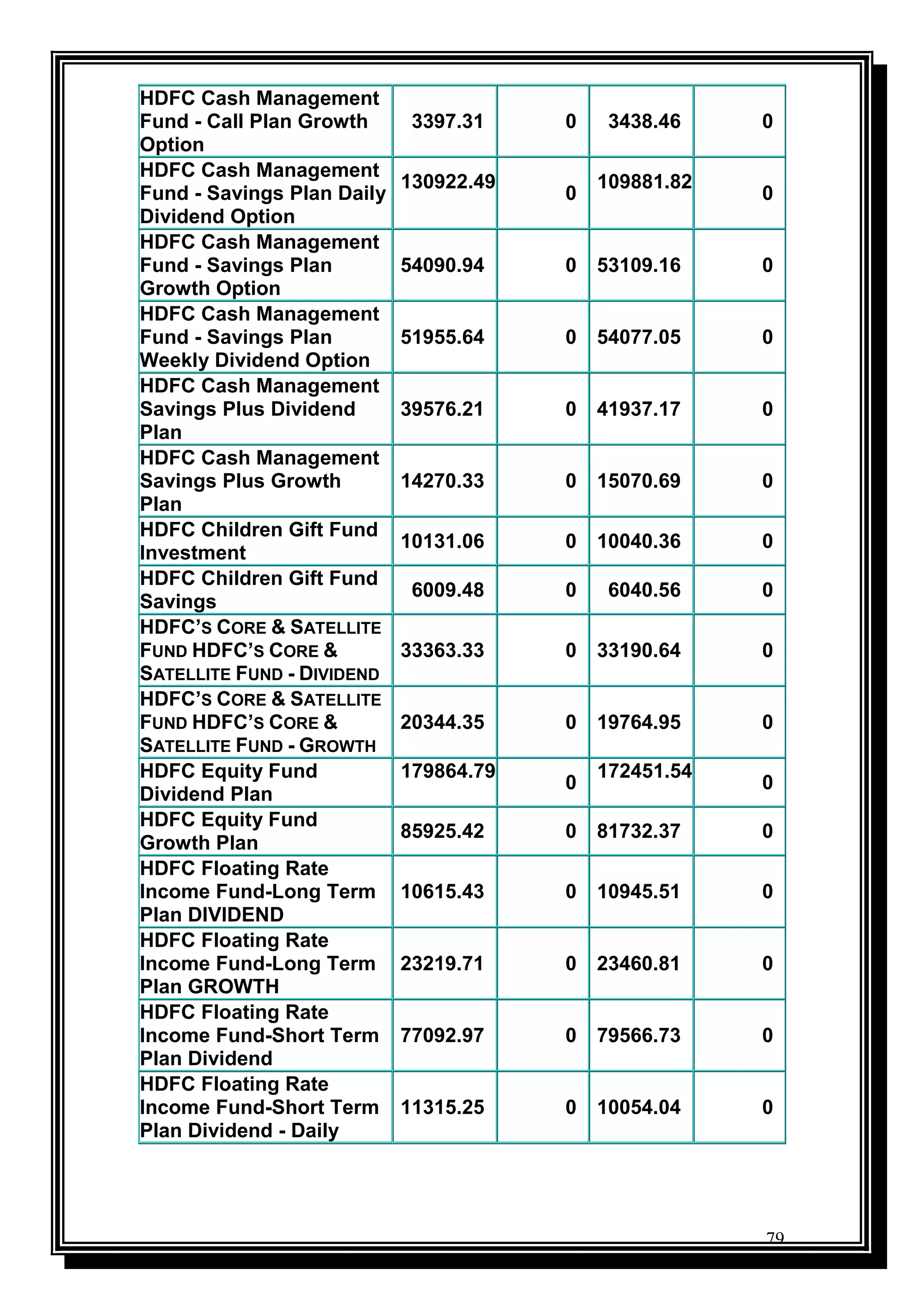

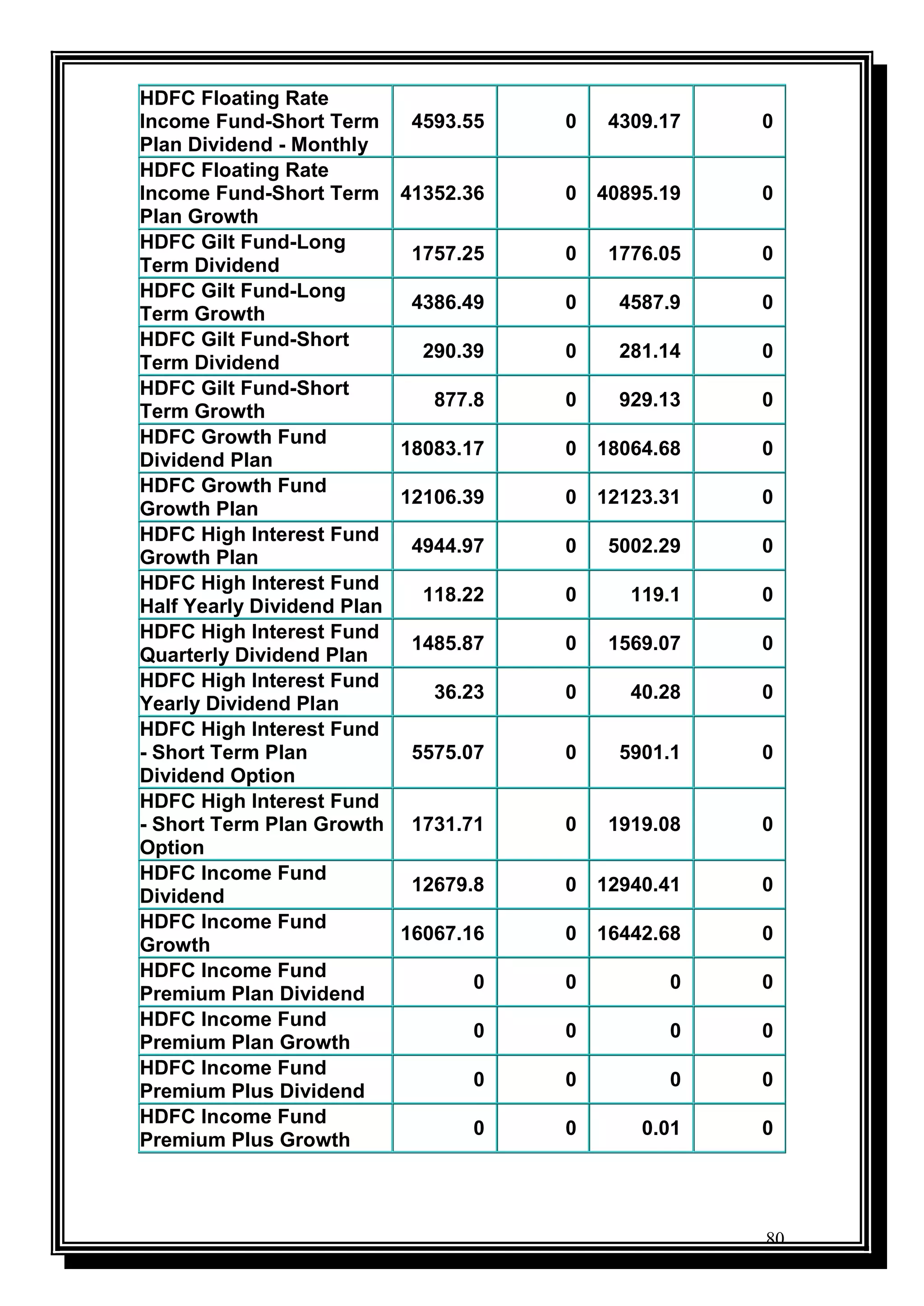

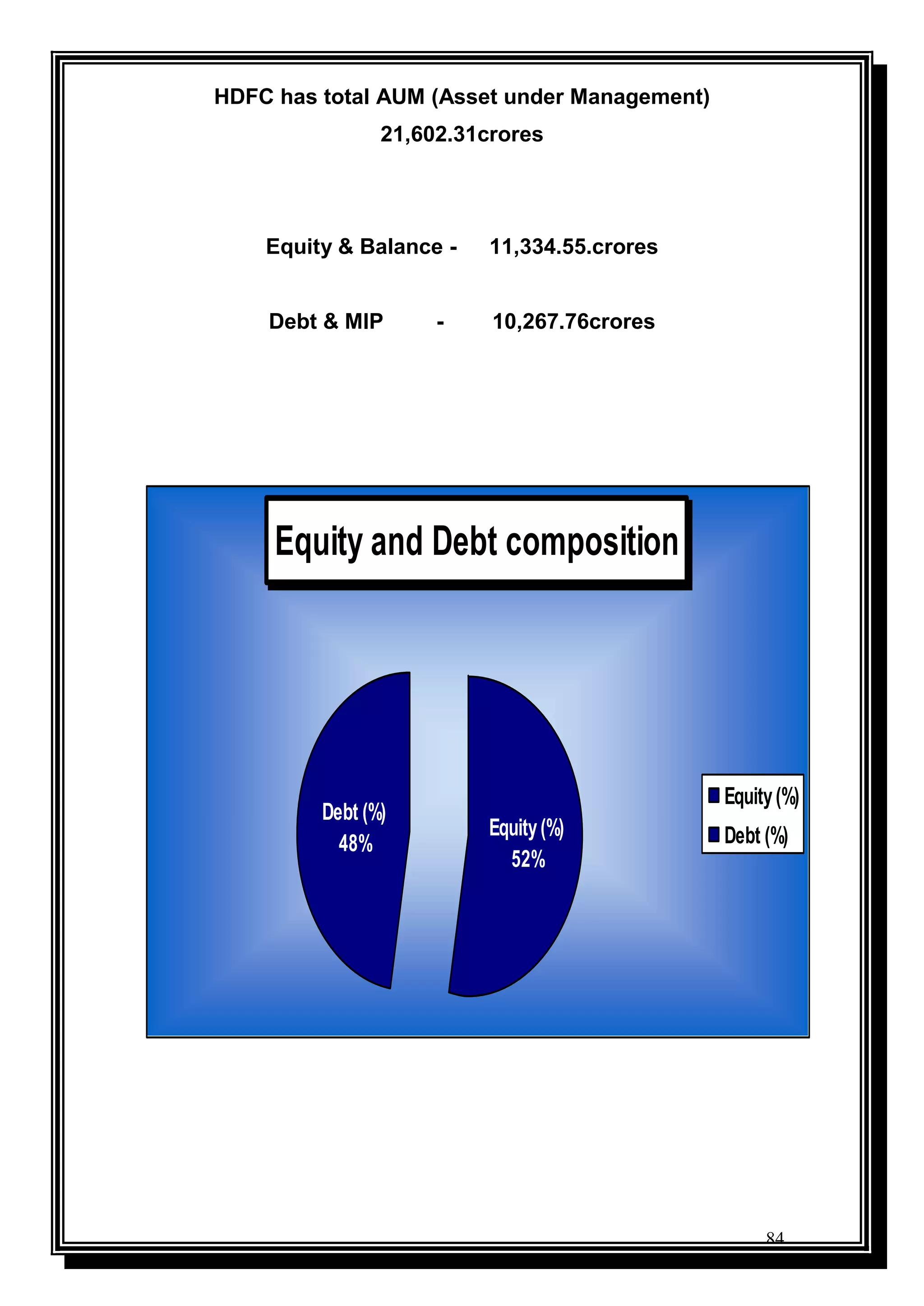

Insights into Assets Under Management (AUM) data and regulatory environments governing mutual funds in India.

Marketing strategies and customer profiling for HDFC Asset Management Company to enhance mutual fund visibility.

