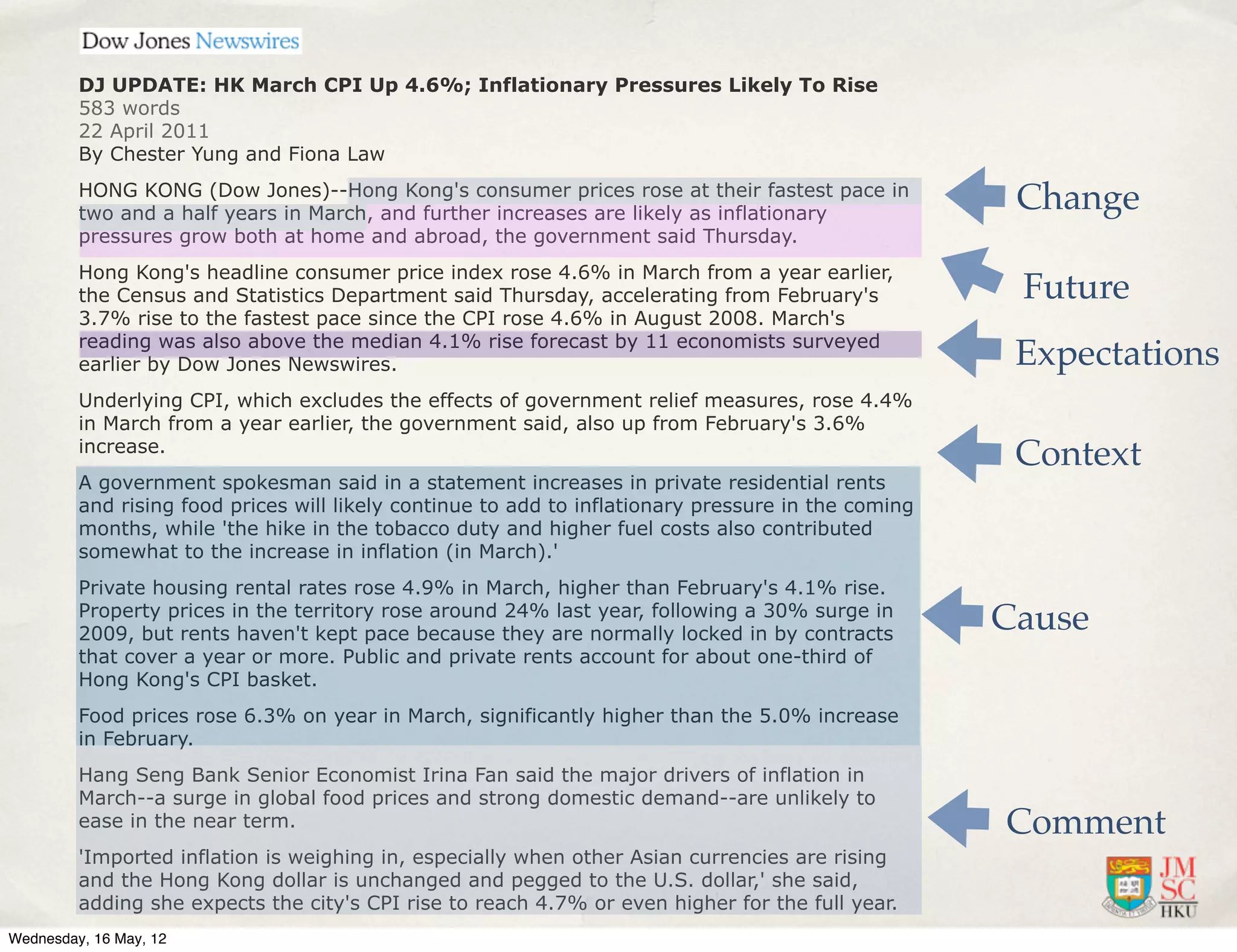

The document discusses key economic goals of governments including full employment, steady annual growth, and stable prices. It also covers various metrics that governments use to measure economic performance, such as output, employment, prices, and trade. Specific measures like the Consumer Price Index (CPI) and unemployment rate are explained in more detail. Problems with measuring economic data like defining unemployment and quality changes over time are also noted.

![INFLATION EFFECTS [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/inflationeffectsautosaved-230527083705-cdfd969a-thumbnail.jpg?width=640&height=640&fit=bounds)