2-2

1. Sales Agency(የሽያጭ ኤጀንሲ/ወኪል):

• Sales agency is a term applied to a business

unit that performs only a small portion of

the functions associated with a branch.

• A sales agency usually carries samples of

products but does not have an inventory

of merchandise and usually lesser degree of

autonomy.

10/2/2024 2

3.

2-3

2. Branch (ቅርንጫፍ):

•As a business enterprise grows, it may establish one

or more branches to market its products over a large

territory.

• The term Branch is used to describe a business unit

located at some distance from the Home Office.

• Branches are separate economic and accounting

entities from their home office.

• However, they are not separate legal entities from

their home office.

10/2/2024

3

4.

2-4

• It is100% owned by the HO.

• Branches may

carry merchandise obtained from Home Office,

make sales, approve customers’ credit, and

make collections from its customers, and

remits cash received.

• A branch may obtain merchandise solely from the

home office, or a portion may be purchased from

outside suppliers.

10/2/2024

4

5.

2-5

The cash receiptsof the branch may be deposited

in a bank account belonging to the home office.

Branch expenses are paid from an imprest cash

fund or bank account provided by home office.

As the imprested cash fund is depleted, the

branch must submit a list of cash payments

supported with vouchers in order to get

replenishment from home office.

10/2/2024

5

6.

2-6

The use ofan imprest cash fund gives the Home

Office considerable control over the cash

transactions of the branch.

However, it is common practice for a large branch

to maintain its own bank accounts.

Extent of autonomy and responsibility of a

branch varies, even among different branches of

the same business enterprise.

10/2/2024

6

7.

2-7

3. Division (ክፍል):

•Division is a business segment or a business

enterprise which generally has more autonomy

than a branch.

• Division may be organized as separate company

or may not be a separate company.

• If the division is not a separate company, the

accounting procedures are the same as Branch.

• If the division is a separate company (subsidiary

company), the financial accounting requires

consolidation, which will be discussed in later

topics. It will serve as Sister company.

10/2/2024 7

8.

2-8

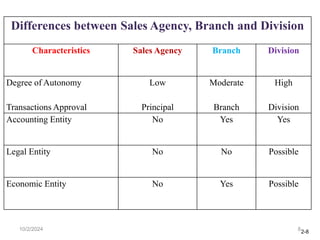

Differences between SalesAgency, Branch and Division

Characteristics Sales Agency Branch Division

Degree of Autonomy

Transactions Approval

Low

Principal

Moderate

Branch

High

Division

Accounting Entity No Yes Yes

Legal Entity No No Possible

Economic Entity No Yes Possible

10/2/2024 8

2-10

Accounting System forSales Agency

10/2/2024 10

Sales agency is sometimes applied to a business

unit that performs only a small portion of the

functions associated branch.

A sales agency usually carries samples of products

but does not have an inventory of merchandise.

Orders are taken from customers and transmitted

to the Home Office.

The Home Office approves the customers’ credit

and ships the merchandise directly to customers.

The sales agency’s receivables are maintained by

the Home Office.

11.

2-11

Accounting System forSales Agency

10/2/2024 11

The Home Office also performs collection

function.

An impressed cash fund generally is maintained at

the sales agency for the payment of operating

expenses.

A sales agency that does not carry an inventory of

merchandise, maintain receivables, or make

collections has no need for a complete set of

accounting.

12.

2-12

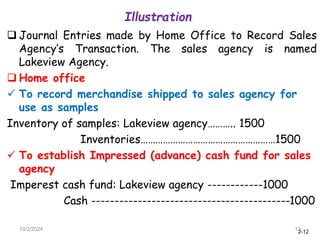

Illustration

10/2/2024 12

JournalEntries made by Home Office to Record Sales

Agency’s Transaction. The sales agency is named

Lakeview Agency.

Home office

To record merchandise shipped to sales agency for

use as samples

Inventory of samples: Lakeview agency……….. 1500

Inventories………………………………………………1500

To establish Impressed (advance) cash fund for sales

agency

Imperest cash fund: Lakeview agency ------------1000

Cash -------------------------------------------1000

13.

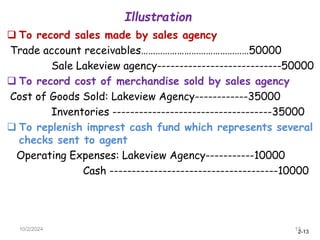

2-13

Illustration

10/2/2024 13

Torecord sales made by sales agency

Trade account receivables………………………………………50000

Sale Lakeview agency----------------------------50000

To record cost of merchandise sold by sales agency

Cost of Goods Sold: Lakeview Agency------------35000

Inventories ------------------------------------35000

To replenish imprest cash fund which represents several

checks sent to agent

Operating Expenses: Lakeview Agency-----------10000

Cash --------------------------------------10000

2-15

Start-Up Costs ofOpening New Branches

10/2/2024

15

The establishment of a branch often requires the

incurring of considerable costs before significant

revenue may be generated.