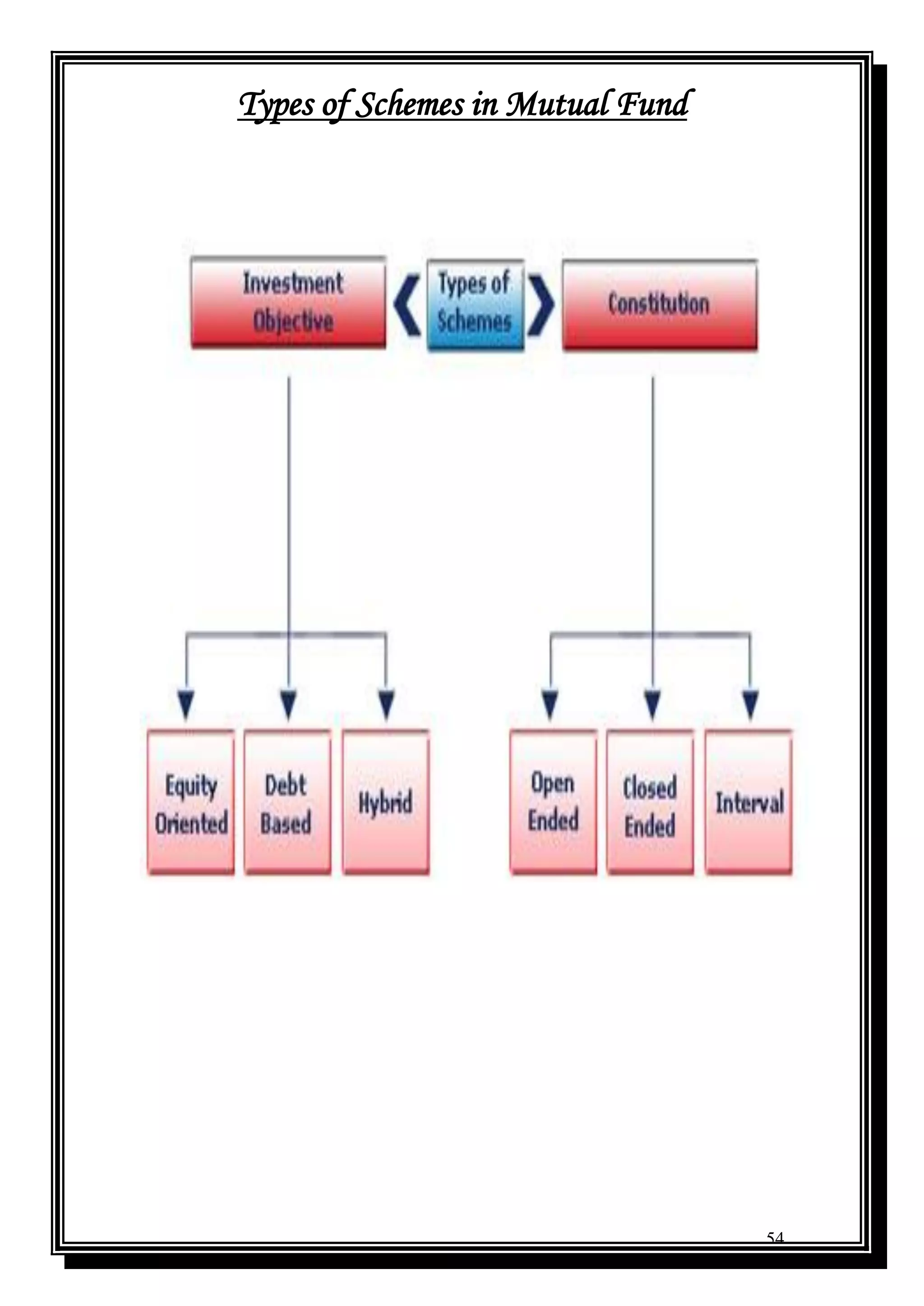

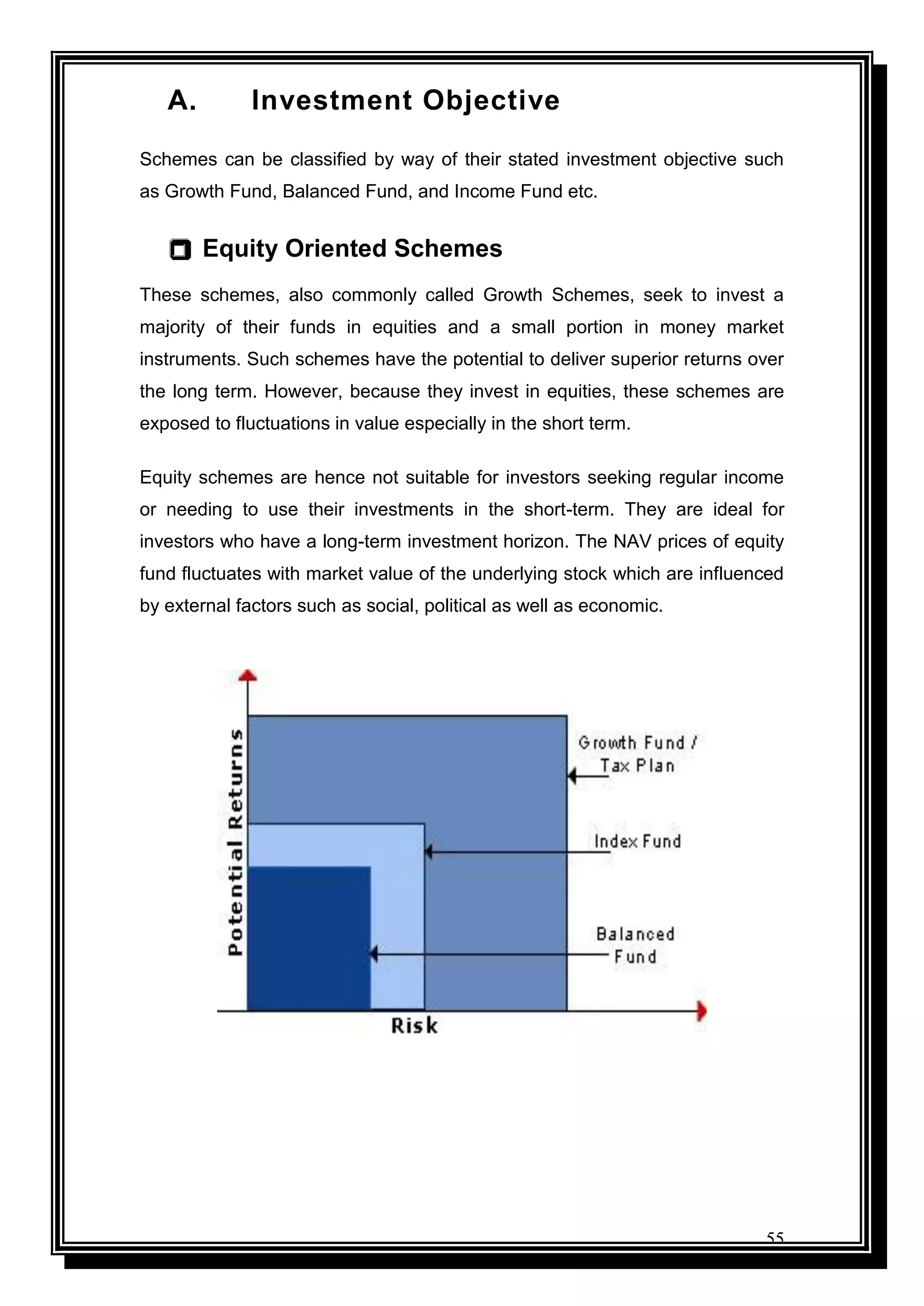

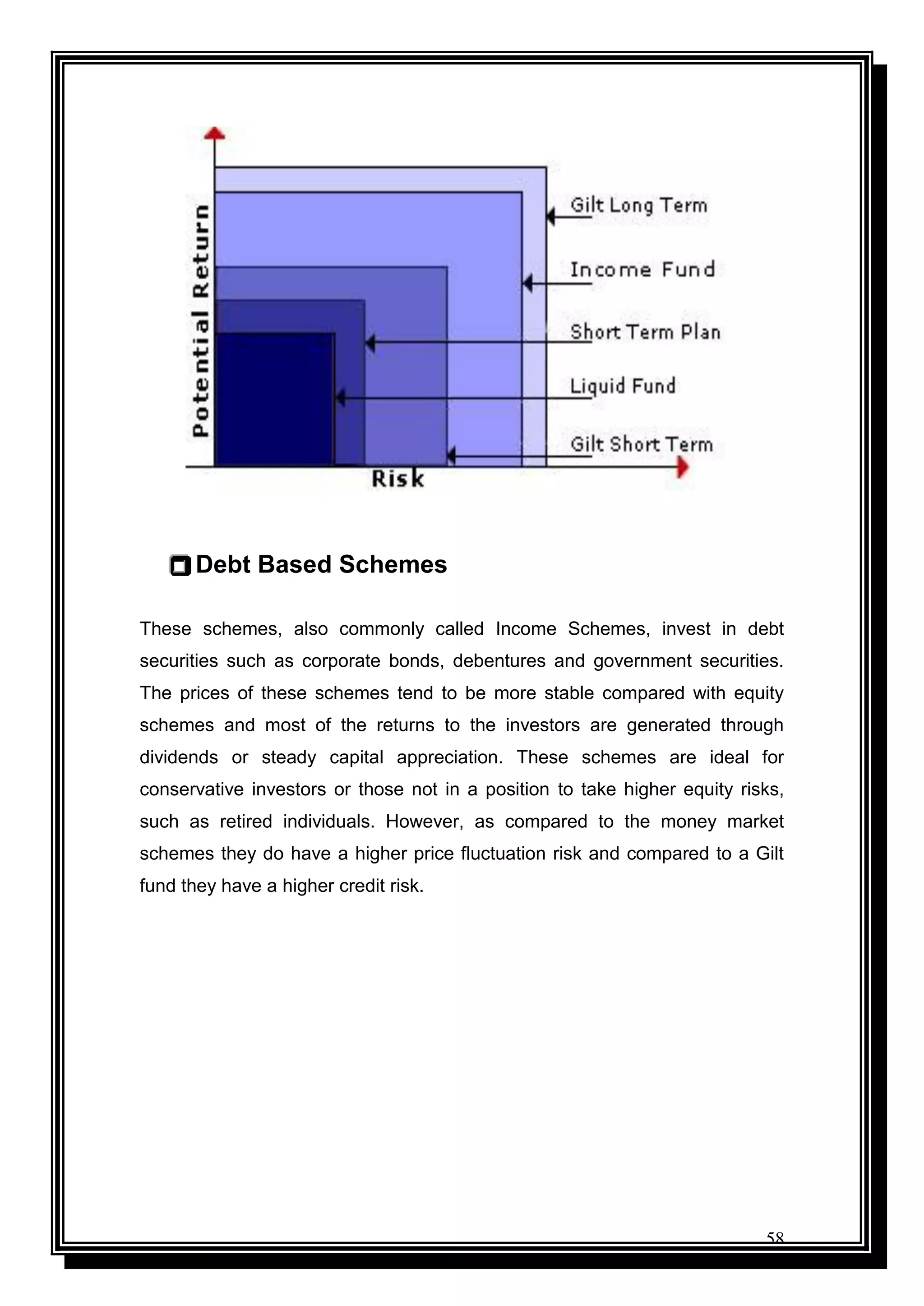

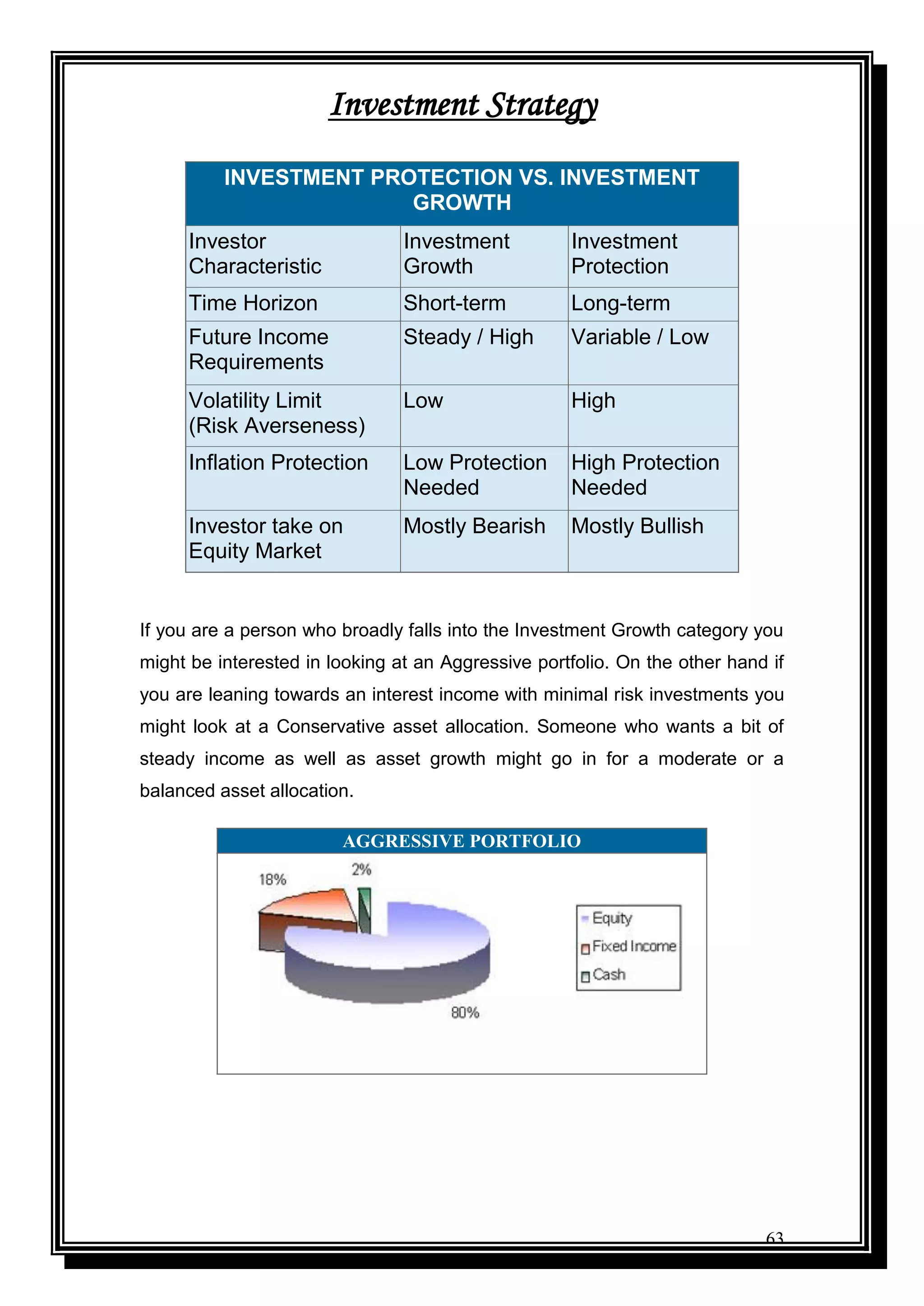

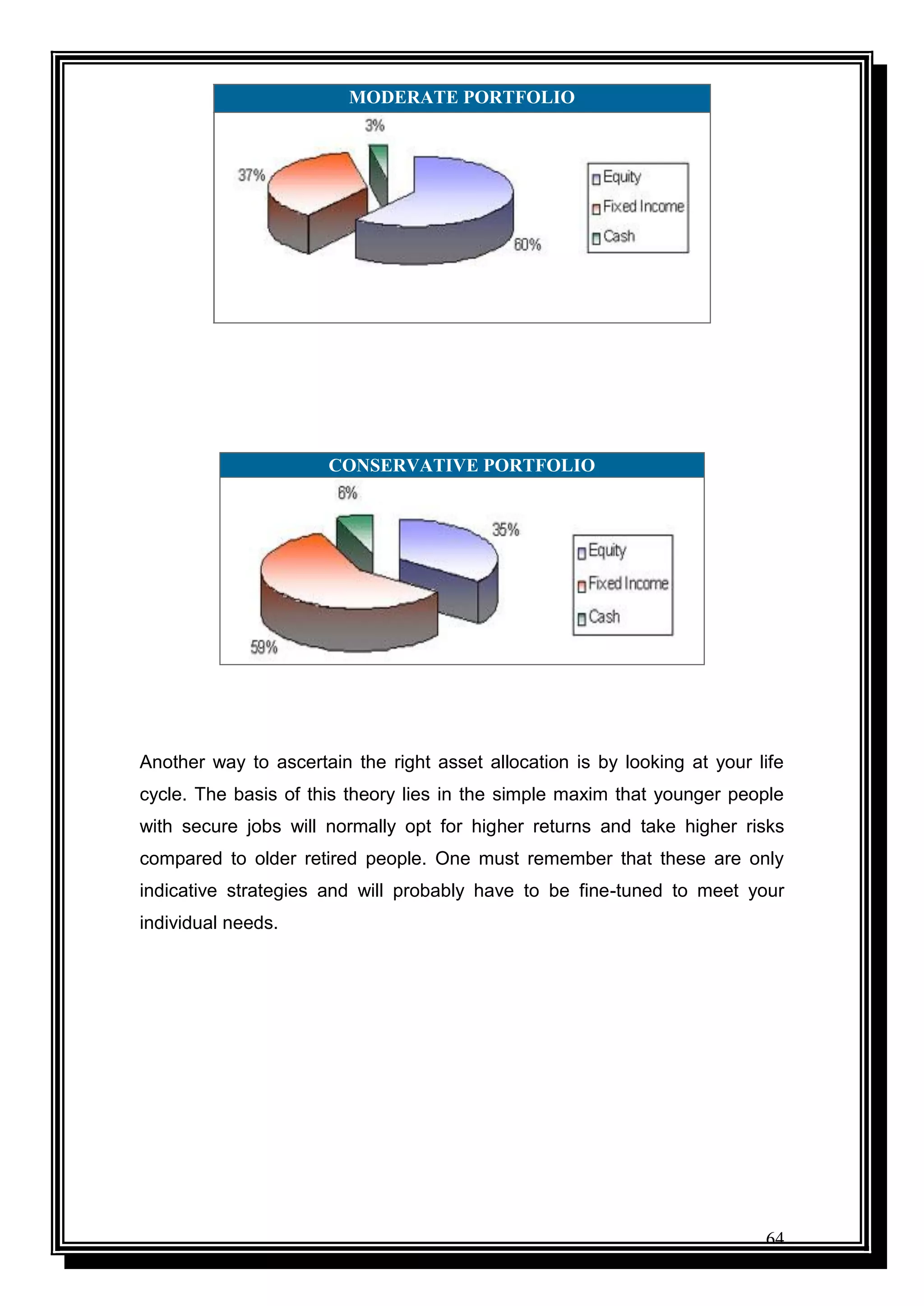

