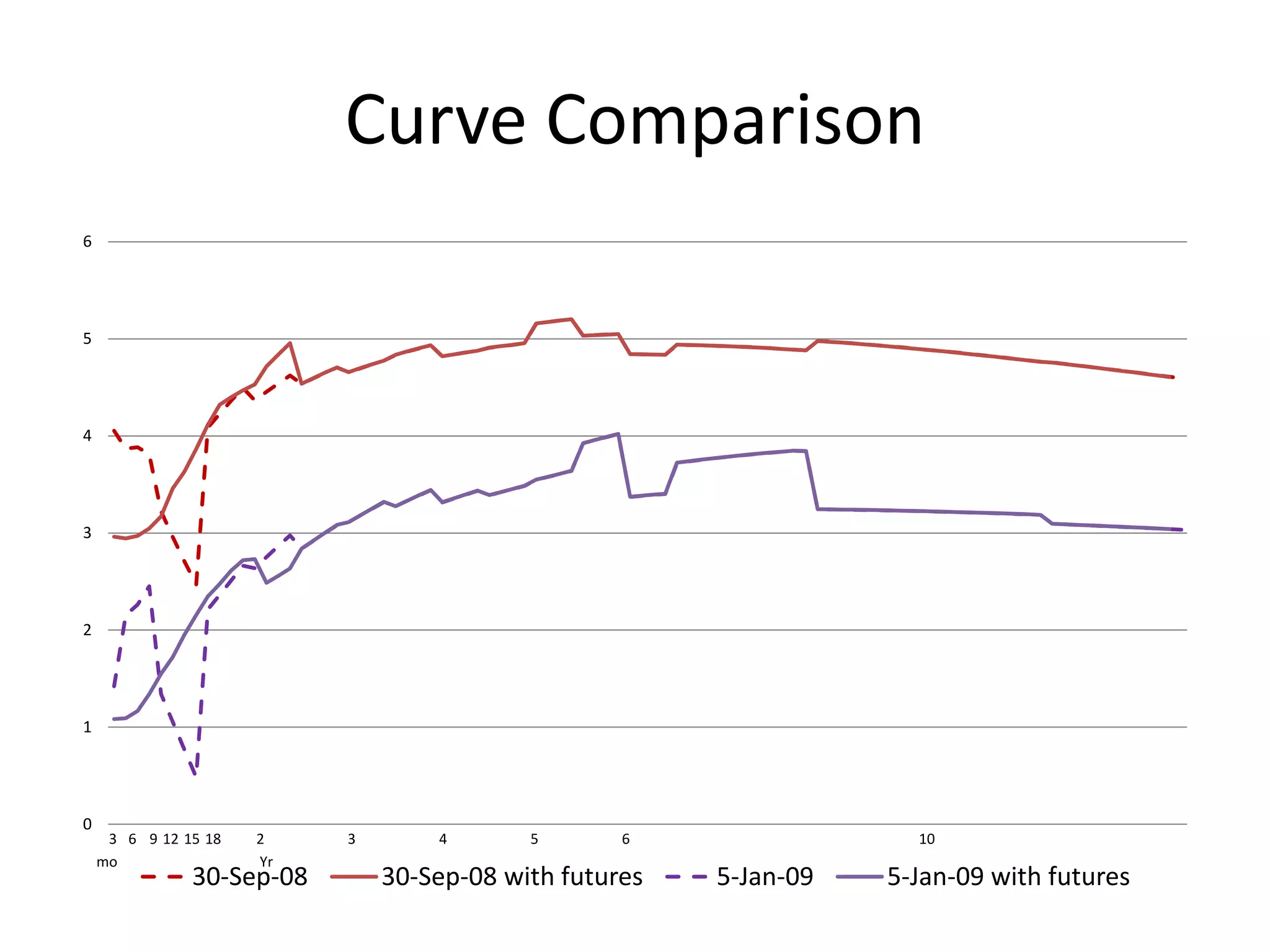

Downloaded 76 times

![Eurodollar Contract

CME Eurodollar Futures (ED) : EDA <Cmdty> CT <go>

Trade Unit Eurodollar Time Deposit have a principal

value of $1,000,000 with a three month

maturity

Point Description 1 point=.005=$12.50

Contract Listing Mar (H), Jun (M), Sep (U), Dec (Z)