Operating losses in the first few months are likely.

Some businesses would capitalize & amortize such

start-up costs on the grounds that such costs are

necessary to successful operation at a new

location.

However, it is not allowed in IFRS.

16.

2-16

Start-Up Costs ofOpening New Branches

10/2/2024 16

In IFRS (IAS 38) start-up cost in connection with the

opening of a branch is recognized as expenses of the

accounting period in which the costs are incurred.

The decision should be based on the principle that net

income is measured by matching expired costs with

realized revenue.

Costs that benefit future accounting periods are

deferred and allocated to those periods.

17.

2-17

Accounting System fora Branch

10/2/2024 17

Two alternative systems:

1. The branch does not maintain a

complete set of accounting records.

• The home office serves only as an

accounting and control center for the

branches (Dependent branches).

18.

2-18

Accounting System fora Branch

10/2/2024 18

2. The branch maintains a complete set of

accounting records (Independent branches)

• Branch maintains its own journal entries, ledger

and chart of accounts similar to those of an

independent business enterprise.

• Financial statements are prepared by the branch

accountant and forwarded to the home office.

• The number and types of ledger accounts, the

internal control structure, the form and content of

the financial statements, and the accounting policies

generally are prescribed by the Home Office.

19.

2-19

Accounting System fora Branch

10/2/2024 19

This chapter focuses on the second system that the

branch maintains its own accounting records.

Transactions recorded by a branch should include all

controllable expenses and revenue for which the

branch manager is responsible.

20.

2-20

Accounting System fora Branch

10/2/2024 20

• If the branch manager has responsibility over all

branch assets, liabilities, revenue, and expenses, the

branch accounting records should reflect this

responsibility.

• Expenses such as depreciation often are not subject to

control by a branch manager; therefore both the

branch plant assets and the related depreciation

ledger accounts generally are maintained by the Home

Office.

21.

2-21

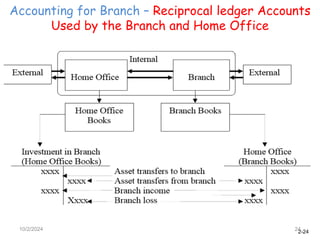

Accounting for Branch– Reciprocal (intra company)

ledger Accounts Used by the Branch and Home

Office

10/2/2024 21

The accounting records maintained by a branch

include a Home Office ledger account*

• H.O reflects all activity b/n the branch and

home office

– It is Cr. for all merchandise, cash or other

assets provided by the home office;

– H.O is Dr. for all cash, merchandise, or other

assets sent by the branch to the home office or

the other branches.

22.

2-22

Accounting for Branch– Reciprocal ledger Accounts

Used by the Branch and Home Office

10/2/2024 22

• H.O ledger account is a quasi-ownership equity

account represents the net investment by the home

office in the branch.

• At the end of an accounting period when the branch

closes its accounting records, the I/Summary account

is closed to the H.O account.

• A net income increases the credit balance of the

Home Office account; a net loss decreases (debit) this

balance.

23.

2-23

Accounting for Branch– Reciprocal ledger Accounts

Used by the Branch and Home Office

10/2/2024 23

In the home office accounting records, a reciprocal ledger

account with a title such as Investment in Branch is

maintained.

• It is non-current asset account

– Dr. for cash merchandise, and services provided to the

branch, and for the NI reported by the branch.

– Cr. for the cash or other assets received from the

branch, and for net losses reported by the branch.

Thus the Investment in Branch account reflects the equity

method of accounting.

A separate investment account generally is maintained by

the H.O for each branch.

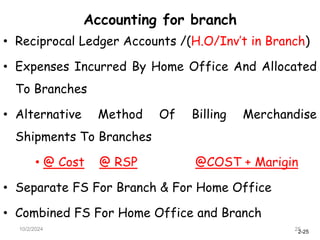

2-25

Accounting for branch

10/2/202425

• Reciprocal Ledger Accounts /(H.O/Inv’t in Branch)

• Expenses Incurred By Home Office And Allocated

To Branches

• Alternative Method Of Billing Merchandise

Shipments To Branches

• @ Cost @ RSP @COST + Marigin

• Separate FS For Branch & For Home Office

• Combined FS For Home Office and Branch

26.

2-26

Acquisition of PlantAssets Used in Branch

10/2/2024 26

• Some business enterprises follow a policy of

notifying each branch of expenses incurred

by the Home Office on the branch’s behalf.

