Downloaded 11 times

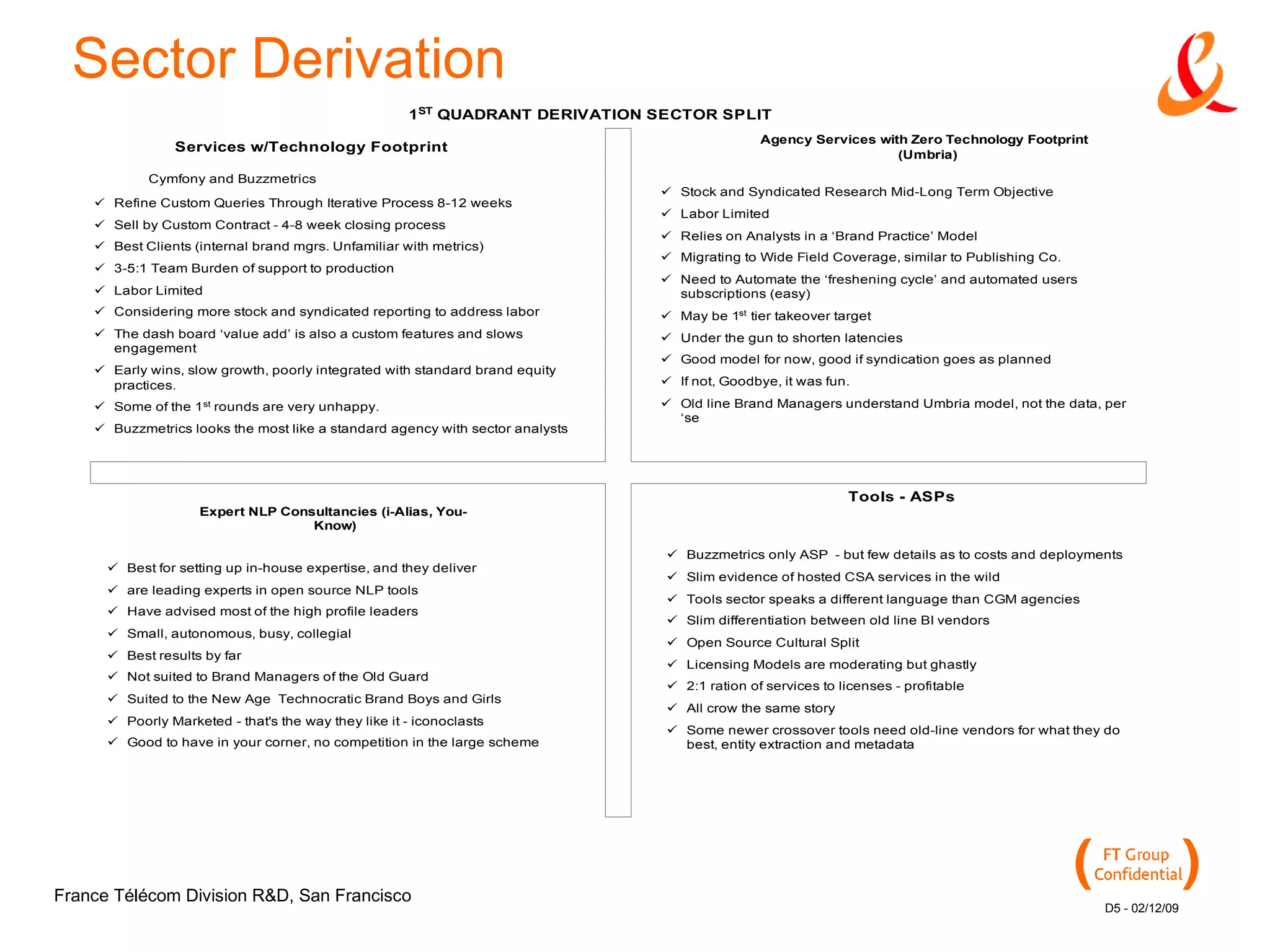

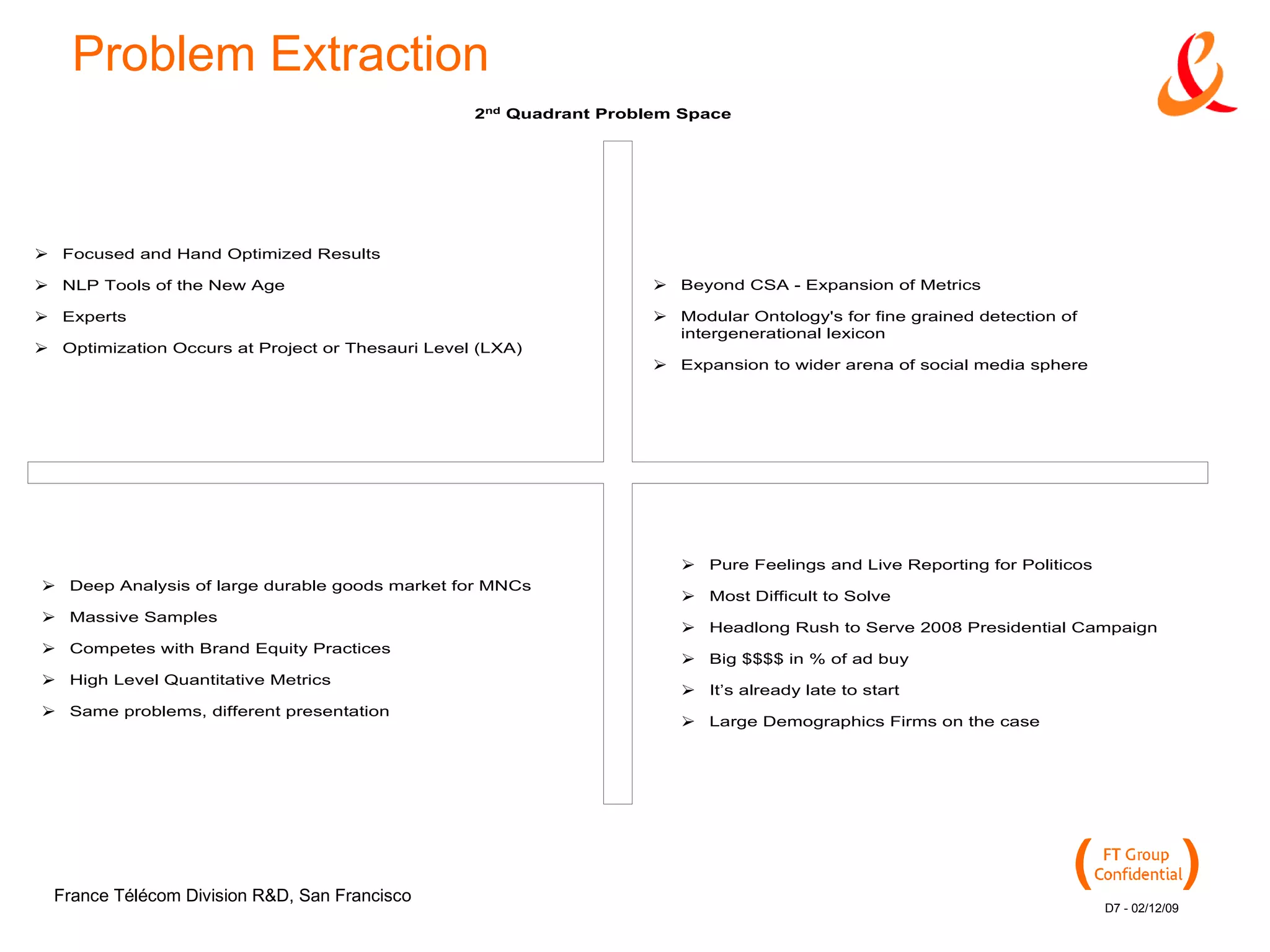

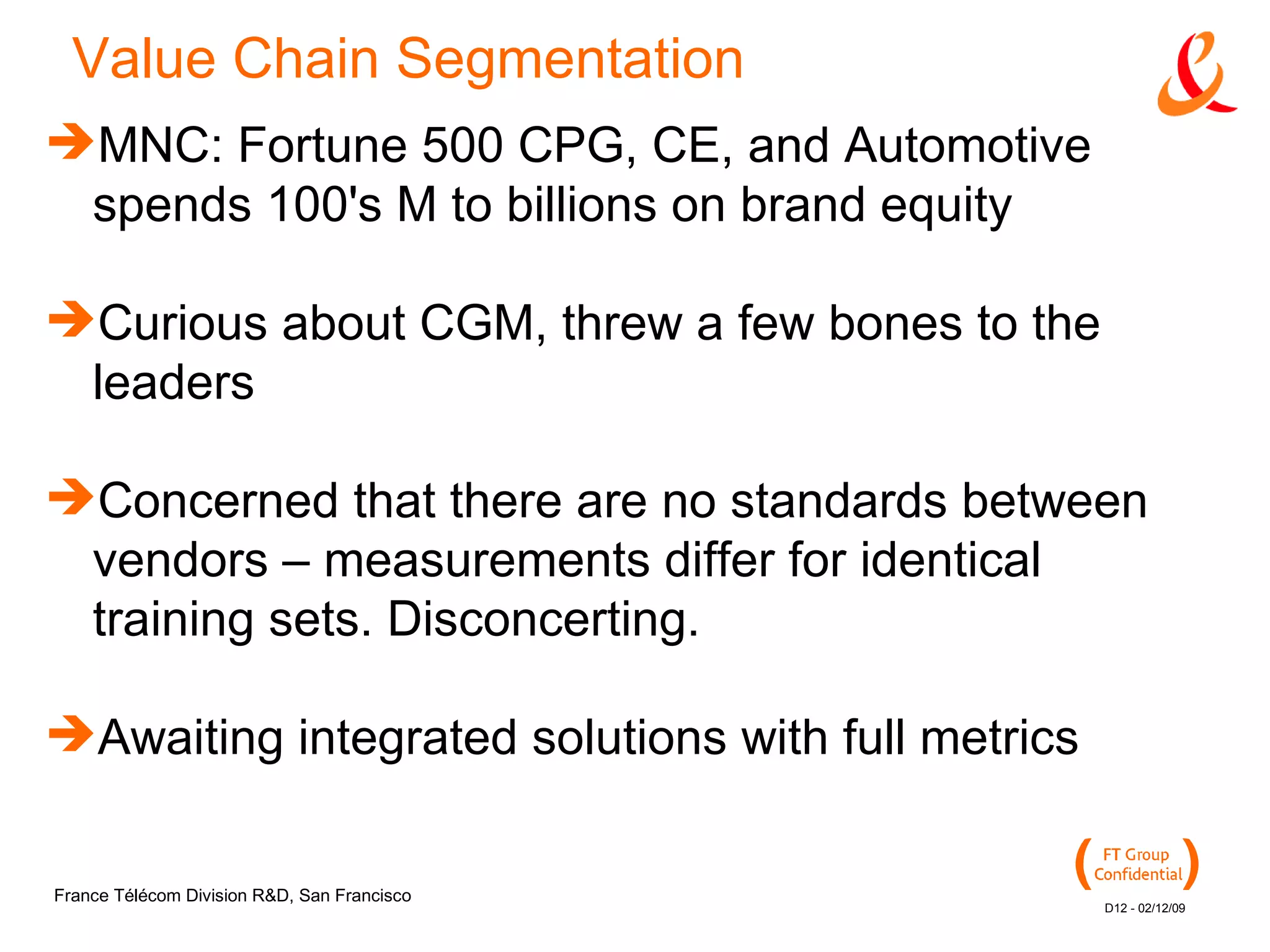

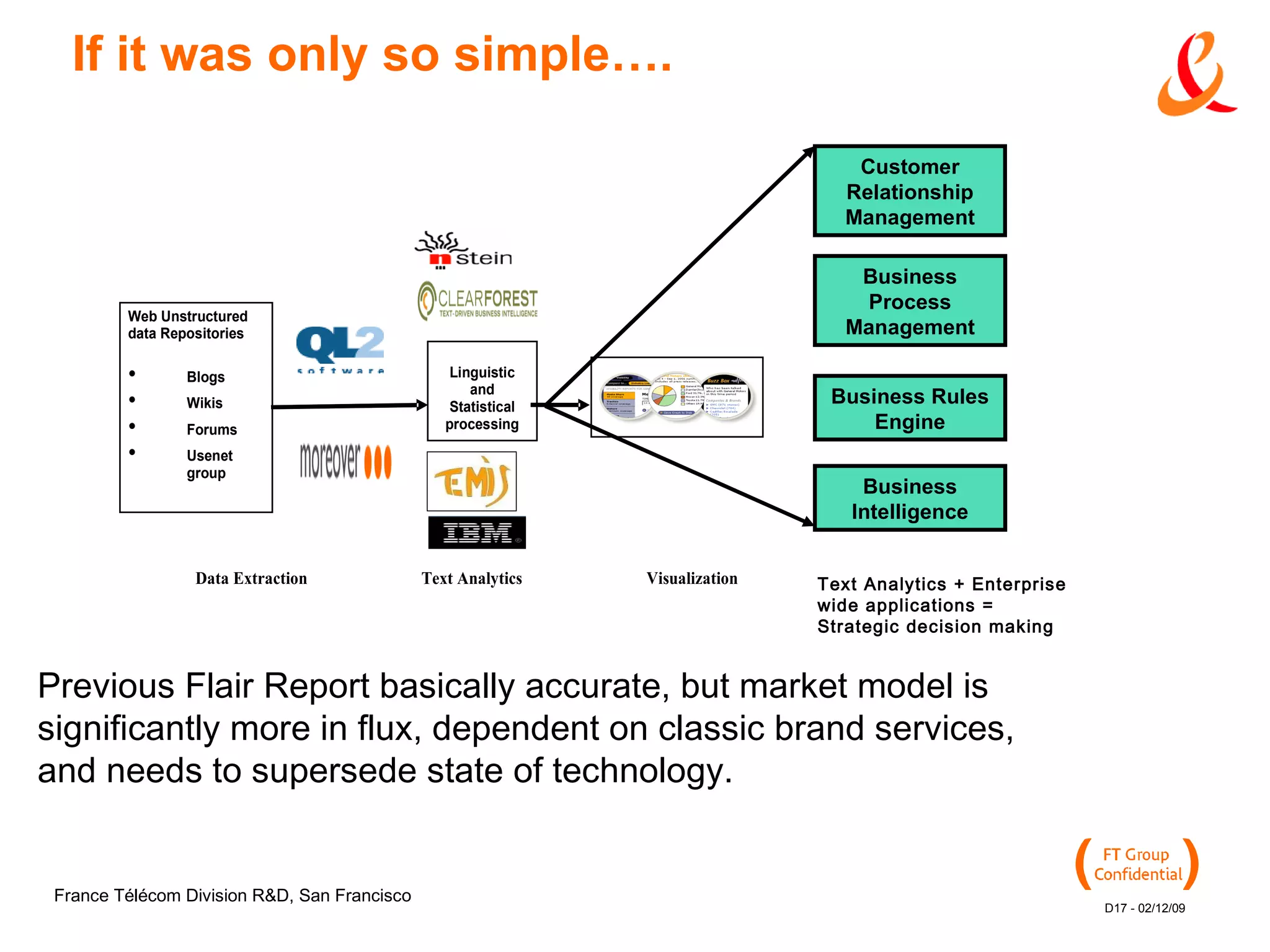

The document analyzes the integration of consumer-generated media (CGM) into brand equity consulting, highlighting the challenges faced by mid-market companies in leveraging CGM services due to their limited brand equity. It discusses the acquisition of Cymfony by TNS and the trend towards advertising analytics, emphasizing the need for actionable insights and improved standards across CGM metrics. The text advocates for a new model that connects large multinational corporations and small to medium enterprises to enhance brand intelligence through effective data utilization.

![Customer Relationship Management [CRM]](https://cdn.slidesharecdn.com/ss_thumbnails/customerrelationshipmanagementcrm-jassinghbhasin-150303100315-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)