Deposit Rate 100-Quote

Bloomberg Ticker EDZ0, EDH1, EDM1, EDU1 Cmdty <Go>

Contract Value 10,000*[100-.25*(100-Quote)]

Libor (%) Quote Contract Price

Sep 19, 2010 0.41 99.59 998,975

Dec 2010 0.405 99.595 998,987.5

Gain/Loss 0.005bps 12.5bps](https://image.slidesharecdn.com/buildcurvecpt-120605033106-phpapp01/75/Evolution-of-Interest-Rate-Curves-since-the-Financial-Crisis-16-2048.jpg)

![Pricing a Eurodollar Strip

PV FV * [1 r /(t / 360)] 1

A eurodollarstrip is composedof n deposit periods- each witha unique

interestrate(ri ) and term(ni ). So, we can write:

PVi FVi * [1 ri (ti / 360)] 1

PVi present va at thestart of theith deposit period

lue

FVi future value at theend of theith deposit

ri interestratefor theith deposit period

i number of thedeposit period,i 1,2,3...,

n](https://image.slidesharecdn.com/buildcurvecpt-120605033106-phpapp01/75/Evolution-of-Interest-Rate-Curves-since-the-Financial-Crisis-29-2048.jpg)

![Solving for the PV of a sequence of

investments starting from n to n-1

T hestrip is a sequence of investment : T heproceedsat theterminati of one deposit are

s on

fully and immediatel reinvestedin thenext deposit periodas a sequence.So, thepresent

y

value for a given periodis thefuture value of theprecedingperiod.FVi 1 PVi . Applying

thisequation t say, the thirddeposit period:

o,

PV3 FV3 *[1 r3 * (t3 / 360)] 1

to find thepresent va of thisdeposit,we must discount it over the

lue secondperiod:

PV2 FV2 * [1 r2 * (t 2 / 360)] 1

PV2 PV3 *[1 r2 * (t 2 / 360)] 1

or

PV2 FV3 *[1 r3 * (t3 / 360)] 1

*[1 r2 * (t 2 / 360)] 1](https://image.slidesharecdn.com/buildcurvecpt-120605033106-phpapp01/75/Evolution-of-Interest-Rate-Curves-since-the-Financial-Crisis-30-2048.jpg)

![Solving for the PV of a sequence of

investments from n to today

We arriveat thepresent va of thecash flow at thesart of the

lue

deposit period- thatis, today- by discountin it over the

g first period,

PV1 FV3 *[1 r3 * (t3 / 360)] 1

*[1 r2 * (t 2 / 360)] 1

*[1 r1 * (t3 / 360)] 1

T hequantity[1 ri * (ti / 360)] 1 is thediscount factor,dfi , for periodi

over any deposit periodsn over whichFVn is discounted T hediscount factor

.

determines in present va - at thestart of period,i of a sum paid at theend of periodi.

, lue

di [1 ri * (ti / 360)] 1](https://image.slidesharecdn.com/buildcurvecpt-120605033106-phpapp01/75/Evolution-of-Interest-Rate-Curves-since-the-Financial-Crisis-31-2048.jpg)