• Plant assets located at a branch generally

are carried in the Home Office accounting

records.

27.

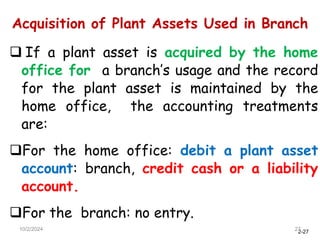

2-27

Acquisition of PlantAssets Used in Branch

10/2/2024 27

If a plant asset is acquired by the home

office for a branch’s usage and the record

for the plant asset is maintained by the

home office, the accounting treatments

are:

For the home office: debit a plant asset

account: branch, credit cash or a liability

account.

For the branch: no entry.

28.

2-28

Acquisition of PlantAssets Used in Branch

10/2/2024 28

If a plant asset is acquired by a branch,

but the accounting record for this plant

asset is maintained by the home office, the

accounting treatments are:

For the branch: debit Home Office and

credit cash or a liability account.

For the home office: debit a plant asset

account: branch, and credit Investment in

Branch account.

29.

2-29

Expense Incurred byHome Office and Allocated to

Branches

10/2/2024 29

The home office may pay some taxes, insurance or

advertising on behalf of branches or for the

benefits of all branches.

These expenses include depreciation expense for

the plant assets purchased by home office but

used by branches.

These expenses are usually allocated to branches

in determining net income of branches.

30.

2-30

Expense Incurred byHome Office and Allocated to

Branches

10/2/2024 30

If the home office chooses to allocate these expenses to

branches, the accounting treatments are:

a. For the home office: debit Investment in Branch account,

credit an appropriate expense account.

b. For the branch: debit expense account, credit Home Office

account.

If the H.O does not make sales and serves only as

accounting center then most or all of its expenses may be

allocated to branches

31.

2-31

Expense Incurred byHome Office and Allocated to

Branches

10/2/2024 31

• H.O may charge each branch interest on the capital

invested in that branch.

• Interest expense recognized by the branches would

be offset by interest revenue recognized by the

H.O.

• Amounts would be netted and would not be

displayed in the combined income statement.

32.

2-32

Alternative Methods ofBilling Merchandise

Shipments to Branches

Three alternative methods are available to the Home

Office for billing merchandise shipped to its branches.

The shipments may be billed:

1. At Home Office cost,

2. At a percentage above Home Office cost, or

3. At the branch’s retail selling price

Shipment of merchandise to a branch does not

constitute a sale b/c ownership title has not changed.

10/2/2024 32

33.

2-33

Billing shipments toa branch at Home

Office cost

Strength: this is the simplest procedure and is

widely used. It avoids the complication of

unrealized gross profit in inventories and permits

the financial statements of branches to give a

meaningful picture of operations.

Weakness: billing merchandise to branches at

Home Office cost attributes all gross profits of

the enterprise to the branches,

Under these circumstances, Home Office cost may

be the most realistic basis for billing shipment to

branches.

10/2/2024 33

34.

2-34

Billing shipments ata percentage above Home

Office cost or at mark up (such as 110% of cost)

Strength: this may be intended to allocate a

reasonable gross profit to the Home Office.

Weakness: when merchandise is billed to a branch

at a price above Home Office cost:

the net income reported by the branch is

understated and;

the ending inventories are over-stated for the

enterprise as a whole.

10/2/2024 34

35.

2-35

• Thus, adjustmentsmust be made by the

Home Office to eliminate the excess of

billed prices over cost (intracompany profits)

in the preparation of combined financial

statements for the Home Office and the

branch.

10/2/2024 35

36.

2-36

Billing shipments toa branch at branch

retail selling prices

• Strength: this may be based on a desire to strengthen

internal control over inventories.

• If the physical inventories taken periodically at the branch

do not agree with the amounts thus computed, an error or

theft may be indicated and should be investigated promptly.

• Weakness: no gross profit assigned to the branches and the

branch’s net loss will equal its operating expenses.

10/2/2024 36

37.

2-37

Separate Financial Statementsfor Branch and for

Home Office ( for internal use only)

• A separate income statement and balance sheet

should be prepared for a branch so management

of the enterprise may review the operating

results and financial position of the branch.

• However, it is important to emphasize that

separate financial statements of the Home

Office and of the branch are prepared for

internal use only; they do not meet the needs of

investors or other external users of financial

statements.

10/2/2024 37

38.

2-38

Separate Financial Statementsfor Branch and for

Home Office ( for internal use only)

• Separate financial statement doesn't serve

external users

• However, to prepare financial statements

for external users , branches financial

statement should be revised to eliminate

any intercompany profits on merchandise

shipments.

10/2/2024 38

39.

