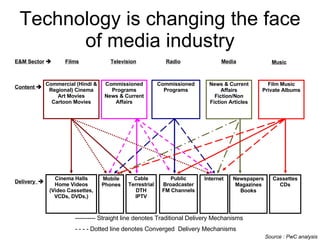

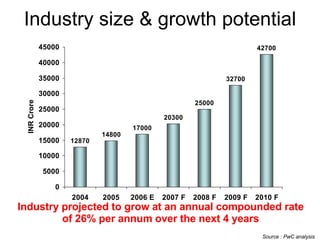

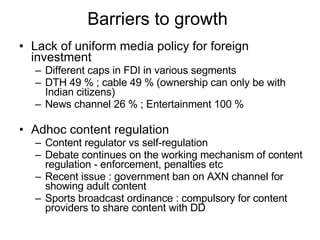

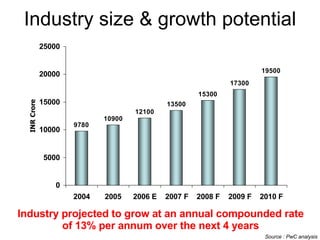

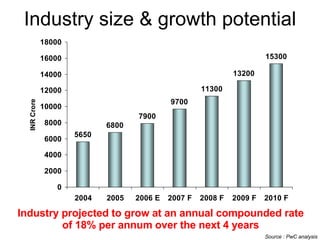

The document discusses the growth potential of the Indian media and entertainment industry across different segments like television, print, films and radio. It highlights that the industry is growing at a fast pace due to rising incomes, urbanization, and exposure to new technologies. Television is the largest segment currently and is expected to grow at 26% annually. Print and films are also growing steadily with increased literacy and multiplexes. The radio sector is opening up with new FM licenses being issued. Overall, the Indian media industry has potential to go global in the future through various strategies like targeting the NRI population, international partnerships and acquisitions of foreign media companies. However, barriers like regulations, piracy and low investments need to be addressed for realizing