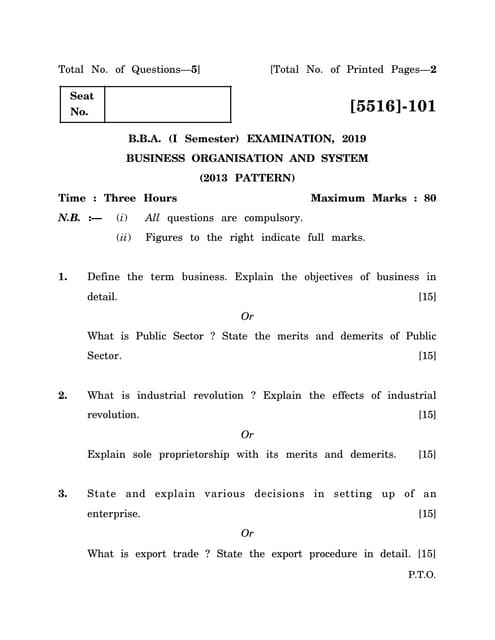

The document provides model questions for accounting for grade 11 students. It contains two sections - Section A with 11 very short answer questions worth 1 mark each. Section B contains 15 short answer questions worth 5 marks each. Some of the questions in Section B require preparing documents like cash book, purchase book, bank reconciliation statement, adjusted trial balance etc. based on the additional information provided.

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

Sub.Code :1031

GRADE XI

Accounting

Model questions

ljBfyL{n] ;s];Dd cfkmg} zAbdf pQ/ lbg'kg]{5 . bfofF lsgf/fdf lbOPsf] cªsn] k"0f{fªs hgfpF5 .

Candidates are required to give their answers in their own words as far as practicable.

The figures in the margin indicate full marks.

Time : 3 Hrs. Full Marks: 75

;d'x “s”(Section “A”)

(clt ;+lIfKt pQ/fTds k|Zgx? / Very Short Answer Questions)

;a} k|Zgx?sf] pQ/ lbg'xf]; . (Attempt All Questions) !!x !=!!

1. n]vf clen]vg eg]sf] s] xf] ?

What is book-keeping?

2. n]vfljlwsf s'g} b'O{ pbb]Zo pNn]v ug'{xf]; .

Mention any two objective of accounting.

3. df}lb|s dfkg cjwf/0fsf] cy{ n]Vg'xf]; .

Write the meaning of money measurement concept.

4. ;Gt'lng k/LIf0fnfO{ kl/eflift ug'{xf]; .

Define trial balance.

5. /]vfªlst r]s eg]sf] s] xf] ?

What is cross cheque?

6. ;}4flGts q'l6sf] af/]df n]Vg'xf]; .

Write about error of principle.

7. hu]8f eg]sf] s] xf] ?

What is reserve?

8. k"FhLut vr{ / cfout vr{ aLrsf] s'g} Ps leGgtf n]Vg'xf]; .

Write any one difference between capital expenditure and revenue expenditure.

9. 9kf]6 eg]sf] s] xf] ?

What is dhapot?

10. a}s gubL lstfasf] kl/efiff lbg'xf]; .

Define bank cash book.

11. ah]6 l;6sf] k|of]u pNn]v ug'{xf]; .

State the use of budget sheet.](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-1-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

;d'x “v”(Section “B”)

(;+lIfKt pQ/fTds k|Zgx? / Short Answer Questions)

;a} k|Zgx?sf] pQ/ lbg'xf]; . (Attempt All Questions) * x % = $)

12. A. n]vfk|ls|ofnfO{ ;+If]kdf pNn]v ug'{xf]; . 3

State accounting process in brief.

B. tnsf ljj/0fx?sf] ;xof]uaf6 n]vf ;lds/0f tof/ ug'{xf]; . 2

Prepare accounting equation from following details.

a) gub ?=@,)),))) / kmlg{r/ ?= %,)),))) af6 Aoj;fosf] z'?jft ul/of] .

Started business with cash Rs. 2, 00,000 and furniture Rs. 5, 00,000.

b) gub ?= *),))) / pbf/f] ?= &),))) df ;fdfg vl/b ul/of] .