2-39

Separate Financial Statementsfor Branch and for

Home Office ( for internal use only)

• The branch statements of financial position will

have H.O Ledger Account instead of Ownership

Equity Account.

• The separate F/st. prepared by branch will be

revised by H.O to include expenses incurred by

the H.O for branch & to show the results of

branch operations after elimination of any intra-

co. profits on merchandise shipments.

• Separate FS also may be prepared for the H.O,

so that the results of its operations and its

financial position can be appraised.

10/2/2024 39

40.

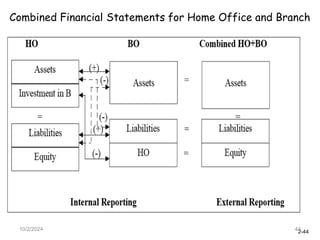

2-40

Combined financial Statementsfor Home Office

and Branch (for external use)

• For investors, the home office and

branches are a single business entity.

• Thus, combined financial statements

should be prepared for external users.

• A four-column work sheet paper is used

to facilitate the preparation of the

combined financial statement.

10/2/2024 40

41.

2-41

Combined financial Statementsfor Home Office

and Branch (for external use)

In preparing the combined financial statements,

the following accounts should be eliminated:

a. Reciprocal ledger accounts

b. Any intra company profits or losses.

c. Any receivables and payables between the

home office and the branch (or between two

branches).

• The rest of accounts are just summed together

for the combined financial statements.

10/2/2024 41

42.

2-42

Combined Financial Statementsfor Home Office

and Branch

• A balance sheet for distribution to

creditors, stockholders, and government

agencies must show the financial position of

a business enterprise having branches as a

single entity.

• A convenient starting point in the

preparation of a combined balance sheet

consists of the adjusted trial balances of

the Home Office and the Branch.

10/2/2024 42

43.

2-43

• Similar accountsare combined to produce a single

total amount for cash, trade accounts receivable,

and other assets and liabilities of the enterprise as

a whole.

• In the preparation of a combined balance sheet,

reciprocal ledger accounts are eliminated because

they have no significance when the branch and

Home Office report as a single entity.

10/2/2024 43

2-45

10/2/2024 45

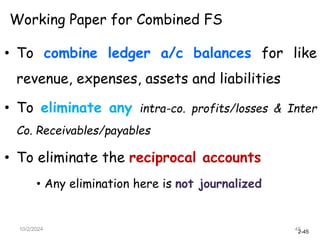

Working Paperfor Combined FS

• To combine ledger a/c balances for like

revenue, expenses, assets and liabilities

• To eliminate any intra-co. profits/losses & Inter

Co. Receivables/payables

• To eliminate the reciprocal accounts

• Any elimination here is not journalized

46.

2-46

10/2/2024 46

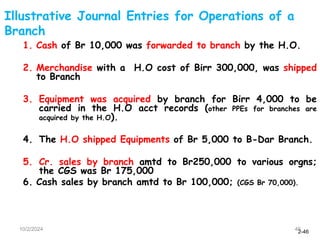

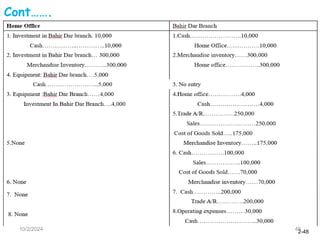

1. Cashof Br 10,000 was forwarded to branch by the H.O.

2. Merchandise with a H.O cost of Birr 300,000, was shipped

to Branch

3. Equipment was acquired by branch for Birr 4,000 to be

carried in the H.O acct records (other PPEs for branches are

acquired by the H.O).

4. The H.O shipped Equipments of Br 5,000 to B-Dar Branch.

5. Cr. sales by branch amtd to Br250,000 to various orgns;

the CGS was Br 175,000

6. Cash sales by branch amtd to Br 100,000; (CGS Br 70,000).

Illustrative Journal Entries for Operations of a

Branch

47.

2-47

10/2/2024 47

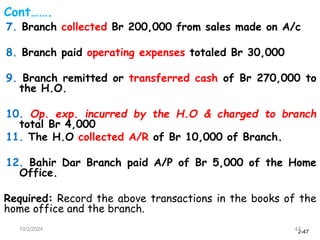

Cont…….

7. Branchcollected Br 200,000 from sales made on A/c

8. Branch paid operating expenses totaled Br 30,000

9. Branch remitted or transferred cash of Br 270,000 to

the H.O.

10. Op. exp. incurred by the H.O & charged to branch

total Br 4,000

11. The H.O collected A/R of Br 10,000 of Branch.

12. Bahir Dar Branch paid A/P of Br 5,000 of the Home

Office.

Required: Record the above transactions in the books of the

home office and the branch.