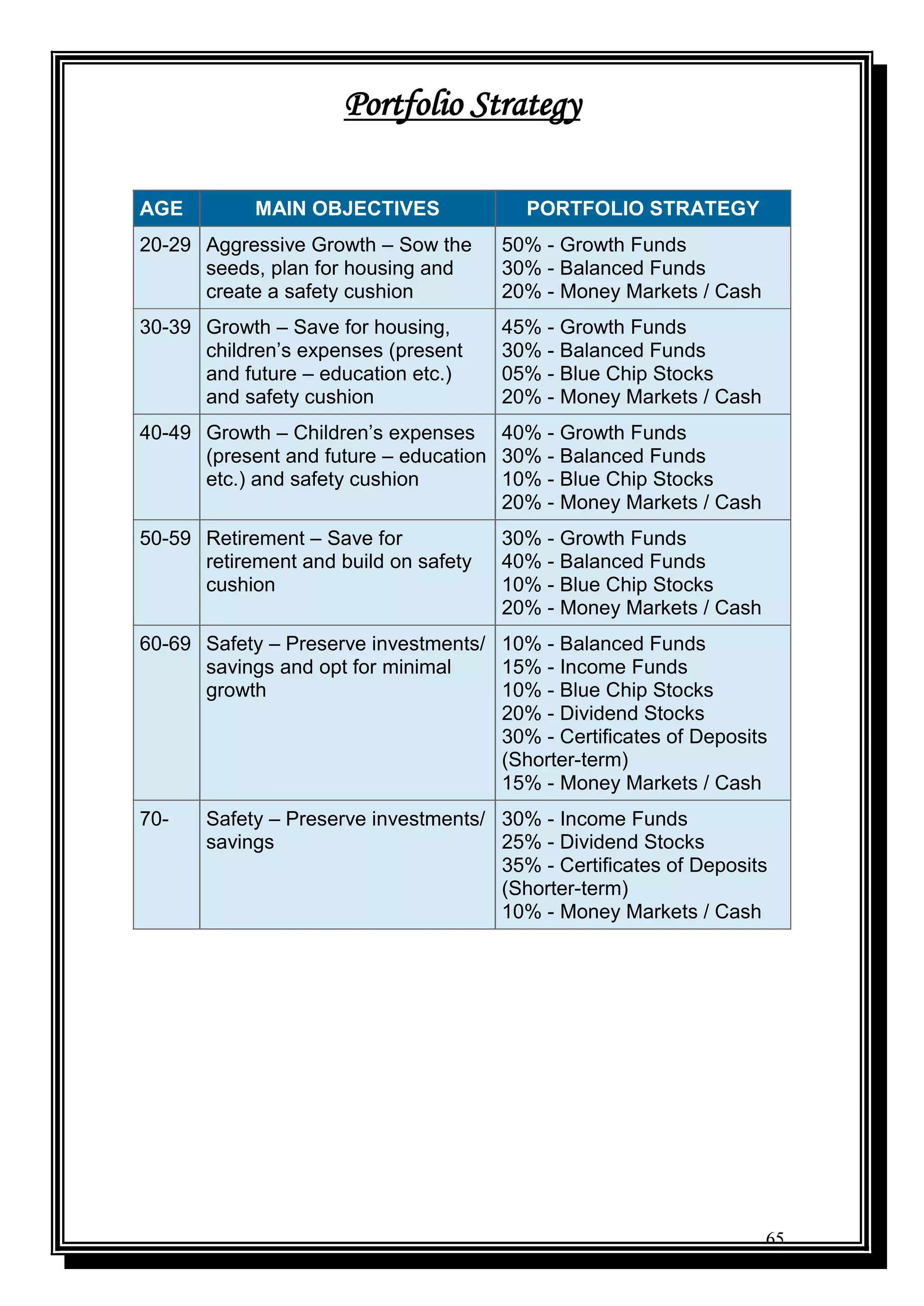

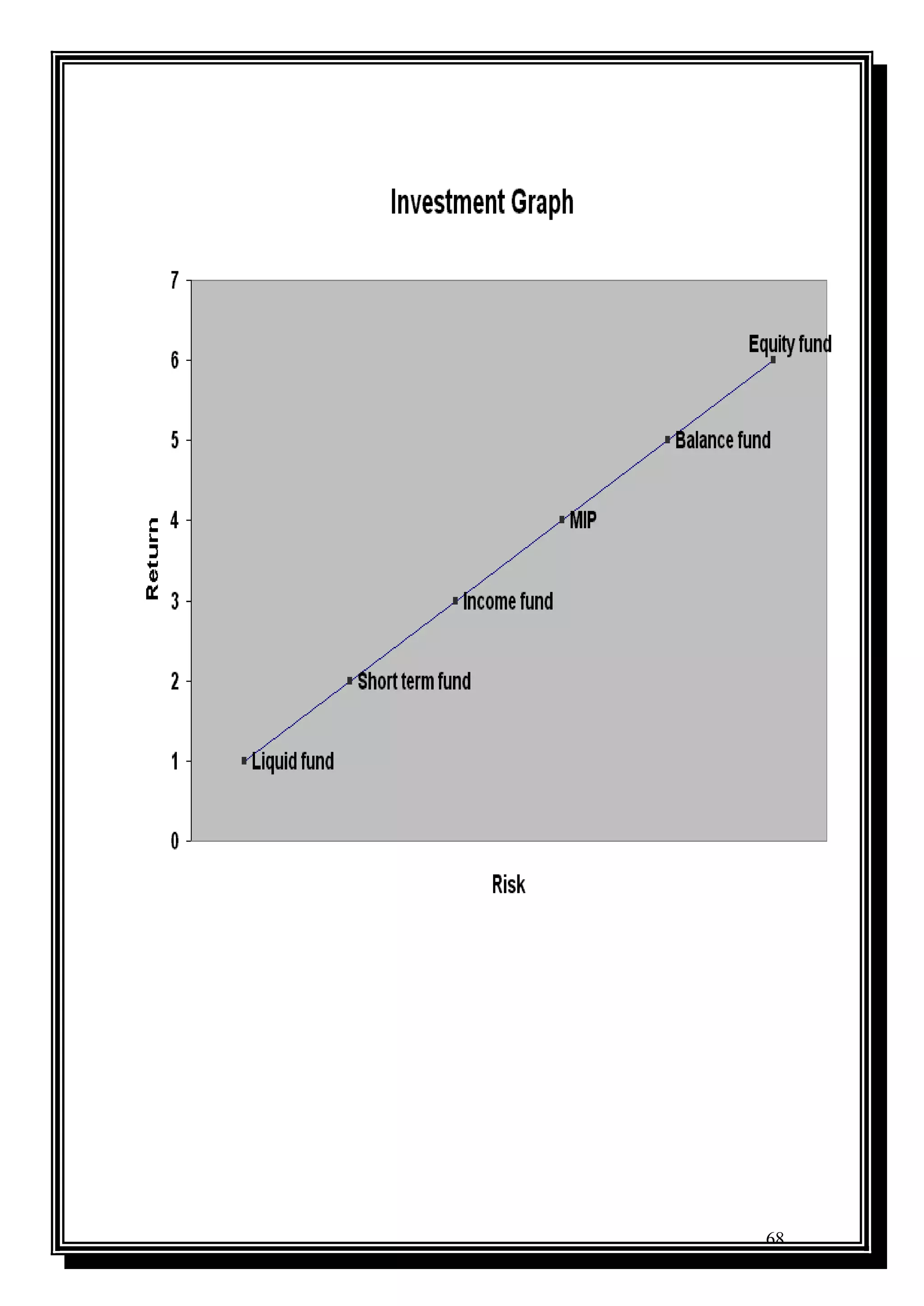

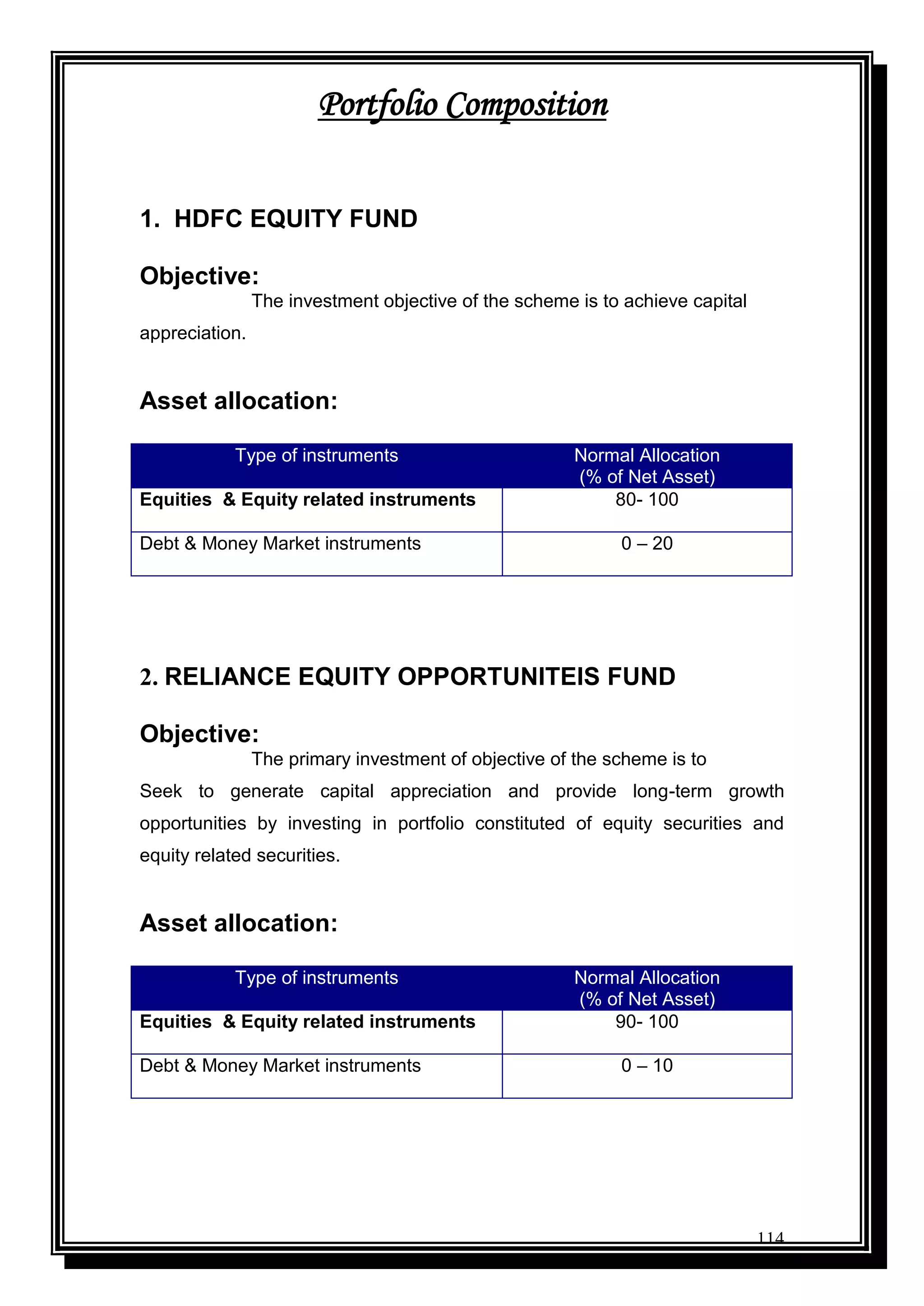

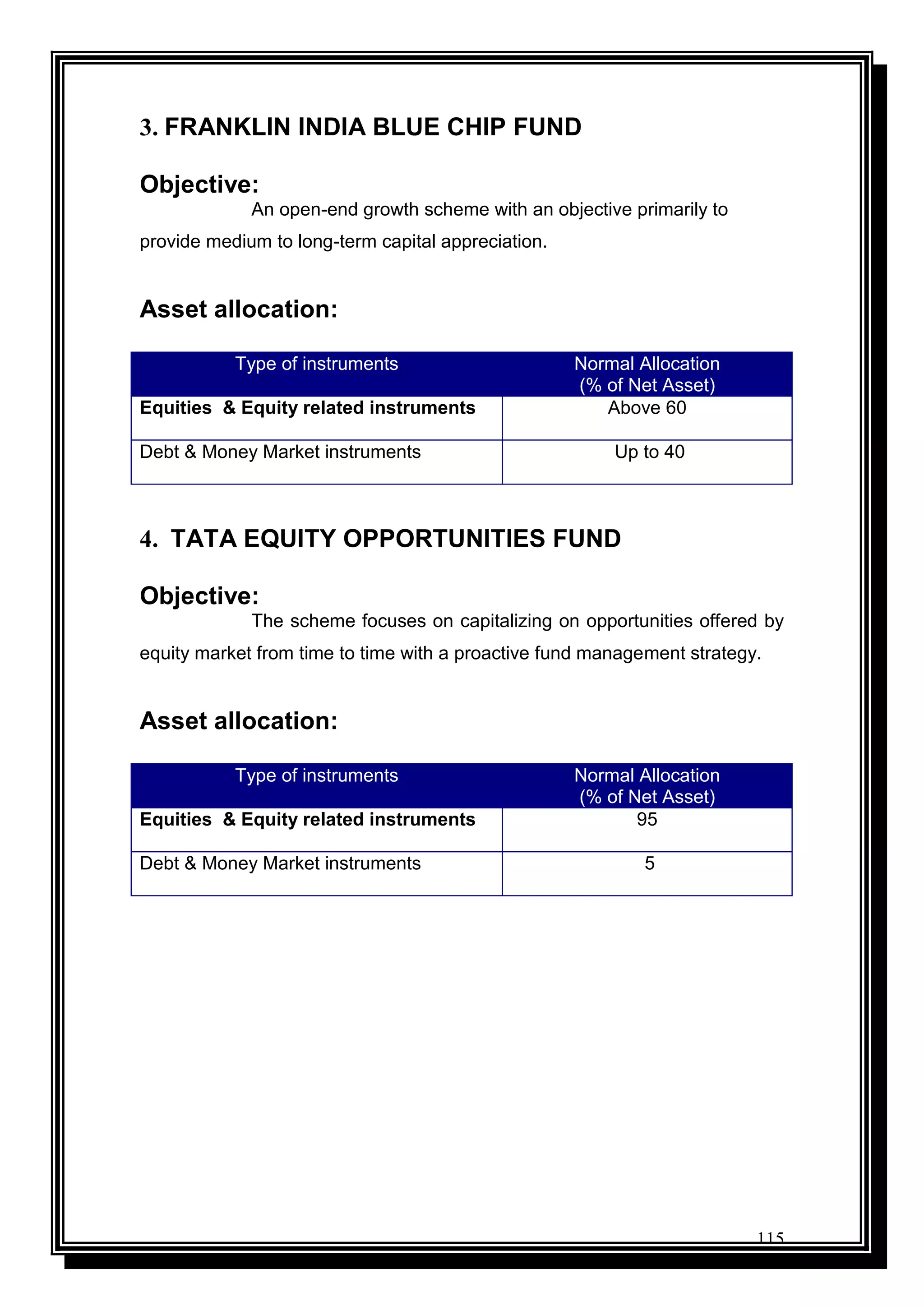

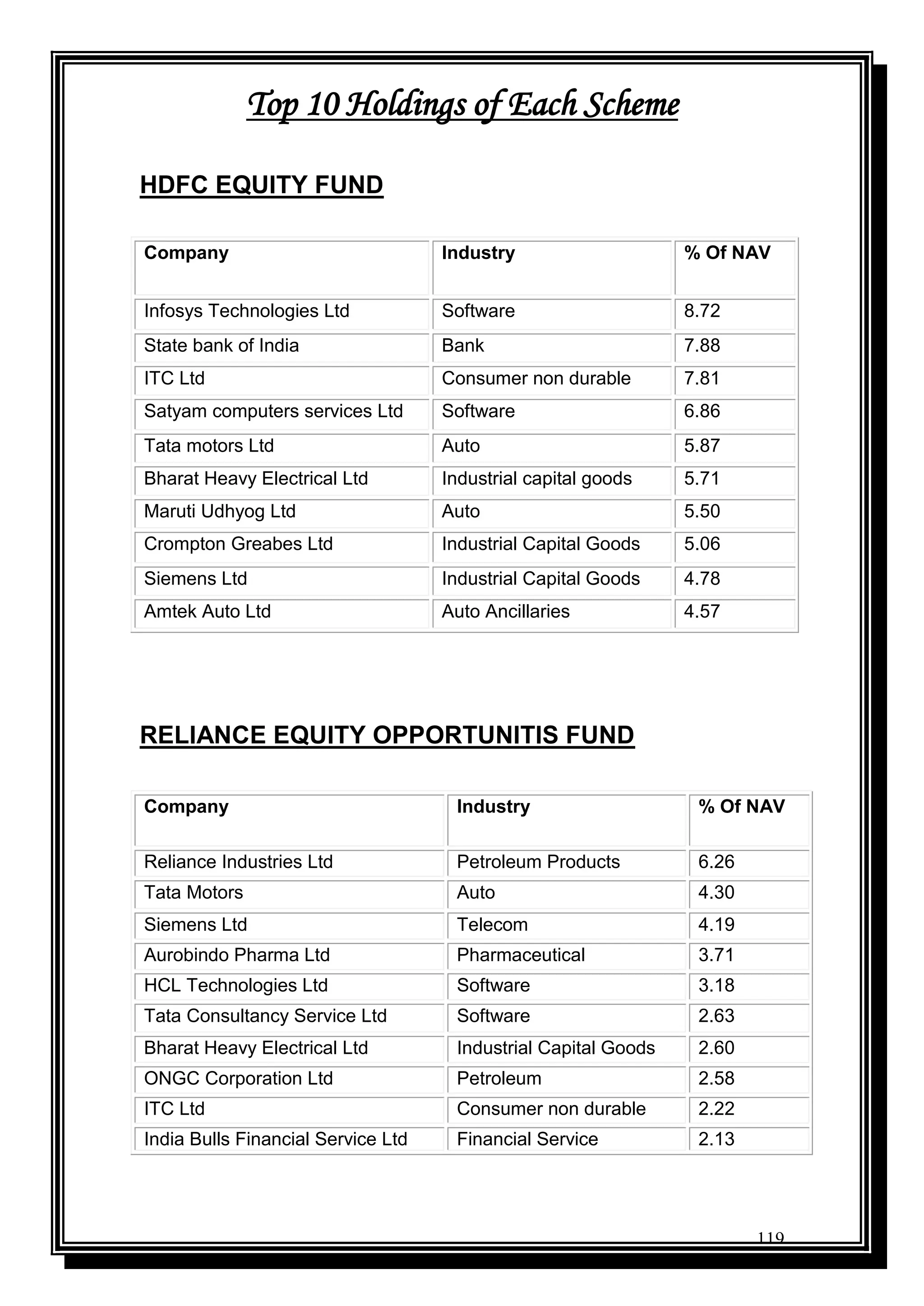

Various mutual fund schemes offered