Purchase goods worth Rs. 80,000 on cash and 70,000 on credit.

c) 3/ ef8f ?= (),))) e'Qmfg ul/of] .

Paid rent Rs. 90,000.

d) ?= @),))) sf] ;dfg ?= @%,))) df ljls| ul/of] .

Sold goods costing Rs 20,000 on cash Rs. 25,000.

13. A. gub / a}+ssf sf/f]af/x? tn lbOPsf 5g:

Cash and banking transactions are given below:

kf}if !M gub / a}s df}hbft s|dz ? ^),))) / ? @,)),)))

Poush 1: Opening balance of cash and bank are Rs. 60,000 and 2, 00,000

respectively.

kf}if !#M gub ? #),))) a}+sdf hDdf ul/of] .

Poush 13: Cash deposited in bank of Rs. 30,000.

kf}if @@M /fdnfO{ ?=#@,))) r]s dfk{mt e'QmfgL u/L ?= #%,))) sf] lx;fa ldnfg ul/of] .

Poush 22: Paid of Rs. 32,000 to Ram through cheque for settling account of

Rs. 35,000.

kf}if @&M d]lzg ljs|L afktclj/naf6 ? !(,))) sf] r]s / ?= #,))) gub k|fKt eof] .

Poush 27: Received a cheque from Aviral of Rs. 19,000 and cash Rs. 3,000

for selling machine.

tof/ ug'{xf];M (Required):

tLg dxnLo gub k'l:tsf (Triple column cash book) 3

B. kmlg{r/ vl/b ;DalGw ljj/0f tn lbO{Psf 5g M

Transactions related to furniture purchases are given below:

l8;]Dj/ %M s?0f ;Knfo;{af6 vl/b

Dec 5: Purchase from Karuna suppliers

!) slkm 6]jn ?= !,)),))) df (10 coffee tables for Rs. 1,00,000)](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-2-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

@) j6f ;fgf s'l;{ ?= $,))) sf] b/df (20 small chairs @ Rs. 4,000 each)

Aofkf/ 5'6 !) % (Trade discount @ 10% )

l8;]Dj/ !(M cGhnL 6«]8;{af6 vl/b

Dec 19: Purchased from Anjali traders:

% j6f knª ? !%,))) sf] b/df (5 beds @ 15,000 each)

* j6f ;f]kmf ;]6 ?= @%,))) sf] b/df (8 pieces of sofa @ Rs. 25,000 per sofa)

tof/ kfg'{xf]; (Required): vl/b lstfj (Purchase book) 2

14. ljj/0fx? lgDgfg';f/ lbO{Psf 5g M

Following information are given:

a) gub lstfan] df}Hbft ? *),))) b]vfof] .

Cash book showed a balance of Rs. 80,000.

b) ljleGg r]sx?af6 hDdf ul/Psf] ? &%,))) dWo] ? @),))) dfq a}+sdf hDdf ePsf] b]lvof] .

Bank credited Rs. 20,000 only out of various cheques of Rs. 75,000

deposited in the bank.

c) ?=(),))) sf] r]s hf/L ePsf]df ?=!),))) a/fa/sf] r]s e'QmfgLsf nflu a}+sdf cfhsf ldlt

;Dd k|:t't ePg .

Cheques issued of Rs. 90,000 but a cheque of Rs. 10,000 was not presented

for payment till the date.

d) u|fxsn] r]s dfkm{t hDdf u/]sf] ?=$$,))) sf] gub lstfjsf clen]v b]lvPg .

A customers deposited a cheque of Rs. 44,000 directly in the bank but has

not been recorded in the cash book.

e) a}+sn]] kf; a'sdf a}+s z'Ns ? %)) vr{ s6fPsf] b]lvof] .

Bank debited Rs. 500 as bank charge in the pass book.

f) ?= !@))) sf] r]s k|fKt eof] / gub lstfadf clen]v ul/of] t/ a}+sdf hDdf x'g ;s]g .