2-50

10/2/2024 50

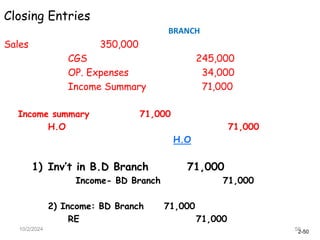

Closing Entries

BRANCH

Sales350,000

CGS 245,000

OP. Expenses 34,000

Income Summary 71,000

Income summary 71,000

H.O 71,000

H.O

1) Inv’t in B.D Branch 71,000

Income- BD Branch 71,000

2) Income: BD Branch 71,000

RE 71,000

51.

2-51

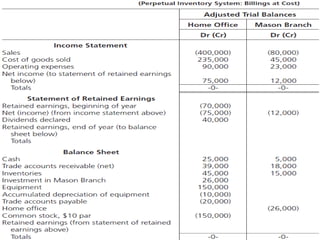

• Assume thatSmaldino Company bills merchandise to

Mason Branch at home office cost.

• That Mason Branch maintains complete accounting

records and prepares financial statements.

• Both the home office and the branch use the perpetual

inventory system.

• Equipment used at the branch is carried in the home

office accounting records.

• Expenses, such as advertising and insurance, incurred

by the home office on behalf of the branch, are

allocated to the branch.

• Transactions and events during the first year (2005) of

operations of Mason Branch are summarized below

(start-up costs are disregarded):

10/2/2024 51

Example 2 on Branch Operation

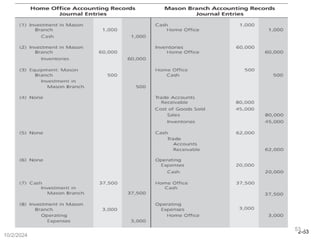

52.

2-52

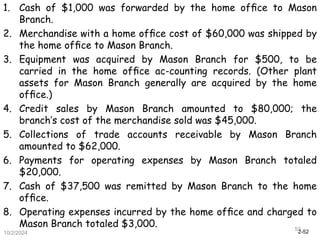

1. Cash of$1,000 was forwarded by the home office to Mason

Branch.

2. Merchandise with a home office cost of $60,000 was shipped by

the home office to Mason Branch.

3. Equipment was acquired by Mason Branch for $500, to be

carried in the home office ac-counting records. (Other plant

assets for Mason Branch generally are acquired by the home

office.)

4. Credit sales by Mason Branch amounted to $80,000; the

branch’s cost of the merchandise sold was $45,000.

5. Collections of trade accounts receivable by Mason Branch

amounted to $62,000.

6. Payments for operating expenses by Mason Branch totaled

$20,000.

7. Cash of $37,500 was remitted by Mason Branch to the home

office.

8. Operating expenses incurred by the home office and charged to

Mason Branch totaled $3,000.

10/2/2024

52

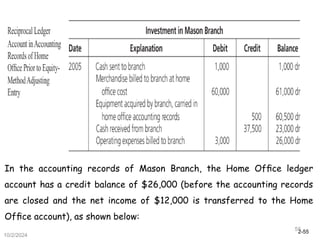

2-54

10/2/2024

54

If abranch obtains merchandise from outsiders as well as

from the home office, the merchandise acquired from the

home office may be recorded in a separate Inventories

from Home Office ledger account.

In the home office accounting records, the Investment in

Mason Branch ledger account has a debit balance of

$26,000 [before the accounting records are closed and the

branch net income of $12,000 ($80,000 - $45,000 -

$20,000 - $3,000 = $12,000) is transferred to the

Investment in Mason Branch ledger account], as illustrated

on the next slide.

55.

2-55

10/2/2024

55

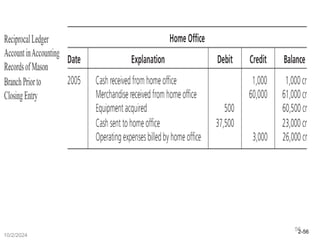

In the accountingrecords of Mason Branch, the Home Office ledger

account has a credit balance of $26,000 (before the accounting records

are closed and the net income of $12,000 is transferred to the Home

Office account), as shown below:

2-57

10/2/2024

57

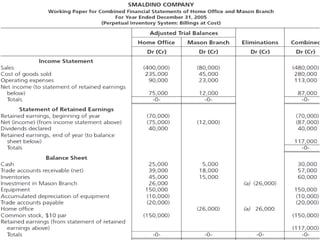

• A workingpaper for combined financial statements

has three purposes: (1) to combine ledger account

balances for like revenue, expenses, assets, and

liabilities, (2) to eliminate any intra company profits

or losses, and (3) to eliminate the reciprocal accounts.