by HDFC, their features, target investors, and investment strategies.

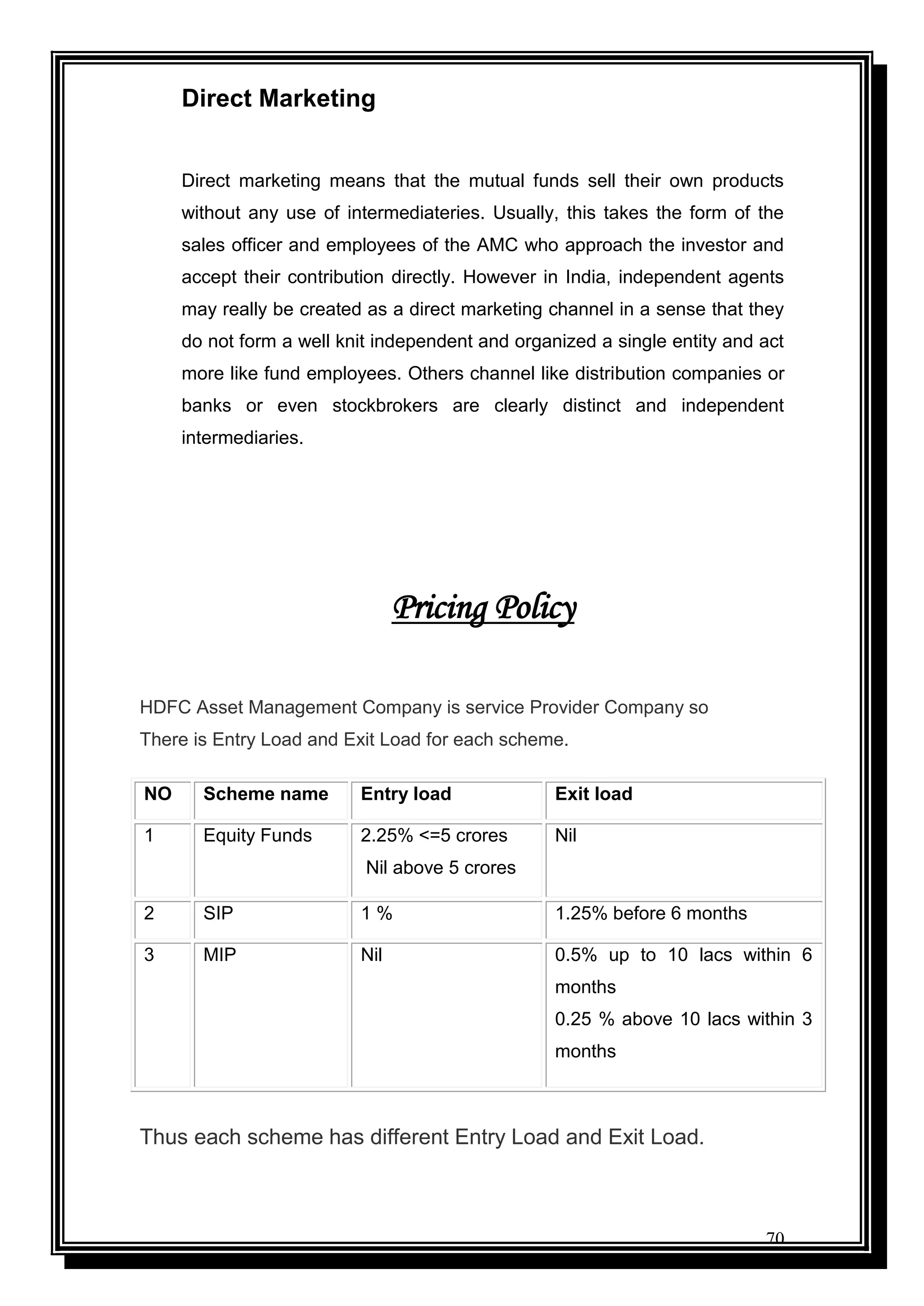

Overview of distribution channels utilized by mutual funds such as individual agents, banks, and direct marketing.