Cheque of Rs. 12,000 received and entered into the cash book but failed to

deposit in the bank.

tof/ ug'{xf]; (Required): a}s lx;fa ldnfg ljj/0f (Bank Reconciliation Statement) 5

15. A. ;Gt'ng k/LIf0f tof/ ug'{ cufl8 lgDgfg'';f/sf q'l6x?nfO{ ;Rofpg'xf]; . 3

Rectify following errors before preparing of trial balance.

a) zdf{nfO{ gubdf ljls| ul/Psf] ?= $%,))) pgsf] vftfdf 8]lj6 ul/of]

Cash sales to Sharma Rs. 45,000 debited to his account

b) ?= !(,))) lals| u/]sf] d]lzg vl/b lstfadf e'njz s|]l86 ul/of]

Sales of machinery @ Rs. 19,000 were wrongly credited in sales account.

c) k]df ;Fusf] ?=@),))) sf] j:t' vl/bnfO{ lals| vftfdf clen]v u/Lof]

Purchase goods from Pema Rs. 20,000 recorded in sales book.](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-3-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

B. ;Gt'ng k/LIf0faf6 lgDgfg';f/sf ljj/0fx? lemlsPsf] 5g

Following information are extracted from the trial balance

ljj/0f (Particulars ) 8]lj6 (Debit) ?=(Rs.) s|]l86 (Credit)

?=(Rs)

ljljw cf;fdLx? (Sundry debtors) 52,000

v/fa C0fsf] k|fjwfg (Provision for bad

debt)

7,000

v/fa C0f (Bad debt) 1,000

yk hfgsf/L (Additional information)

a) v/fa C0f ?=@,))) (Bad debt Rs. 2,000)

b) v/fa C0fsf] k|jwfg %% (provision for bad debt @ 5%)

tof/ ug'{xf]; (Required): v/fa C0fsf] k|fjwfg vftf (Provision for bad debt account 2

cyjf (Or),

A 6]«l8Ë sDkgLsf] c;dfof]lht ;Gt'ng k/LIf0f ljj/0f lgDgfg';f/ lbO{Psf] 5

An unadjusted trial balance of 'A' trading concern is given below

ljj/0f (Particulars) 8]lj6 (Debit)

?=(Rs.)

ljj/0f (Particulars) s|]l86 (Credit)

?=(Rs)

hldg tyf ejg (Land and building) 400,000 k"FhL (Capital) 425,000

cf;fdL (Debtors) 225,000 ;fx' (Creditors) 120,000

a}+s df}Hbft (Bank balance) 145,000 ljqmL (Sales) 515,000

tna (Salary) 80,000 C0f (Loan) 250,000

sfof{no vr{ (Office expenses) 40,000

vl/b (Purchase ) 380,000

gub (Cash) 25,000

clu|d aLdf (Prepaid insurance) 15,000

hDdf(Total) 13,10,000 hDdf(Total) 13,10,000

yk hfgsf/L (Additional information):

a) clu|d sfof{no vr{ (Office expenses prepaid) Rs 3,000

b) hldgsf] d"No a[l4 (Land appreciated by) 10%

c) ltg{ afFsL tna (Salary outstanding) Rs. 1500

d) v/fa C0f s§L (Bad debts written off) Rs. 2500

e) clu|d jLdfsf] ;dfKtL (Prepaid insurance expire) Rs. 10,000](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-4-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

tof/ ug'{xf]; (Required): ;dfof]lht ;Gt'ng k/LIf0f (Adjusted Trial balance) 5

16. hgj/L !, @)!* df ABC sDkgLn] ?= ^,)),))) df df]6/ e]g vl/b u¥of] . h'nfO{ !, @)!( df sDkgLn]

csf]{ df]6/ e]g ?= *,)),))) df vl/b u¥of] . ! h'nfO{ @)@) df klxnf vl/b u/]sf] df]6/ e]gnfO{ gub

?= %),))) wf6fdf lals| u¥of] / ;f]lx ldtLdf ?= !),)),))) a/fa/sf] csf]{ df]6/ e]g vl/b u¥of] . l:y/

ls:tf ljlwdf d"No ¥xf;s§L !)% sf b/n] k|ltjif{ sfl6G5 / x/]s jif{ sDkgLsf] sf/f]af/ l8;]Da/sf] #!

df aGb ul/G5 .

