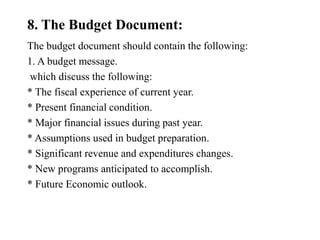

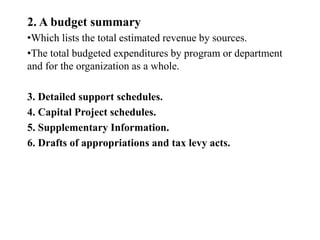

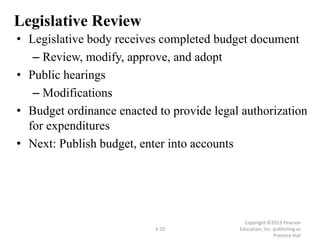

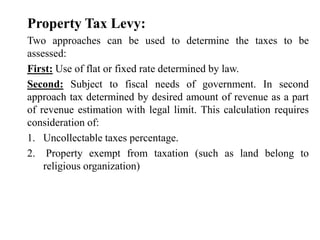

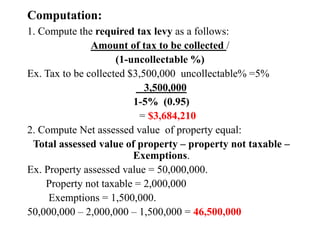

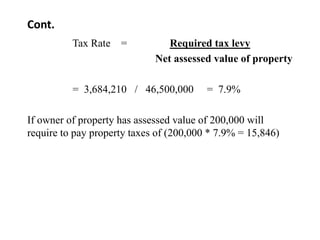

Chapter 3 discusses budgetary considerations in governmental accounting, emphasizing the importance of budgeting in resource allocation among competing services that governments provide to citizens. It outlines the types of budgets—operating, capital, and cash forecasts—and the budget process, which includes policy guidelines, budget calendars, revenue estimates, and expenditure requests. Additionally, it highlights the necessity of legislative review and the legal implications of budgetary decisions, along with methods for calculating property taxes and controlling spending.