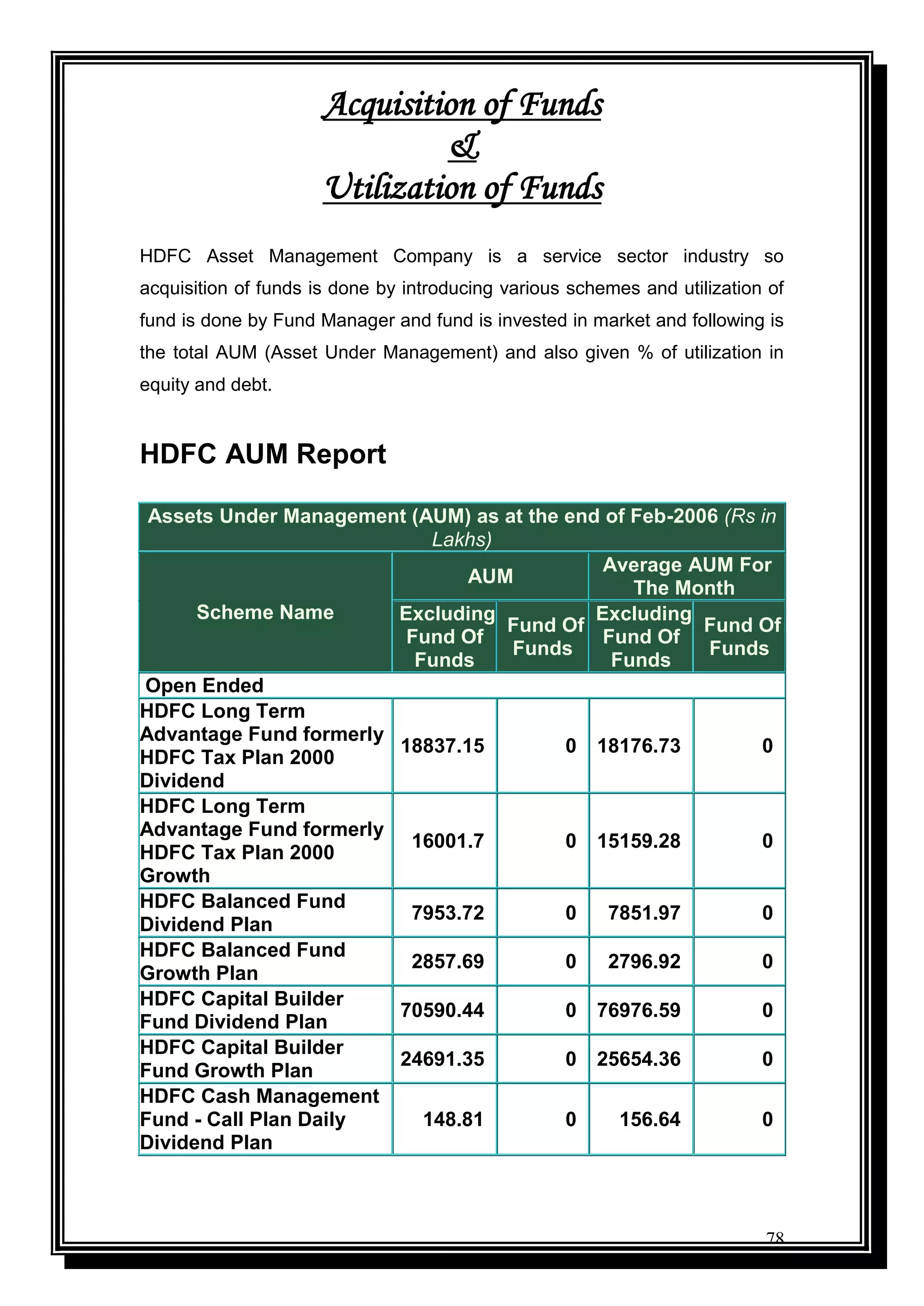

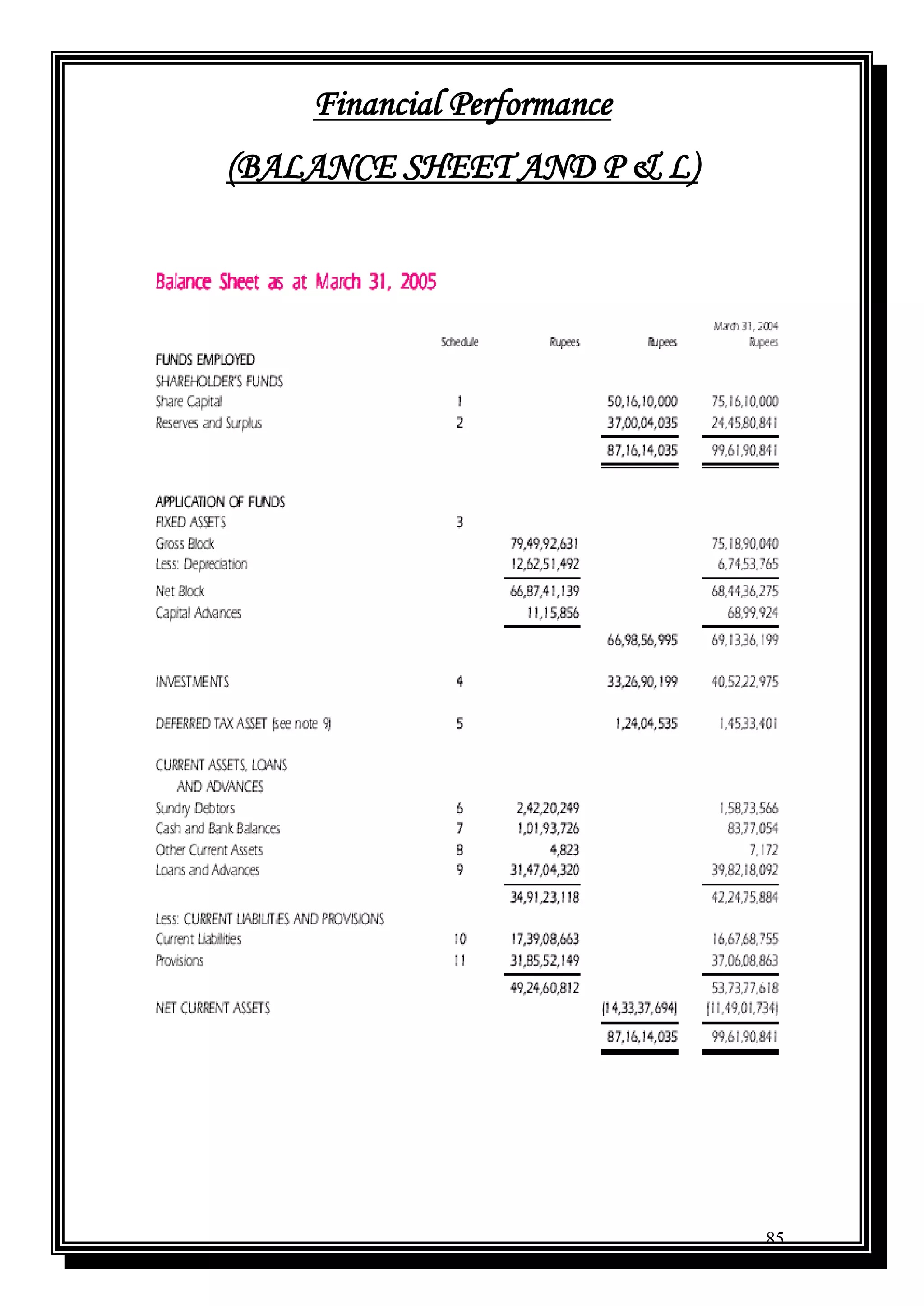

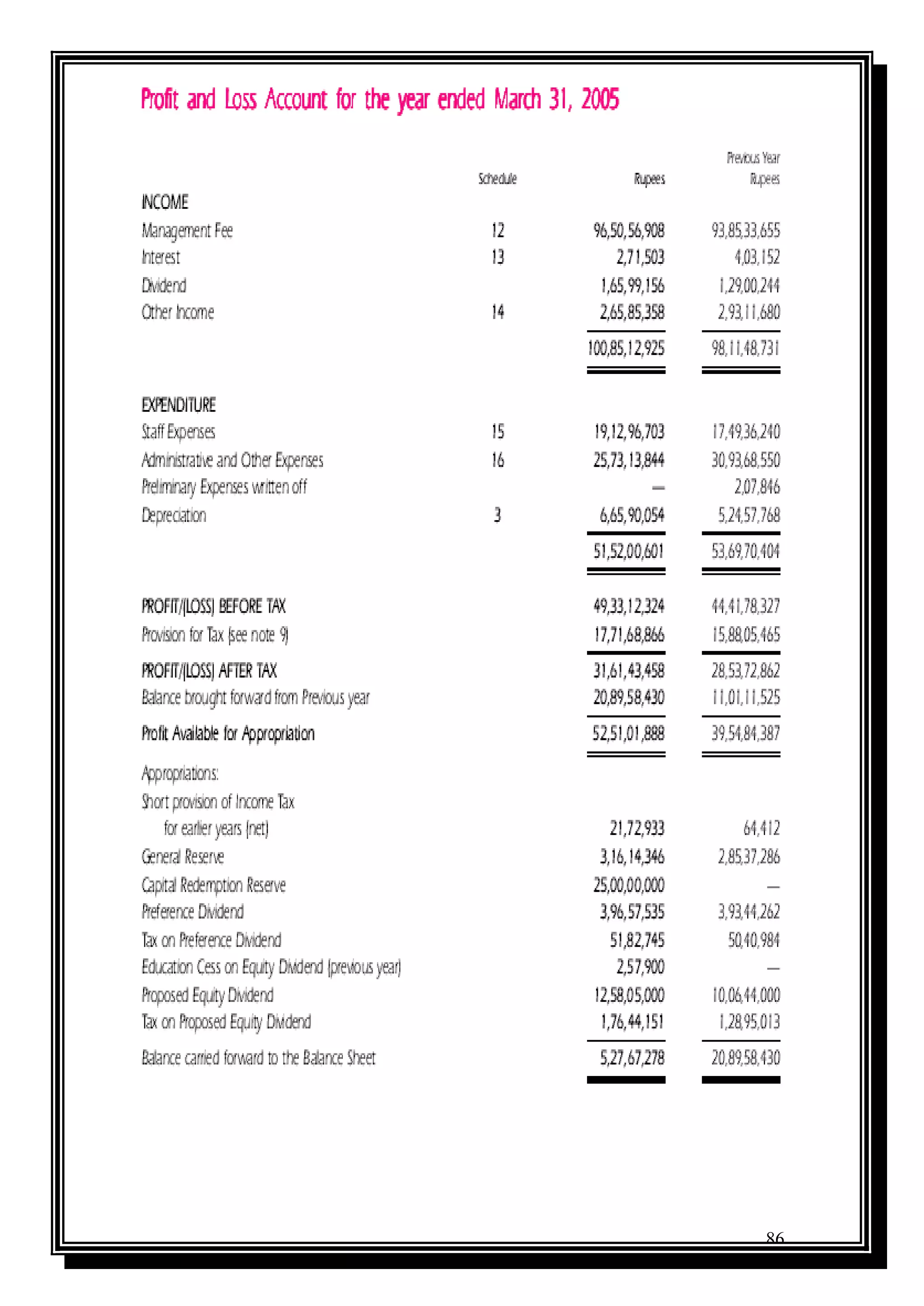

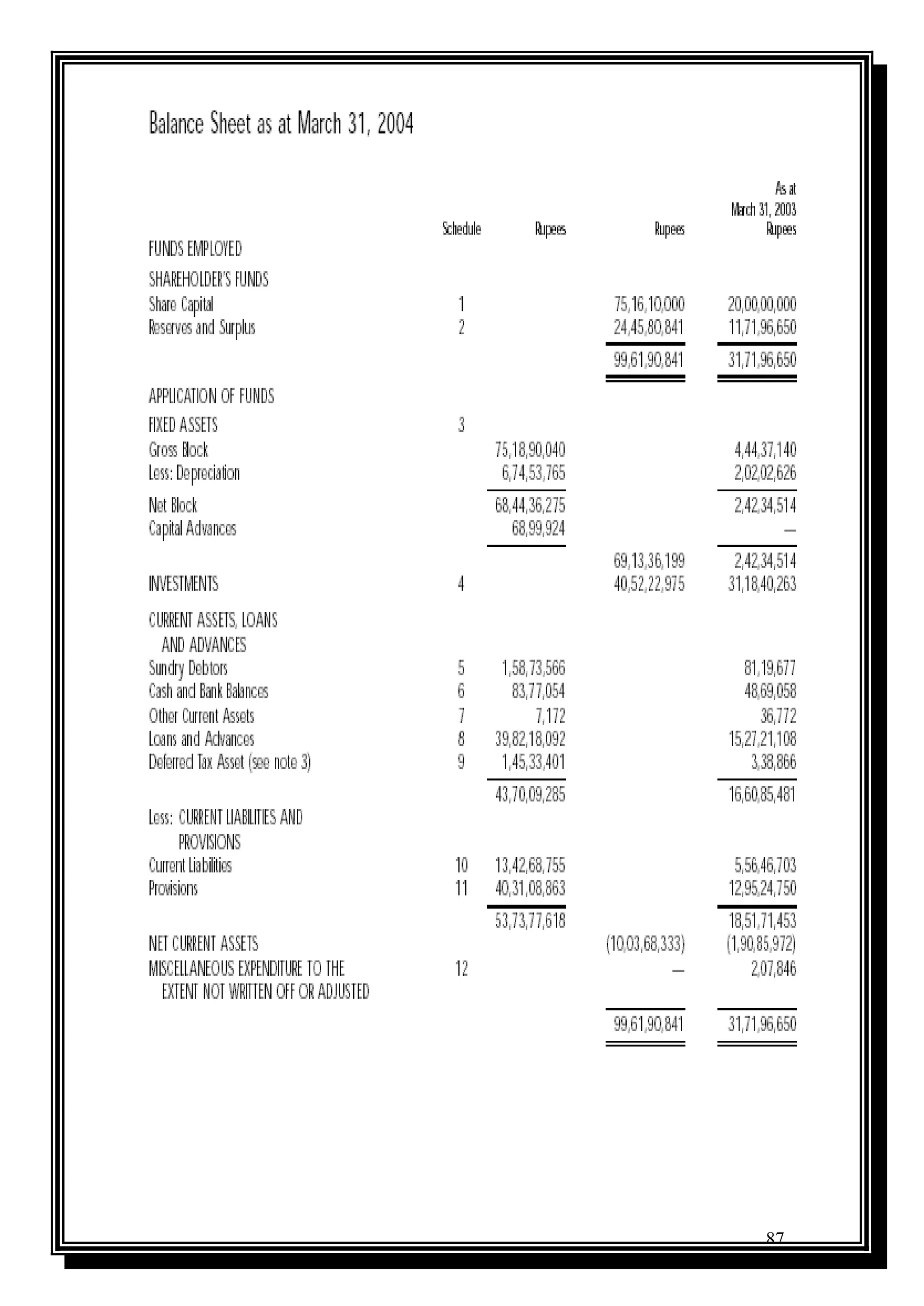

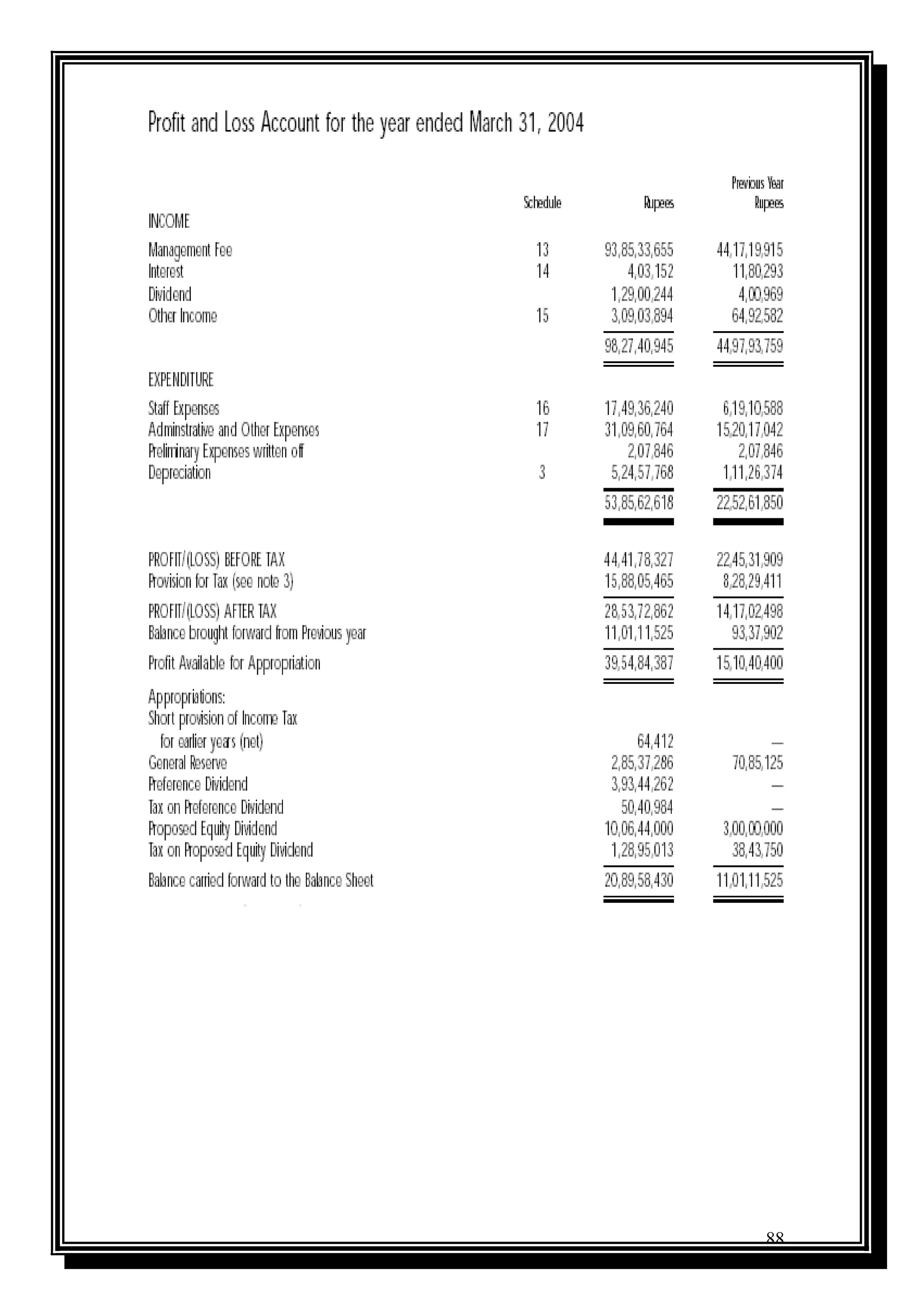