On 1st

January, 2018 ABC Company purchased a motor van at Rs. 6, 00,000. On

1st

July, 2019, company purchased another van worth Rs. 8, 00,000. On 1st

July

2020, the first motor van was sold bearing the loss of Rs. 50,000 and on the same

date company purchased another van for Rs. 10,00,000. Depreciation was charged

@10% p.a. under fixed installment method. The accounts of the company were

closed on 31st

December each year.

tof/ ug'{xf]; (Required): tLg jif{sf]nfuL df]6/ e]g vftf (Motor Van account for the first

three years) (1+2+2=5)

17. gjLg 6]«8{;sf] r}q #), @)&! sf] ;Gt'lnt k/LIf0f tn lbO{Psf] 5,

Trial balance of Nabin Trader on Chaitra 30, 2071 is given below.

yk lyk ljj/0f (Additional information)

a) d]l;g/Ldf d"No¥xf; !)% k|ltjif{ (Depreciation on machinery 10% p.a)

b) ltg{ afFsL tna ?=$))) (Salary payable Rs. 4,000)

c) gofF v/fj C0f ?= !,))) (New bad debt Rs. 1,000)

tof/ ug'{xf]; (Required):

a) gfkmf gf]S;fg vftf (Profit & Loss account)

ljj/0f (Particulars) ?=(Rs.) ljj/0f (Particulars ?=(Rs.)

ljls| vr{ (Selling expenses) 5,000 s'n gfkmf(Gross profit b/d) 87,000

Aofh (Interest) 5,000 ;fx' (Creditors) 8,000

cf;fdL (Debtors) 25,000 a}+s C0f(Bank loan) 19,000

v/fa C0f (Bad debt) 2,000 v/fa C0fsf] k|fjwfg

(Provision for bad debt)

2,000

aLdf (Insurance) 1000 k"FhL (Capital) 50,000

tna (Salaries) 20,000

nufgL (Investment) 40,000

gub (Cash) 14,000

d]l;g (Machinery) 50,000

ef8f (Rent) 4,000

hDdf (Total) 166,000 hDdf (Total) 166,000](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-5-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

b) jf;nft (Balance sheet) (3+2)

18. /]8qm;sf] lgDgfg';f/sf ljj/0fx? lbO{Psf 5g (Red Cross provides following information):

!–!–@)!* sf] jf;fnt (Balance Sheet as on 1-1- 2018)

bfloTj (Liabilities) Amount Assets Amount

k"FhL sf]if (Capital fund)

C0f (Loan)

4,00,000

60,000

:y/ ;DkQL (Fixed assets)

nufgL (Investments)

clGtd gub df}Hbft (Closing

cash balance)

3,00,000

1,00,000

60,000

hDdf (Total) 4,60,000 hDdf (Total) 4,60,000

/]8qm;sf] ldlt #!–!@–@)!* sf k|fKtL / e'QmfgLnfO{ tn lbO{Psf] 5

Receipts and payments of Red Cross are given below as on 31st

-12-2018

k|fKtL (Receipts)

;b:o z'Ns (Subscriptions) Rs. 50,000

k|j]z z'Ns (Entrance fees) Rs. 30,000

nufgLdf Aofh (interest on investment) Rs. 5,000

k'/fgf] kmlg{r/ ljqmL (Sale of old Furniture) Rs. 5,000

e'QmfgL (Payment)

6'gf{d]G6 vr{ (Tournament expenses) Rs.10,000

Hofnf(wages) Rs. 20,000

lk|lG6ª (Printing) Rs. 7,500

;fdfGo vr{ (General expenses) Rs. 12,000

;dfrf/kq(Newspaper) Rs. 1,800

cGo ljj/0fx? lgDgfg';f/ lbO{Psf] 5 (Other information and outstanding are given below):

a) lk|lG6ª vr{ ltg{ afFsL ?= %)) / Hofnf ltg{ afFsL ?= #))(Printing outstanding Rs. 500 and

wages outstanding Rs. 3,000)

b) $)% k|j]z z'Ns k'FhLut (40% of the entrance fee is to be capitalized)

c) l:y/ ;DkQLsf] d"No ¥xf; !) % (Fixed assets depreciate by 10%)

d) ;b:o z'Ns afFsL ?=@@,))) (Subscription due for the year Rs. 22,000)

tof/ ug'{xf]; (Required):

a. k|fKtL / e'QmfgL vftf (Receipts and payment a/c)

b. cfo tyf Aoo vftf (Income and Expenditure a/c) (2+3)](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-6-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

