Downloaded 33 times

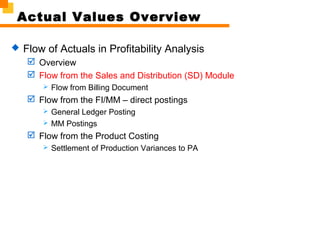

The document provides an overview of profitability analysis (CO-PA) in SAP. It discusses the objectives of CO-PA which include understanding functions, master data, sources of actual values, and planning. It also outlines the course content which covers CO-PA structures, actual value flows from sales, FI/MM, and product costing, planning methods and versions, and the CO-PA information system.