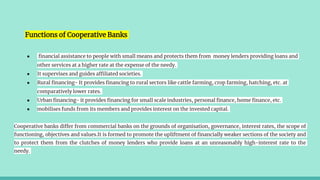

Cooperative banks are voluntary associations owned and operated by their members. They are established to provide self-help and mutual assistance to their members. In India, cooperative banks are registered under state cooperative societies acts and regulated by the Reserve Bank of India.

There are different types of cooperative banks operating at various levels. Primary cooperative credit societies (PCCS) operate at the village level and provide financial services to farmers. Central cooperative banks (CCB) operate at the district level, while state cooperative banks (SCB) work at the state level and act as the apex body. Urban cooperative banks cater to urban and semi-urban areas. The long-term cooperative institutions include primary agricultural and rural development banks.

Co

![STATUTES

In India, co-operative banks are registered under the States Cooperative Societies Act. They also come under the

regulatory ambit of the Reserve Bank of India (RBI) under two laws, namely, the Banking Regulations Act, 1949, and the

Banking Laws (Co-operative Societies) Act, 1965.They were brought under the RBI's watch in 1966, a move which brought

the problem of dual regulation along with it.

Sec3 NIA “banker” includes any person acting as a banker and any post office savings bank].Sec56 ref to bank/bank co.

includes coop bank

BRA Sec 5 (b) "banking" means the accepting, for the purpose of lending or investment, of deposits of money from

the public, repayable on demand or otherwise, and withdrawal by cheque, draft, order or other wise;

(c) "banking company" means any company which transacts the business of banking1 [in India]; Explanation.--

Any company which is engaged in the manufacture of goods or carries on any trade and which accepts deposits of

money from the public merely for the purpose of financing its business as such manufacturer or trader shall not be

deemed to transact the business of banking within the meaning of this clause;

As per sec. 3 BRA, act dont apply to (a) a primary agricultural credit society (b) a co-operative land mortgage bank; and

(c) any other co-operative society, except in the manner and to the extent specified in Part V.]](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-8-320.jpg)

![STATUTE CONTD.

sec[7. Use of words "bank", "banker", "banking" or "banking company"

(1) No company other than a banking company shall use as part of its name 2[or in connection with its business] any

of the words "bank", "banker" or "banking" and no company shall carry on the business of banking in India unless

it uses as part of its name at least one of such words.

(2) No firm, individual or group of individuals shall, for the purpose of carrying on any business, use as part of its or

his name any of the words "bank", "banking" or "banking company".

(3)Nothing in this section shall apply to (a) a subsidiary of a banking company formed for one or more of the

purposes mentioned in sub-section (1) of section 19, whose name indicates that it is a subsidiary of that banking

company; 17 (b) any association of banks formed for the protection of their mutual interests and registered under

section 25 of the Companies Act, 1956 (1 of 1956](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-9-320.jpg)

![3.NABARDA 2(u) “State co-operative bank”

principal co-operative society in a State, the primary object of which is the financing of other co-operative

societies in the State: Provided that in addition to such principal society in a State, or where there is no such

principal society in a State, the State Government may declare any one or more co-operative societies carrying on

business in that State to be also or to be a State cooperative bank or State co-operative banks within the meaning

of this definition;

● The state co-operative bank is a federation of central co-operative bank and acts as a watchdog of the

co-operative banking structure in the state.

● It procures funds from share capital, deposits, loans and overdrafts from the Reserve Bank of India.

● The state co-operative banks lend money to central co-operative banks and primary societies and not

directly to the farmers.

5cciiia , BRA "multi-State co-operative bank" means a multi-State co-operative society which is a primary co-

operative bank;] ; 3[(cciiib) "multi-State co-operative society" means a multiState co-operative society

registered as such under any Central Act for the time being in force relating to the multiState co-operative

societies but does not include a national co-operative society and a federal co-operative;]](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-12-320.jpg)

![INTERNATIONAL ORIGINS:0………..scotland

in 1498. The Shore Porters Society, for example, claims to be one of the world’s first cooperatives, being

established in Aberdeen, Scotland, It was a removal, haulage and storage company, originating as a group of

porters working in Aberdeen Harbor.

The first documented consumer cooperative was founded [1] in a barely furnished cottage in Fenwick, East in

1769,Ayrshire, when local weavers manhandled a sack of oatmeal into John Walker's whitewashed front room and

began selling the contents at a discount, forming the Fenwick Weavers' Society.

A further example was in New Lanark, Scotland where Robert Owen (1771–1858) and other mill owners agreed to

limit their returns on invested capital and to use residual profits that accrued for the benefit of the entire

community (Royle, 1998).

In the decades that followed more Scottish cooperatives formed, including Lennoxtown Friendly Victualling

Society, founded in 1812. The focus of the Lennoxtown group was operation of the busy Lennox Mill, where tenants

of the Woodhead estate brought their corn to be ground. Another significant event of the group was the

establishment of the calico printing works at Lennoxmill on a site adjacent to the corn mill. The printing of calico

and other cotton cloth was soon established as a major industry in the area.](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-27-320.jpg)

![International origins:.......UK ,ROCHDALE

The cooperative movement began in Europe in the 19th century, primarily in Britain and France.

The industrial revolution and the increasing mechanisation of the economy transformed society and threatened the

livelihoods of many workers. The concurrent labour and social movements and the issues they attempted to address

describe the climate at the time. These movements were supported by governments of the respective countries. This

success was achieved due to the failure of the commercial banks to fund and support the needs of small business owners

and ordinary people who were outside the formal banking net. Cooperative banks helped overcome the vital market

imperfections and serviced the poorer layers of society.

By 1830, there were several hundred co-operatives.[3] Some were initially successful, but most cooperatives founded in

the early 19th century had failed by 1840.[4] However, Lockhurst Lane Industrial Co-operative Society (founded in 1832

and now Heart of England Co-operative Society), and Galashiels and Hawick Co-operative Societies (1839 or earlier,

merged with The Co-operative Group) still trade today.[5][6]

It was not until 1844 when the Rochdale Society of Equitable Pioneers established the "Rochdale Principles" on which

they ran their cooperative, that the basis for development and growth of the modern cooperative movement was

established.[7] though these principles helped spread cooperative movement in many parts of Europe, in British

Isles it came from the revivalist Christian movement and found high acceptance with working class and lower middle

class segments of society.](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-30-320.jpg)

![Rochdale Principles of Cooperative movement

Rochdale Principles are a set of ideals for the operation of cooperatives. They were first set out in 1844 by the Rochdale

Society of Equitable Pioneers in Rochdale, England and have formed the basis for the principles on which co-operatives

around the world continue to operate. The implications of the Rochdale Principles are a focus of study in co-operative

economics. The original Rochdale Principles were officially adopted by the International Co-operative Alliance (ICA) in

1937 as the Rochdale Principles of Co-operation. Updated versions of the principles were adopted by the ICA in 1966 as

the Co-operative Principles and in 1995 as part of the Statement on the Co-operative Identity.[1]

Original version (adopted 1937)

1. Open membership.

2. Democratic control (one person, one vote).

3. Distribution of surplus in proportion to trade.

4. Payment of limited interest on capital.

5. Political and religious neutrality.

6. Cash trading (no credit extended).

7. Promotion of education](https://image.slidesharecdn.com/co-operativebankingsystem-210627165728/85/Co-operative-banking-system-origin-scope-object-32-320.jpg)