Downloaded 495 times

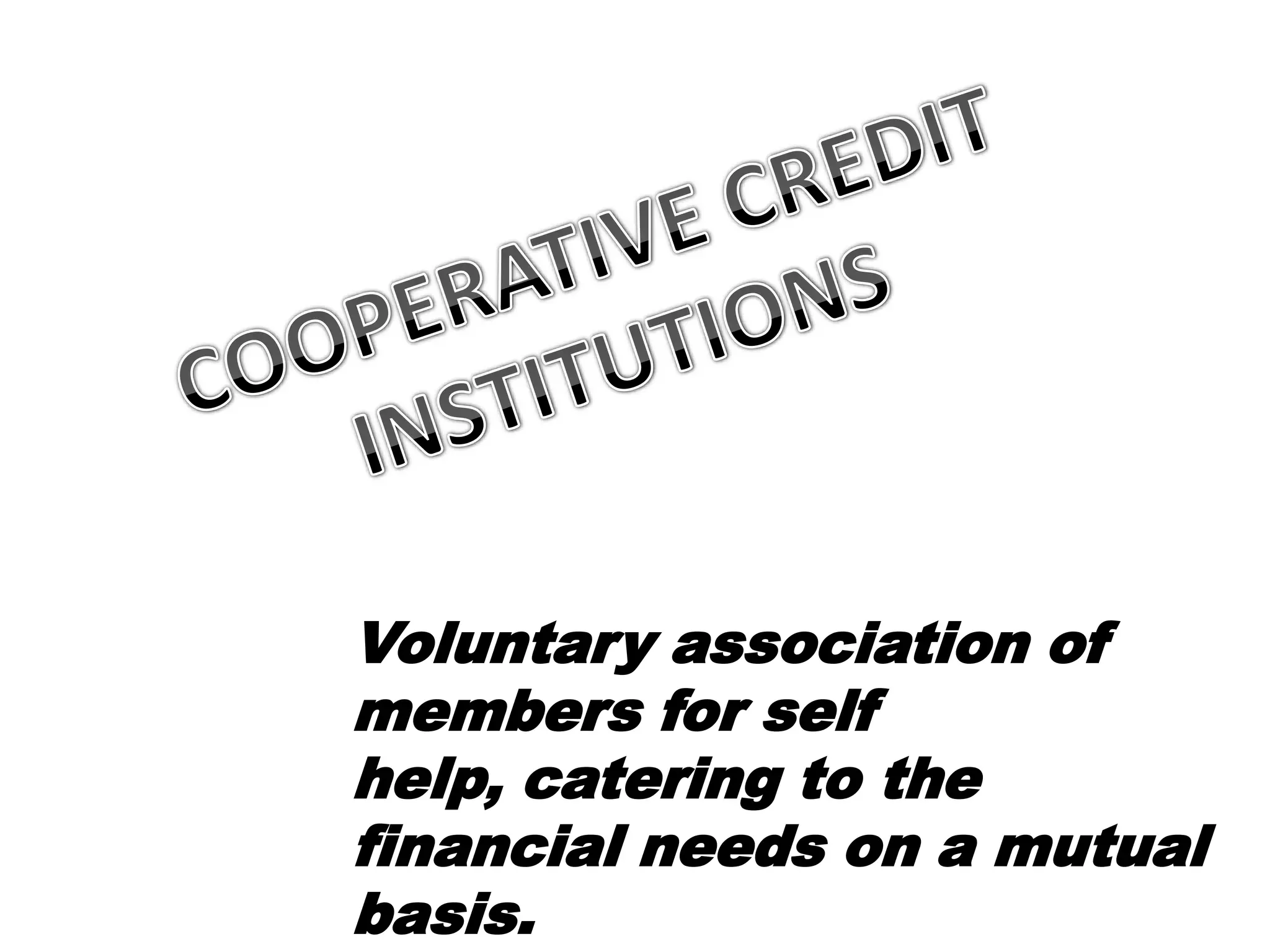

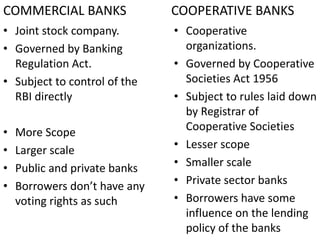

Cooperative banks are financial institutions that are owned and operated by their members. They are formed through voluntary association for purposes of self-help and meeting members' financial needs. Cooperative banks are owned and controlled by their members who are both customers and owners. They provide banking services like loans and deposits to their members.