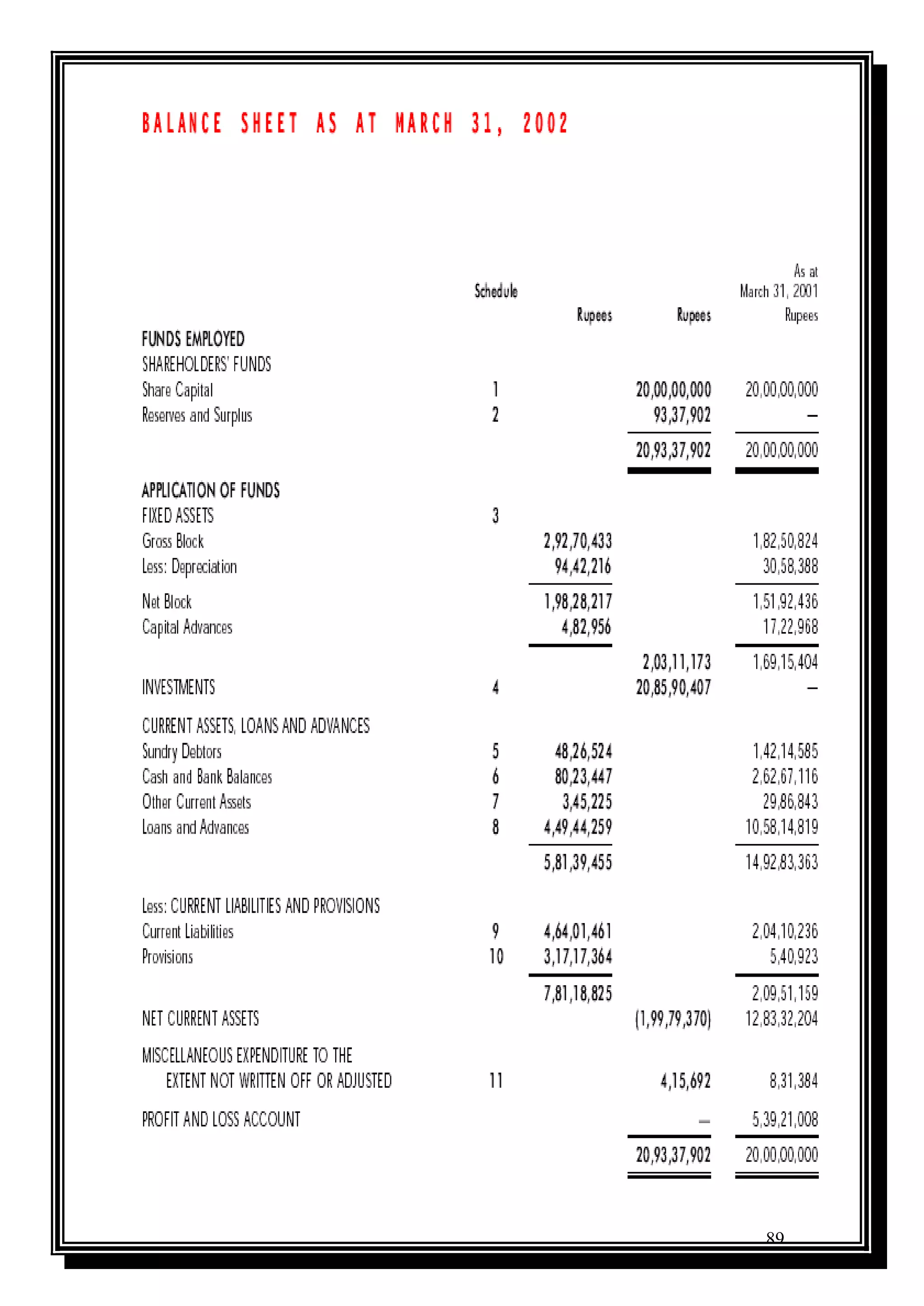

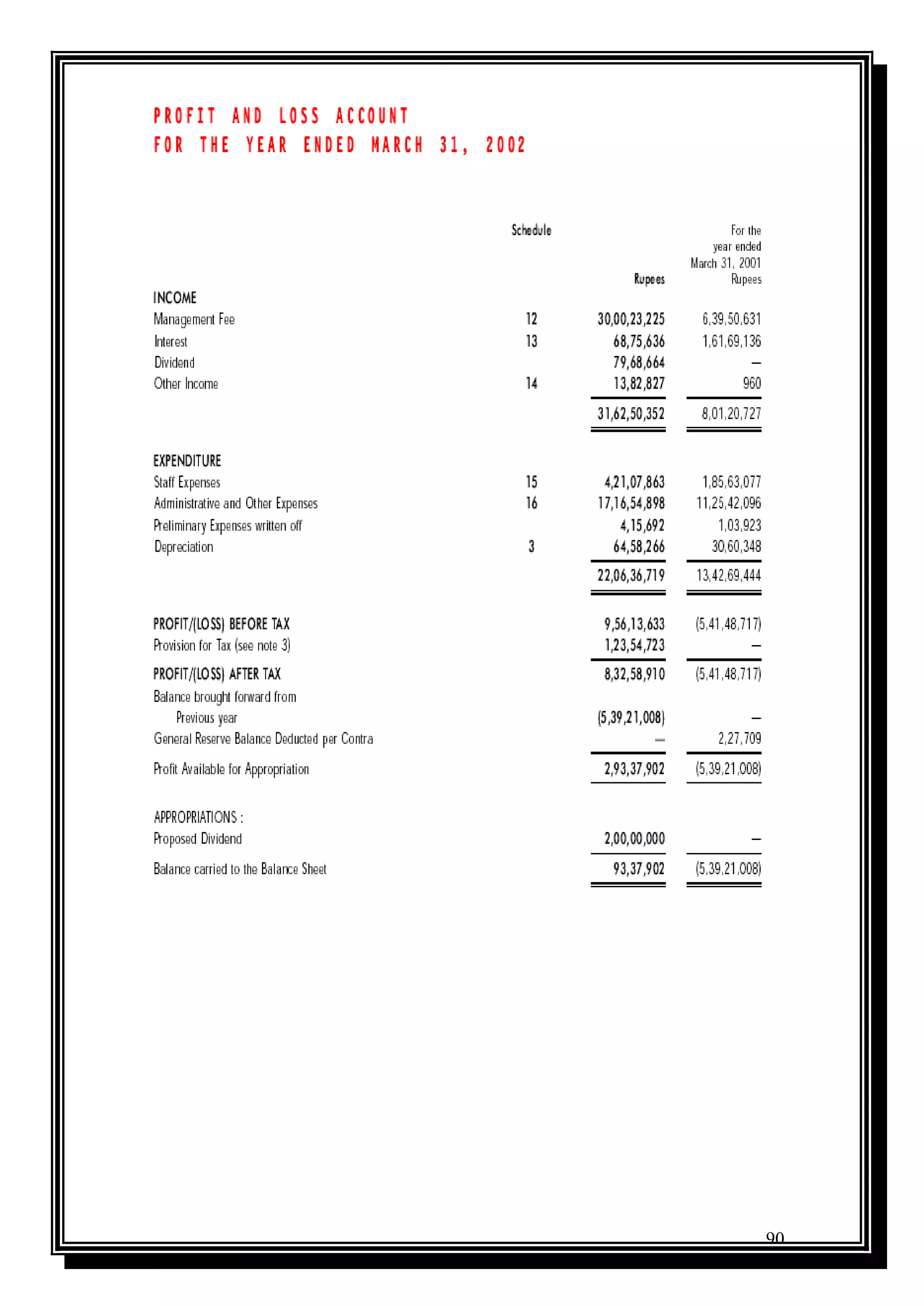

Details of operational aspects, financial acquisition, and management of funds, highlighting HDFC's AUM performance.

