Download to read offline

![Private & Confidential Case Study: Volatility Control Equities 19 August 2013

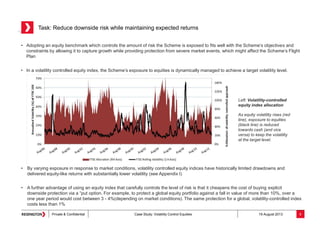

Appendix II: Implementation Structure

7

Case Study

Pension Scheme

Bank

3m Libor + X

Volatility controlled index with a 1y put option at

90% on the index

Key Terms of 1y Total Return Swap

Client pays 3m USD Libor + X

Client receives Return on [Index] – 3m LIBOR + Put option at [Strike] on the [Index]

Index

10% volatility controlled equity index (70% MSCI World Net of Dividend Tax + 30% MSCI Emerging Markets Index Net of

Dividend Tax)

Strike for Put Option 90%

Volatility Measure Maximum of exponentially Weighted Moving Average with = 3% and 6%](https://image.slidesharecdn.com/casestudyvolcontrolequities-130927092626-phpapp02/85/Case-Study-Volatility-Control-Equities-7-320.jpg)

A large UK pension scheme with a £3.5 billion deficit sought to reduce risk while maintaining returns. They implemented a volatility-controlled equity index with a put option to limit downside risk. This reduced equity risk exposure from 30% to 10% while delivering equity-like returns with lower volatility. It also lowered the cost of downside protection compared to purchasing puts directly on a passive equity index. The scheme's risk-return profile improved, allowing it to better fund its deficit over time with lower vulnerability to market stress.