• Assume that the perpetual inventories of $15,000

($60,000 - $45,000 = $15,000) at the end of 2005

for Mason Branch had been verified by a physical

count.

Working Paper for Combined Financial Statements

58.

2-58

10/2/2024

58

• Note thatthe $26,000 debit balance of the Investment in

Mason Branch ledger account and the $26,000 credit

balance of the Home Office account are the balances

before the respective accounting records are closed, that

is, before the $12,000 net income of Mason Branch is

entered in these two reciprocal accounts.

• In the Eliminations column, elimination (a) offsets the

balance of the Investment in Mason Branch account

against the balance of the Home Office account.

• This elimination appears in the working paper only; it is

not entered in the accounting records of either the home

office or Mason Branch because its only purpose is to

facilitate the preparation of combined financial

statements.

• The following working paper provides the information for

the combined financial statements of Smaldino Company.

2-63

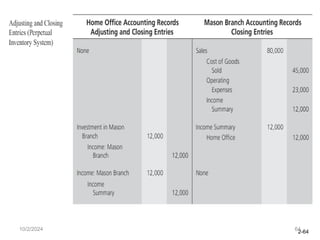

10/2/2024 63

Home OfficeAdjusting and Closing Entries and Branch

Closing Entries

• The home office’s equity-method adjusting and

closing entries for branch operating results and

the branch’s closing entries on December 31,

2005, are as follows:

2-65

10/2/2024 65

• Asstated previously, the home offices of some

business enterprises bill merchandise shipped to

branches at home office cost plus a markup percentage

(or alternatively at branch retail selling prices).

• Because both these methods involve similar

modifications of accounting procedures, a single

example illustrates the key points involved, using the

illustration for Smaldino Company above and with one

changed assumption: the home office bills merchandise

shipped to Mason Branch at a markup of 50% above

home office cost, or 33 1/3% of billed price.

Billing of Merchandise to Branches at Prices

above Home Office Cost

66.

2-66

10/2/2024 66

• Underthis assumption, the journal entries for the

first year’s events and transactions by the home office

and Mason Branch are the same as those presented

above, except for the journal entries for shipments of

merchandise from the home office to Mason Branch.

• These shipments ($60,000 cost + 50% markup on cost

= $90,000) are recorded under the perpetual inventory

system as follows:

Billing of Merchandise to Branches at Prices

above Home Office Cost

67.

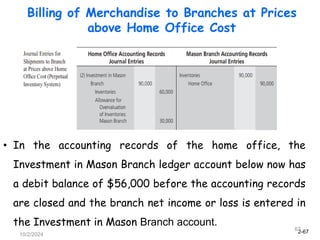

2-67

10/2/2024

67

Billing of Merchandiseto Branches at Prices

above Home Office Cost

• In the accounting records of the home office, the

Investment in Mason Branch ledger account below now has

a debit balance of $56,000 before the accounting records

are closed and the branch net income or loss is entered in

the Investment in Mason Branch account.

68.

2-68

10/2/2024

68

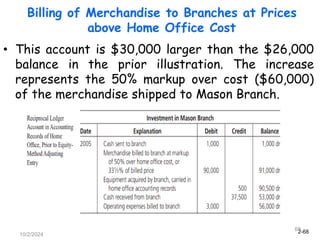

Billing of Merchandiseto Branches at Prices

above Home Office Cost

• This account is $30,000 larger than the $26,000

balance in the prior illustration. The increase

represents the 50% markup over cost ($60,000)

of the merchandise shipped to Mason Branch.

69.

2-69

10/2/2024

69

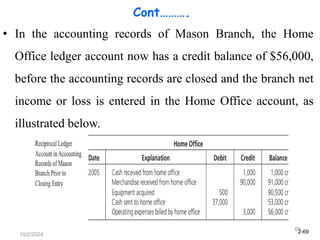

Cont……….

• In theaccounting records of Mason Branch, the Home

Office ledger account now has a credit balance of $56,000,

before the accounting records are closed and the branch net

income or loss is entered in the Home Office account, as

illustrated below.

70.

2-70

10/2/2024

70

Cont………..

• Mason Branchrecorded the merchandise received from the home

office at billed prices of $90,000; the home office recorded the

shipment by credits of $60,000 to Inventories and $30,000 to

Allowance for Overvaluation of Inventories: Mason Branch.

• Use of the allowance account enables the home office to maintain a

record of the cost of merchandise shipped to Mason Branch as well as

the amount of the unrealized gross profit on the shipments.

• At the end of the accounting period, Mason Branch reports its

inventories (at billed prices) at $22,500. The cost of these inventories

is $15,000 ($22,500/1.50 = $15,000).