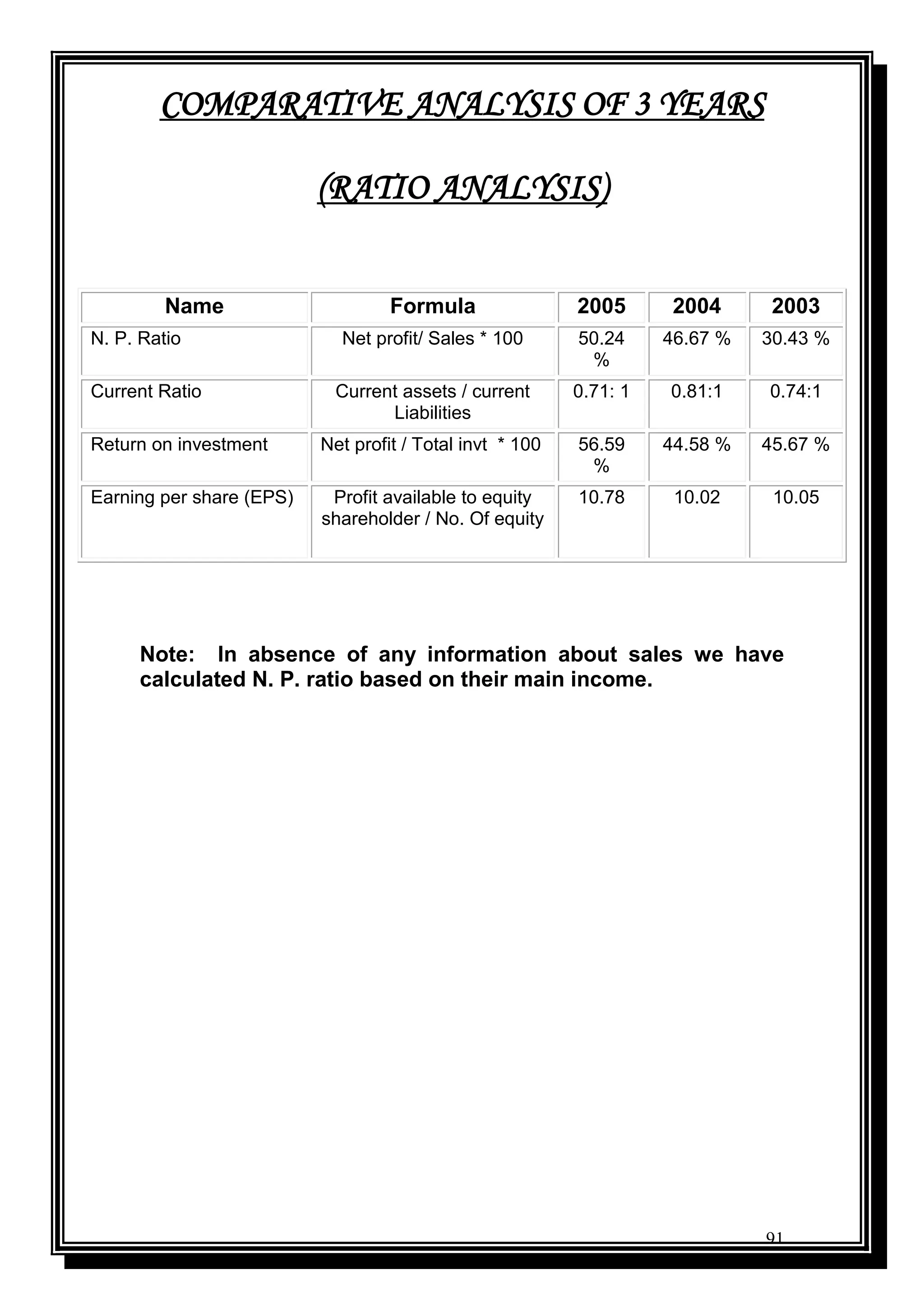

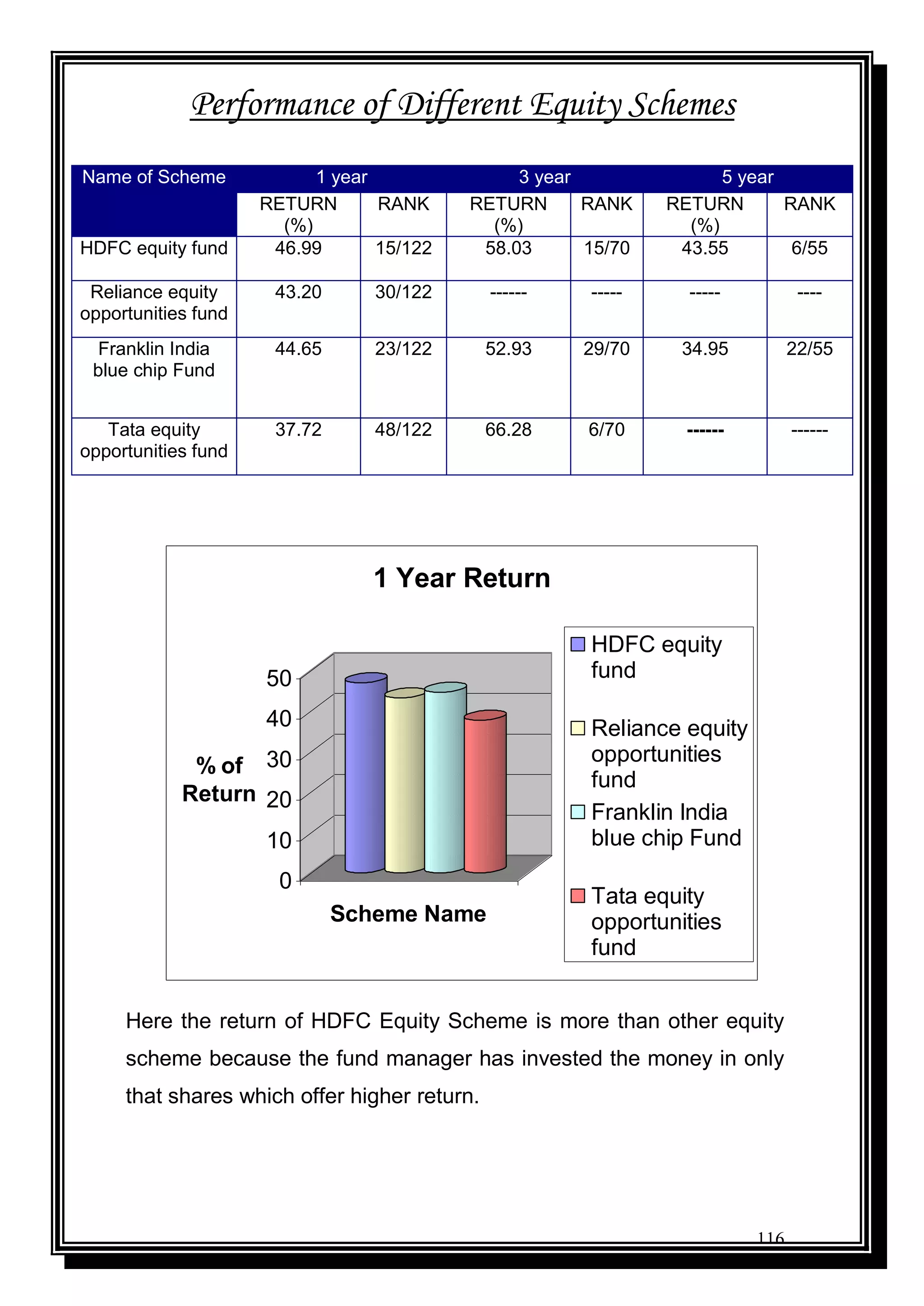

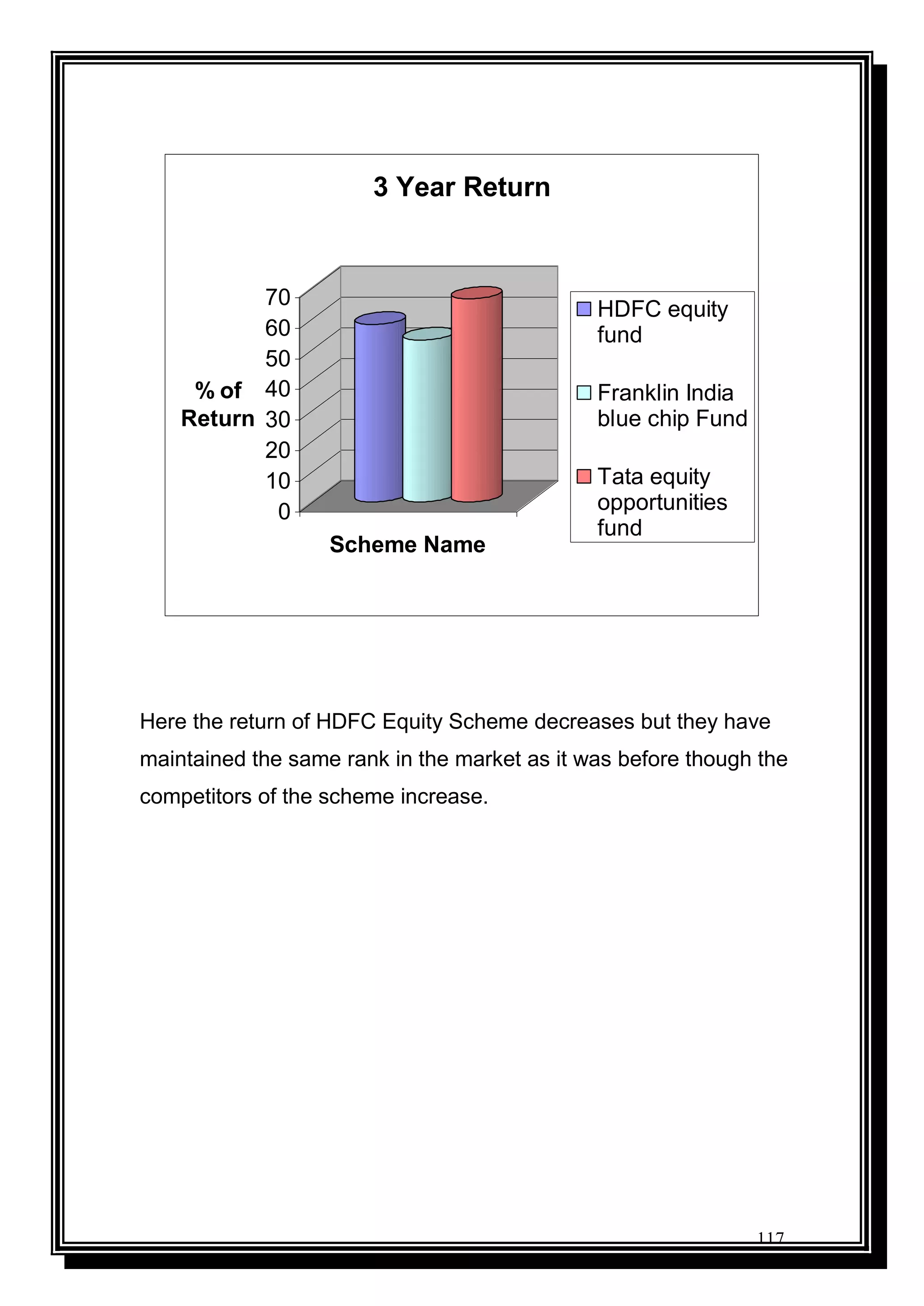

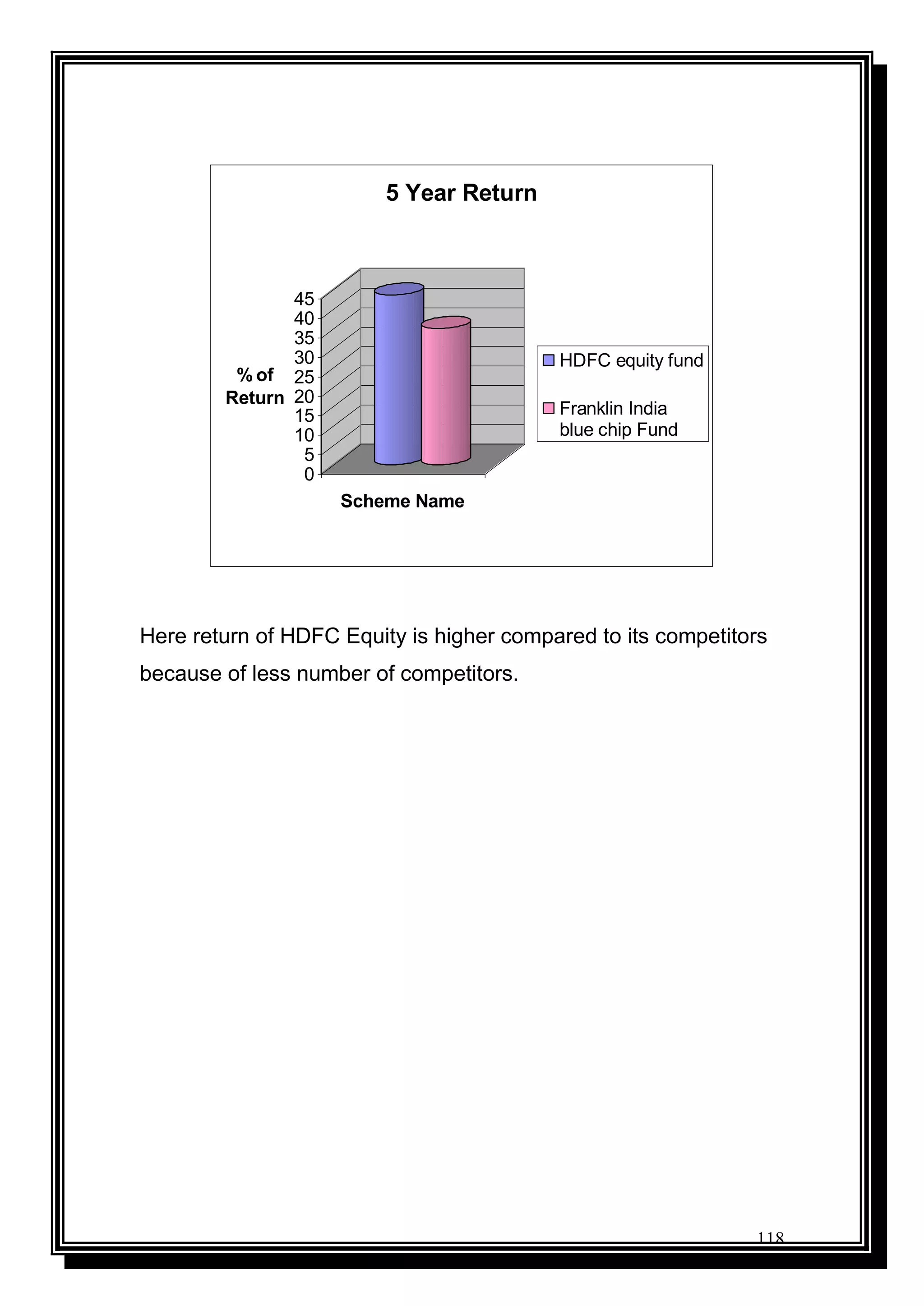

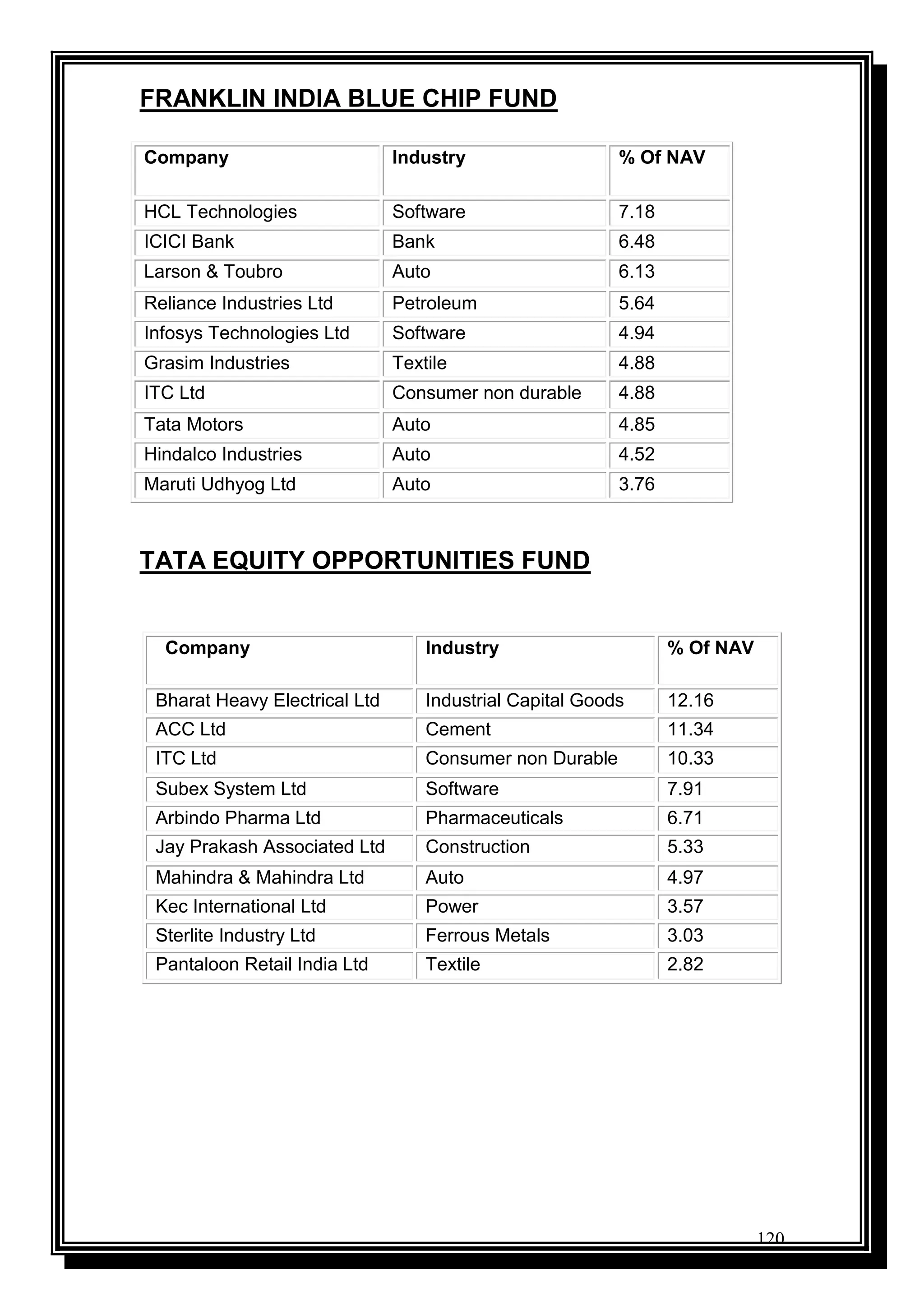

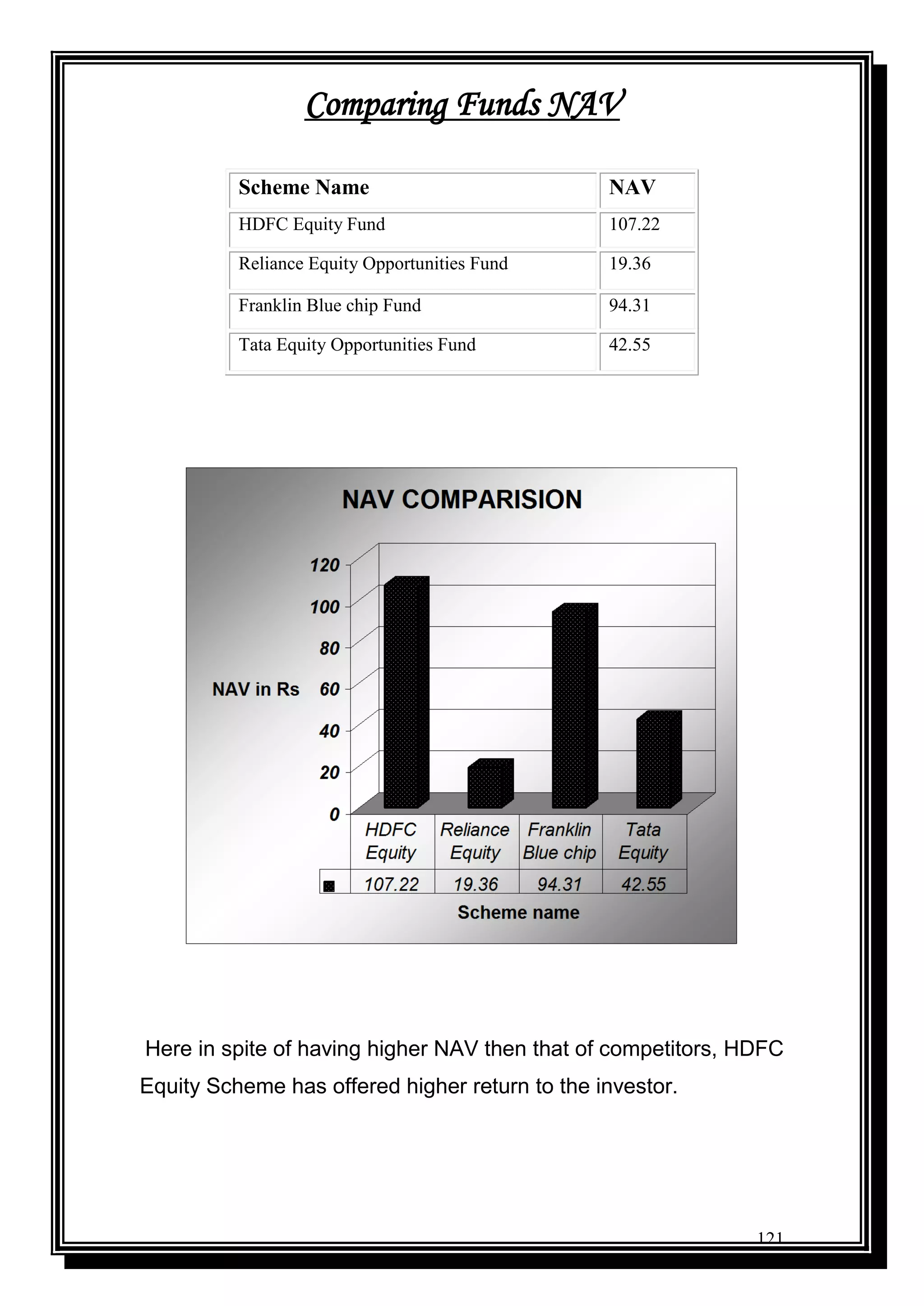

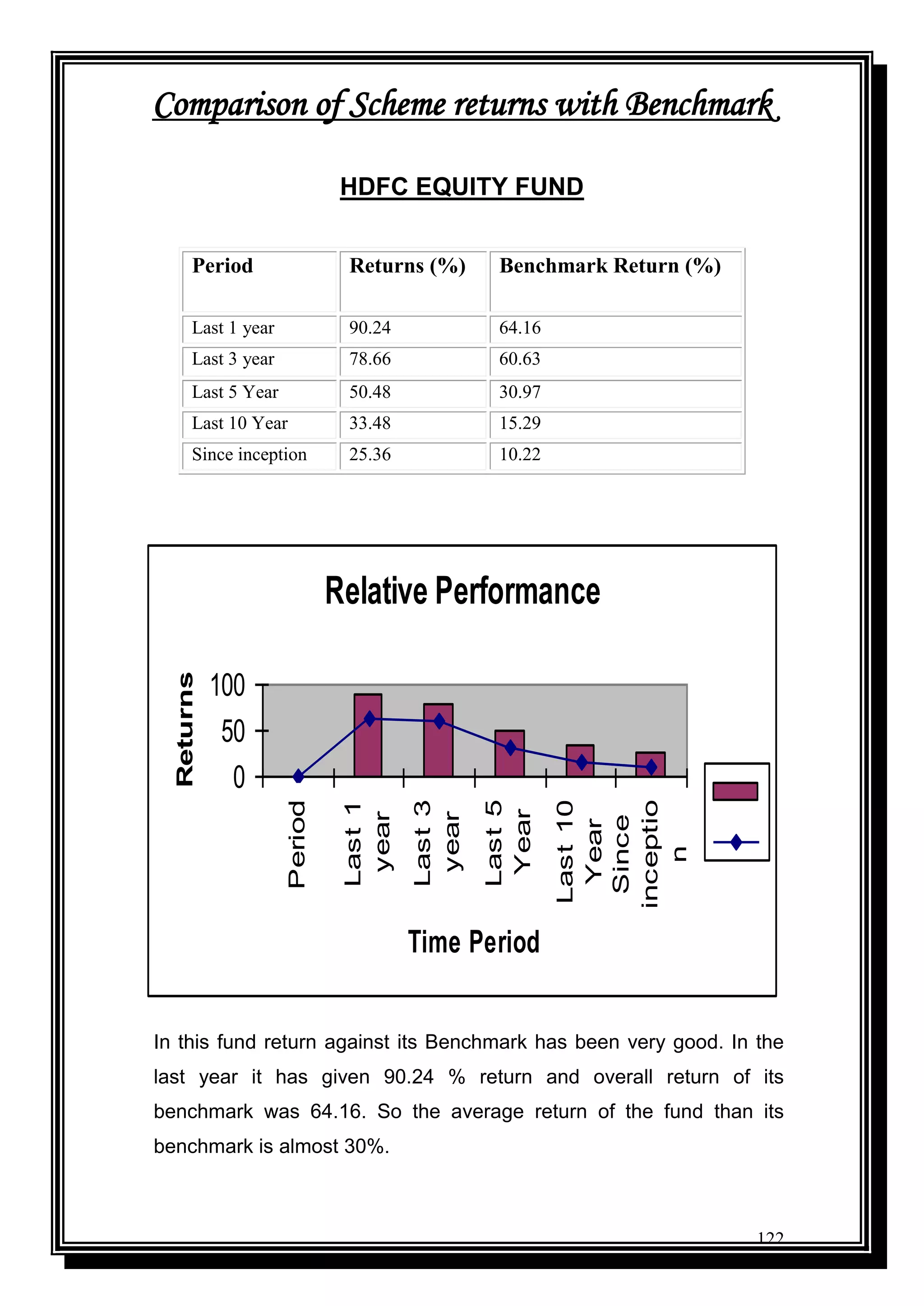

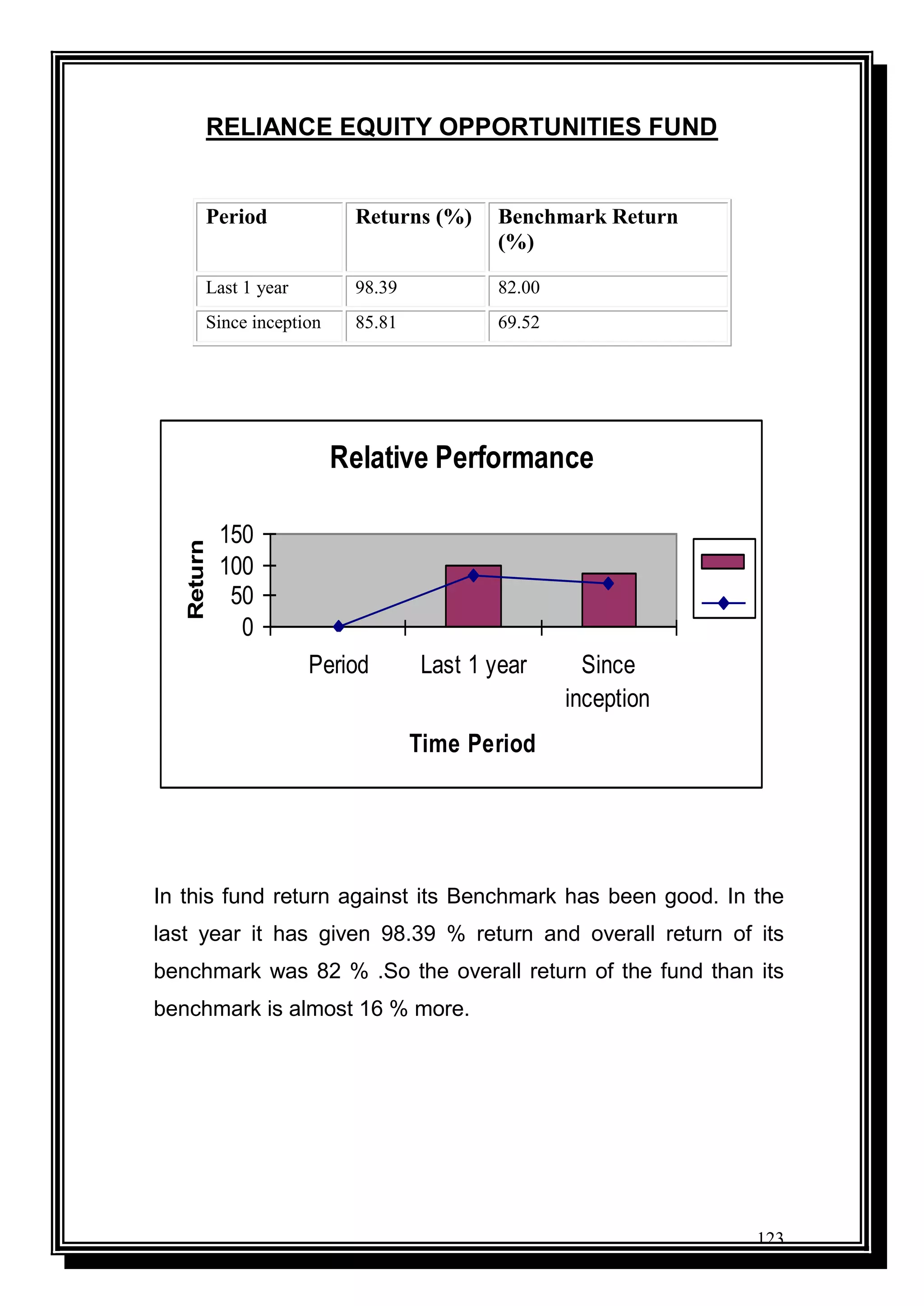