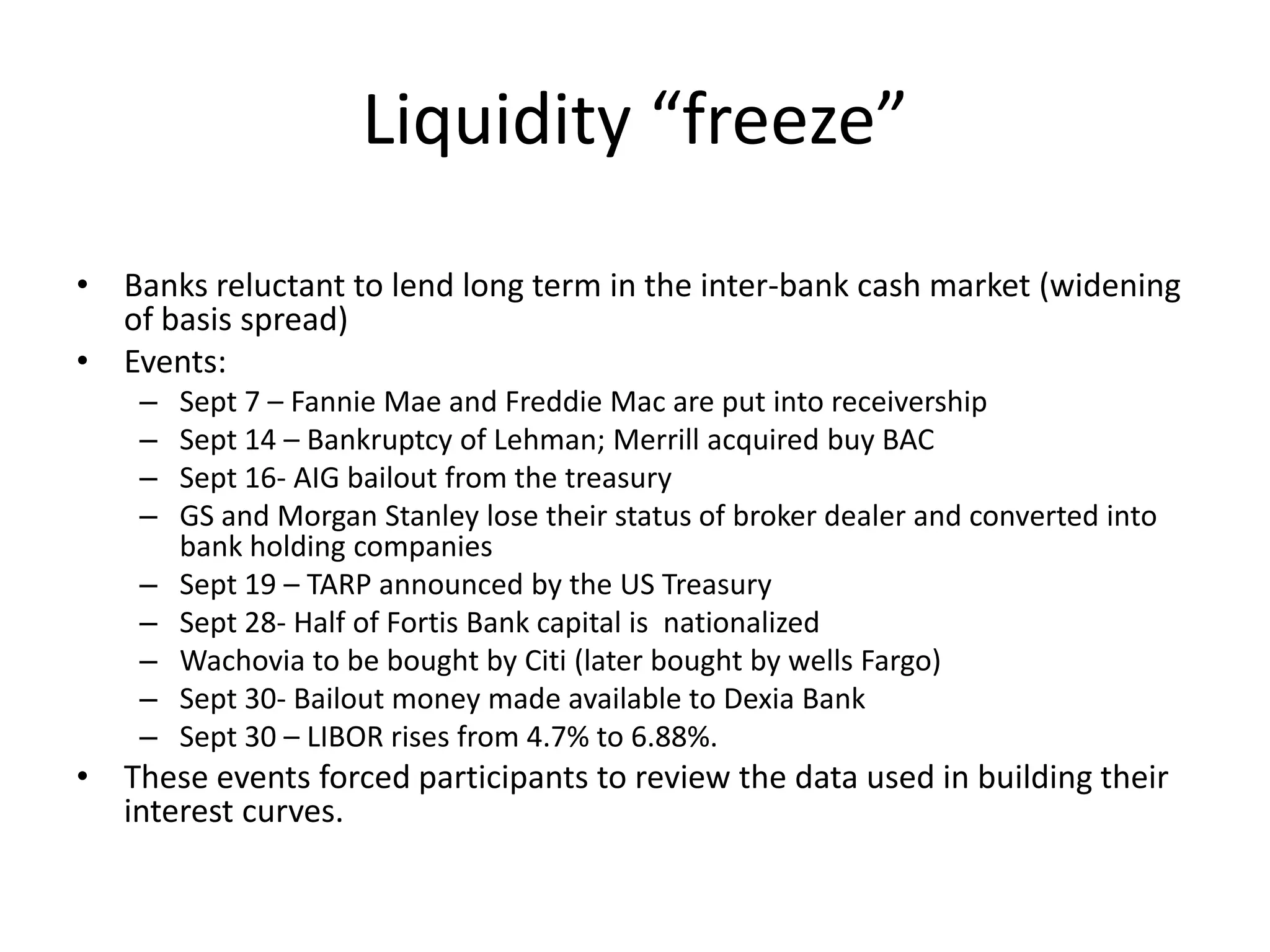

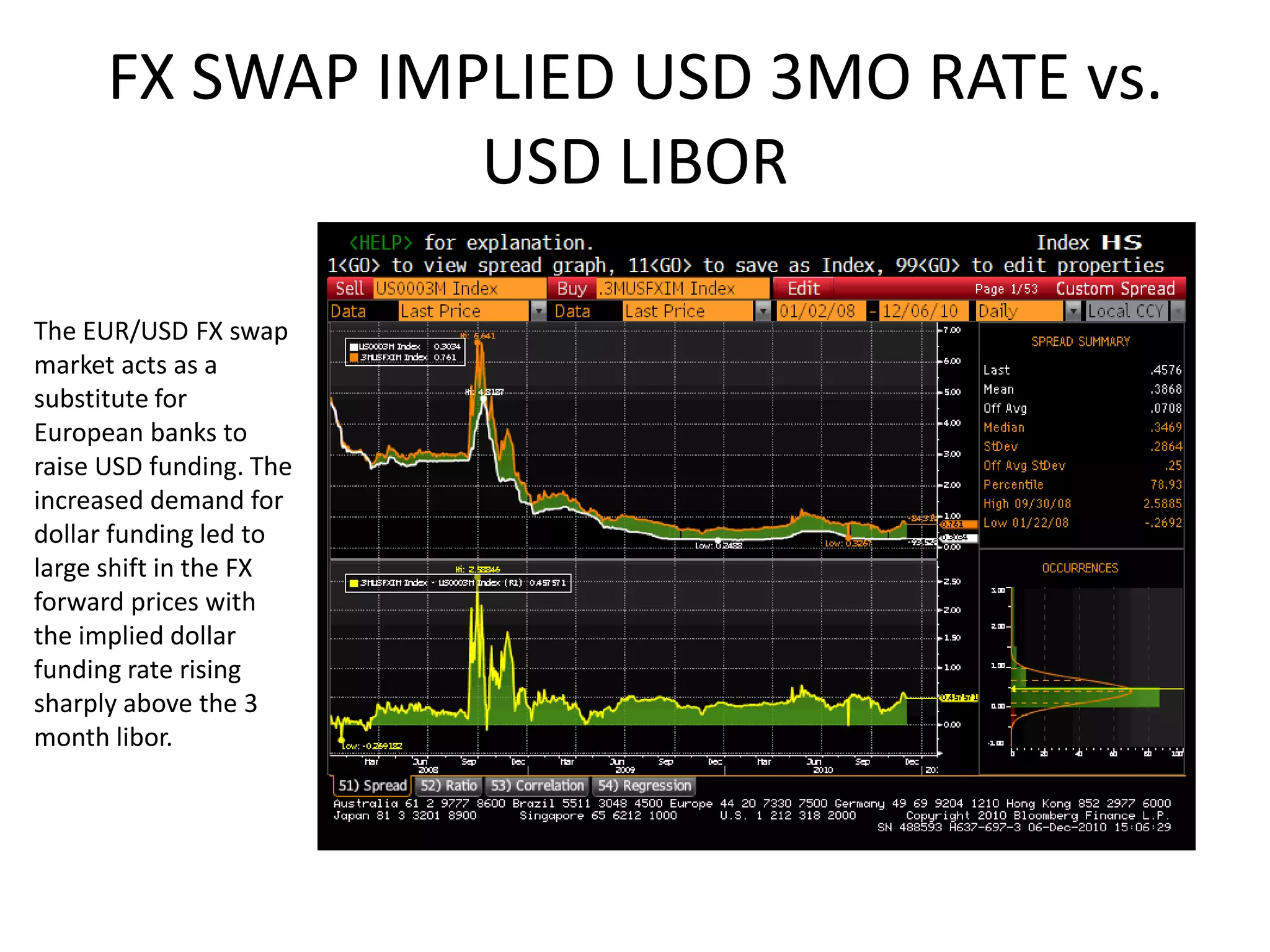

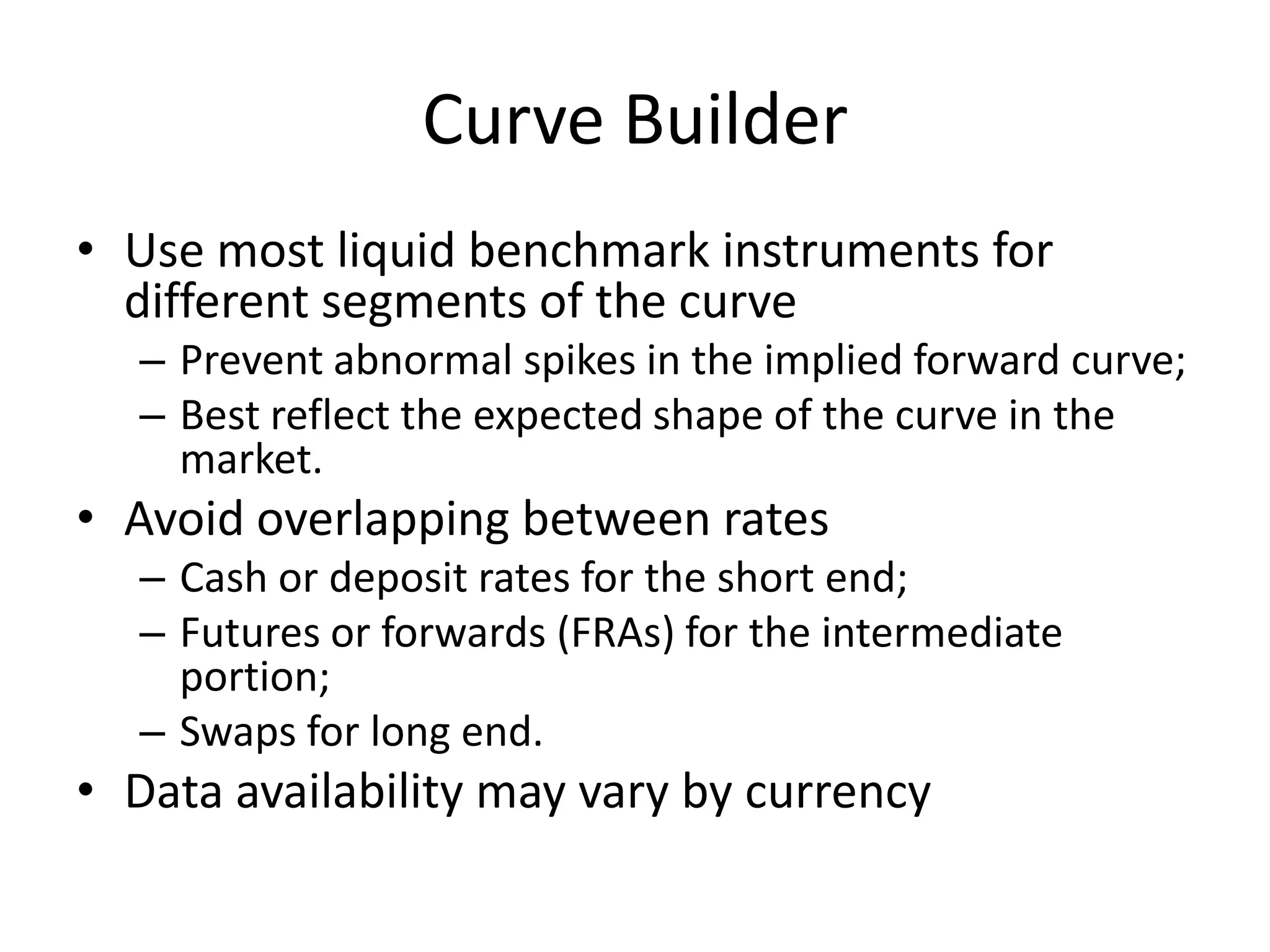

The document discusses the evolution of interest rate curves and highlights key events that impacted the financial markets, particularly during the 2007-2008 financial crisis. It details the shifts in market behaviors, such as the widening of Libor-OIS spreads, and provides insights into the methodologies of constructing interest rate curves using benchmark instruments and alternative funding sources. Additionally, it covers Eurodollar futures and the role of customization in swap curve creation through various market instruments.