• In the home office accounting records, the required balance of the

Allowance for Overval uation of Inventories: Mason Branch ledger

account is $7,500 ($22,500 $15,000 $7,500); thus, this account

balance must be reduced from its present amount of $30,000 to

$7,500.

71.

2-71

10/2/2024

71

Cont………..

• The reasonfor this reduction is that the 50% markup of billed

prices over cost has become realized gross profit to the home

office with respect to the merchandise sold by the branch.

• Consequently, at the end of the year the home office reduces its

allowance for overvaluation of the branch inventories to the

$7,500 excess valuation contained in the ending inventories.

• The debit adjustment of $22,500 in the allowance account is

offset by a credit to the Realized Gross Profit: Mason Branch

Sales account, because it represents additional gross profit of

the home office resulting from sales by the branch.

• These matters are illustrated in the home office end-of-period

adjusting and closing entries below.

72.

2-72

10/2/2024

72

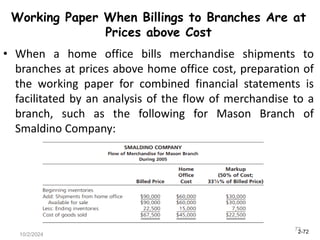

Working Paper WhenBillings to Branches Are at

Prices above Cost

• When a home office bills merchandise shipments to

branches at prices above home office cost, preparation of

the working paper for combined financial statements is

facilitated by an analysis of the flow of merchandise to a

branch, such as the following for Mason Branch of

Smaldino Company:

73.

2-73

10/2/2024

73

Cont……….

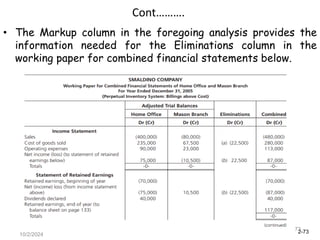

• The Markupcolumn in the foregoing analysis provides the

information needed for the Eliminations column in the

working paper for combined financial statements below.

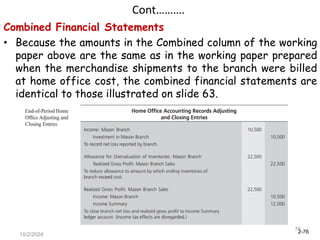

2-75

10/2/2024

75

Cont……….

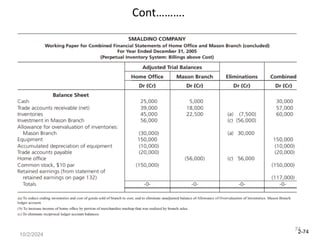

• The foregoingworking paper differs from the

working paper on slide 60 by the inclusion of an

elimination to restate the ending inventories of the

branch to cost. Also, the income reported by the

home office is adjusted by the $22,500 of

merchandise markup that was realized as a result

of sales by the branch.

• As stated on slide 58, the amounts in the

Eliminations column appear only in the working

paper. The amounts represent a mechanical step to

aid in the preparation of combined financial

statements and are not entered in the accounting

records of either the home office or the branch.

76.

2-76

10/2/2024

76

Cont……….

Combined Financial Statements

•Because the amounts in the Combined column of the working

paper above are the same as in the working paper prepared

when the merchandise shipments to the branch were billed

at home office cost, the combined financial statements are

identical to those illustrated on slide 63.

77.

2-77

10/2/2024

77

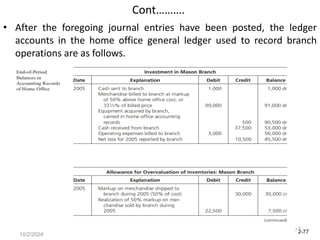

Cont……….

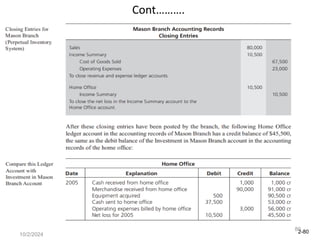

• After theforegoing journal entries have been posted, the ledger

accounts in the home office general ledger used to record branch

operations are as follows.

2-79

10/2/2024

79

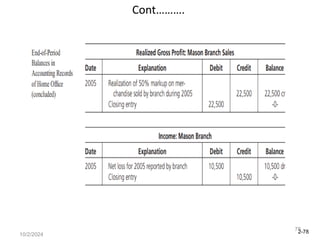

Cont……….