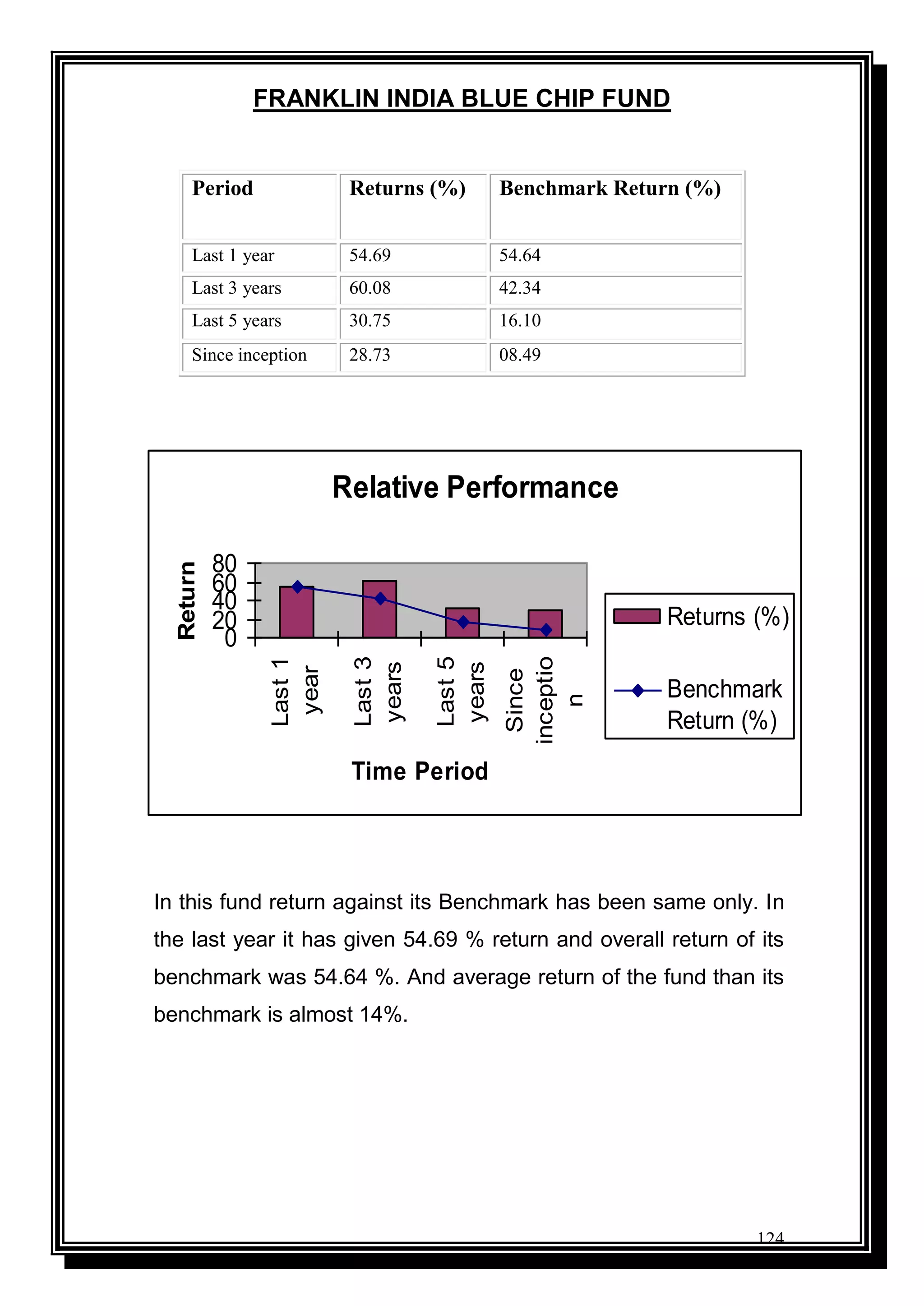

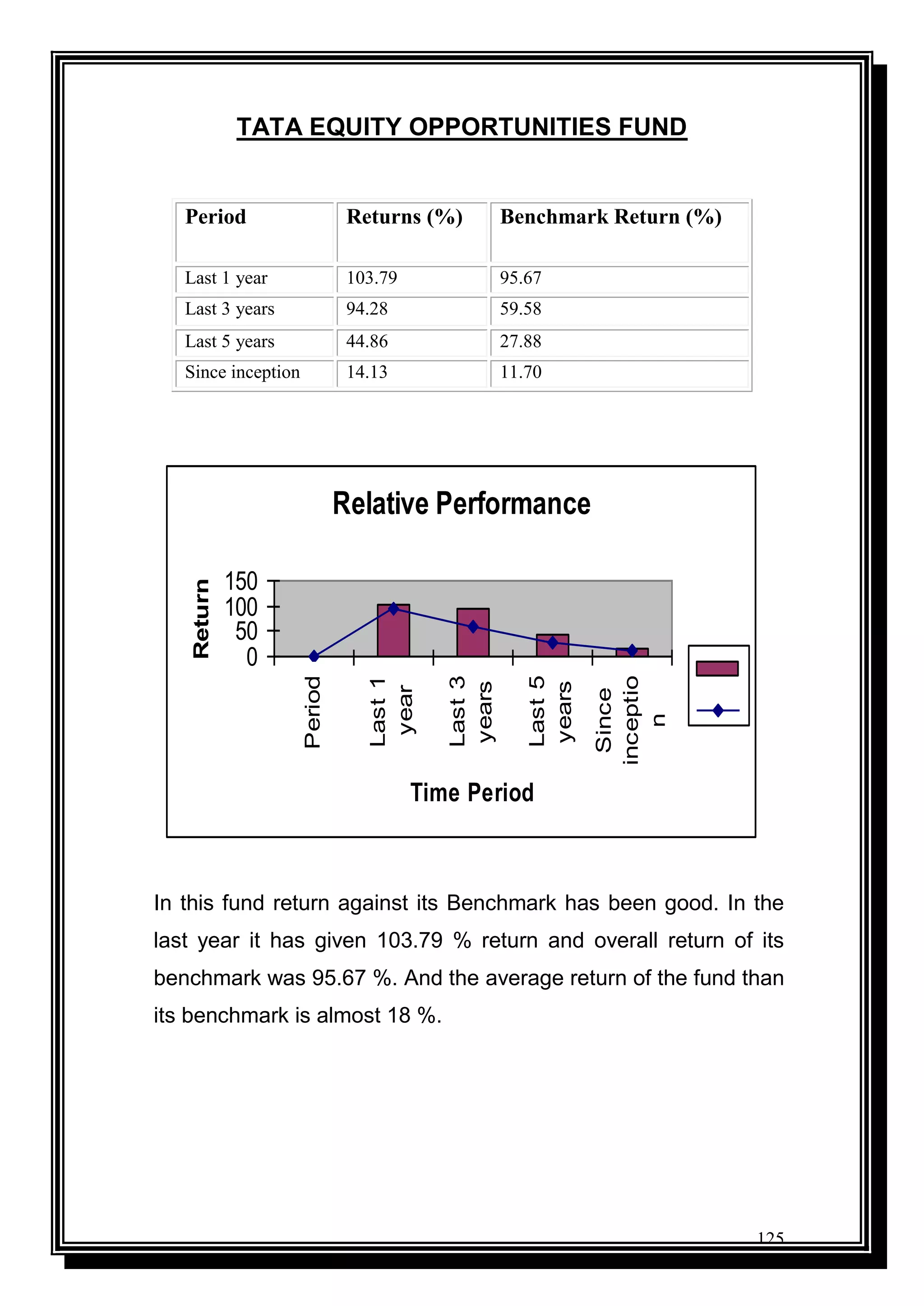

Comparative analysis of HDFC and its competitors' equity schemes through performance metrics and findings.

Conclusions drawn from the research findings, limitations of the study, and recommendations for HDFC's mutual fund strategies.