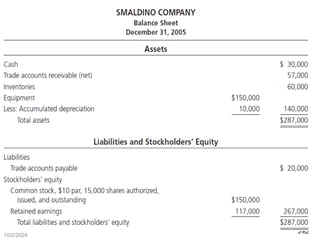

• In theseparate balance sheet for the home office, the $7,500

credit balance of the Allowance of Overvaluation of

Inventories: Mason Branch ledger account is deducted from

the $45,500 debit balance of the Investment in Mason

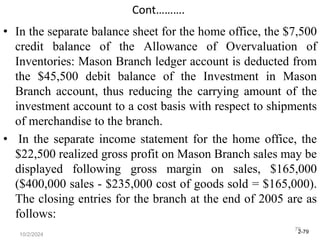

Branch account, thus reducing the carrying amount of the

investment account to a cost basis with respect to shipments

of merchandise to the branch.

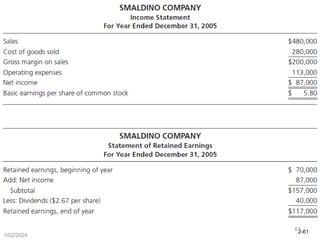

• In the separate income statement for the home office, the

$22,500 realized gross profit on Mason Branch sales may be

displayed following gross margin on sales, $165,000

($400,000 sales - $235,000 cost of goods sold = $165,000).

The closing entries for the branch at the end of 2005 are as

follows:

2-81

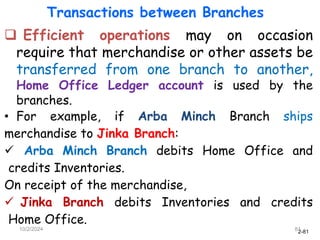

Transactions between Branches

Efficient operations may on occasion

require that merchandise or other assets be

transferred from one branch to another,

Home Office Ledger account is used by the

branches.

• For example, if Arba Minch Branch ships

merchandise to Jinka Branch:

Arba Minch Branch debits Home Office and

credits Inventories.

On receipt of the merchandise,

Jinka Branch debits Inventories and credits

Home Office.

10/2/2024 81

82.

2-82

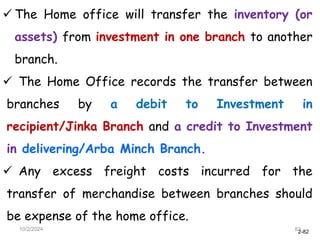

The Homeoffice will transfer the inventory (or

assets) from investment in one branch to another

branch.

The Home Office records the transfer between

branches by a debit to Investment in

recipient/Jinka Branch and a credit to Investment

in delivering/Arba Minch Branch.

Any excess freight costs incurred for the

transfer of merchandise between branches should

be expense of the home office.

10/2/2024 82

83.

2-83

Illustration: Excess freightcosts on inter-branch

transfers of merchandise.

The Home office in Addis Ababa shipped merchandise

costing Birr 8,000 to Arba Minch Branch and paid freight

costs of Birr 500.

A week later, the Home office instructed Arba Minch

Branch to transfer this merchandise to Jinka Branch.

Freight costs of Birr 400 were paid by Arba

Minch branch to carry out this order.

10/2/2024 83

84.

2-84

If themerchandise had been shipped directly

from the home office to Jinka, the freight costs

would have been Birr 600.

Assume that the H.O & its branches use perpetual

inventory system.

Make all the necessary journal entries in the

accounting records of Home office, AM Branch

and Jinka Branch.

10/2/2024 84

85.

2-85

Home Office

Investment inArba Minch Branch 8,500

Inventories 8,000

Cash 500

To record shipment and payment of freight costs

Investment in Jinka Branch 8,600

Excess Freight Expense* 300

Investment in Arba Minch Branch 8,900

To record transfer of merchandise from AM to JK

under instruction of the Home Office.

10/2/2024 85

86.

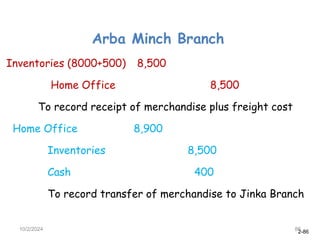

2-86

Arba Minch Branch

Inventories(8000+500) 8,500

Home Office 8,500

To record receipt of merchandise plus freight cost

Home Office 8,900

Inventories 8,500

Cash 400

To record transfer of merchandise to Jinka Branch

10/2/2024 86

![2-54

10/2/2024

54

If a branch obtains merchandise from outsiders as well as

from the home office, the merchandise acquired from the

home office may be recorded in a separate Inventories

from Home Office ledger account.

In the home office accounting records, the Investment in

Mason Branch ledger account has a debit balance of

$26,000 [before the accounting records are closed and the

branch net income of $12,000 ($80,000 - $45,000 -

$20,000 - $3,000 = $12,000) is transferred to the

Investment in Mason Branch ledger account], as illustrated

on the next slide.](https://image.slidesharecdn.com/advancedfaiichaptertwo-250305131937-09a2ae78/85/Advanced-FA-II-Chapter-Two-pdf111111111-54-320.jpg)