19. A. Zj]tfn] Psf]xf]/f] n]vf k|0ffnL cGt{ut n]vf /fVg] ub{l5g . pgn] hgj/L !, @)!& df ?= @,)),)))

df Aoj;fo z'? ul/g . pgL k|ltdlxgf ?= @,))) sf b/n] 3/ vr{sf nflu Aoj;foaf6 gub lemSg]

ub{l5g . pgsf] jif{sf] clGtdsf] Aoj;fosf] ljj/0f lgDgfg';f/ lbO{Psf] 5 .

Shweta keeps her account under the single entry system. She started a

business with Rs. 2,00,000 on 1st

Jan, 2017. She withdraws Rs. 2,000 per

month for household work. The position of her business at the end of the

year was as follows;

l:y/ ;DkQL (Fixed assets) Rs. 1,90,000

df}Hbft (Inventory) Rs. 85,000

ltg{afFsL vr{ (Due expenses) Rs. 10,000

;fx' (Creditors) Rs. 50,000

cf;fdL (Debtors) Rs. 40,000

a}+s df}Hbft (Bank balance) Rs. 60,000

tof/ ug'{xf]; (Required):

a) clGtd cj:yf ljj/0f (Closing statement of affairs)

b) gfkmf gf]S;fg ljj/0f (Statement of profit andloss) (1+1=2)

B. lhNnf:t/Lo sfof{nosf] sf/f]jf/sf] lgDgfg';f/sf] ljj/0f lbO{Psf] 5 M

Following transactions of District level office are given:

a) r}t !, 3/wgL z}n]ifnfO{ k|lt dlxgf ?= *,))) sf b/n] # dlxgfsf 3/ef8f e'Qmfg ul/of] .

Chaitra 1, House rent @ Rs. 8000 per month for three month paid to house

owner Sailesh

b) r}t !%, gf=;'= /fdrGb|n] ?= %))) sf] kmlg{r/ ljn / ?= !))) sf] a}+s ef}r/ k]z ePsfn] lghsf]

k]ZsL ? ^))) km{5of}6 ul/of] .

Chaitra 15, Furniture advance of Rs. 5000 was cleared as per bill of Rs.

6000 and bank voucher of Rs. 1000 submitted by Na. Su. Ramchandra

c) sd{rf/Lsf] sflt{s dlxgfsf] kfl/>lds ?= #)))) (;+rosf]if yk afx]s) dWo] ?= ^))) sd{rf/L

;+rosf]if, ?=#))) ;fdflhs ;'/Iff sf]if / ?= !%)) cfos/ s§f u/L /sd ljt/0f ul/of]] .

Staff renmeration of kartik Rs. 30000 (with out provident fund) was

distributed after deducting P.F. Rs. 6000, social security Rs. 300 and

income tax Rs. 1500.

tof/ ug'xf]; (Required): hg{n ef}r/ (Journal Vouchers) (1+1+1=3)](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-7-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

cyjf (Or),

lgDgfg';f/sf hfgsf/Lx? lbO{Psf 5g (Following information are given):

ah]6 pklzif{s (Budget sub-heads ) aflif{s ah]6 (Annual

budget)

kmfNu'0f ;Ddsf] vr{

(Expenses up to

Falgun)

sd{rf/Lsf] vr{ (Employee

remuneration)

800,000 400,000

sfof{no ;fdfu|L (Office materials) 120,000 60,000

3/ef8f (House rent ) 140,000 80,000

kmlg{r/ / lkml6Ë (Furniture and

fitting)

80,000 35,000

;jf/L ;fwg (Vehicles) 500,000 350,000

r}q dlxgfsf] vr{ (Expenditure for the month of Chaitra):

r}q !, kmlg{r/ vl/b ? !),))) (Chaitra 1: Purchase furniture Rs. 10,000)

r}q %, ;jf/L vl/b ?=!)),))) (Chaitra 5: Purchase vehicles for Rs.100,000)

r}q !), clu|d ef8f e'QmfgL ?= !),)))(Chaitra 10: Advance rent paid for Rs 10,000)

r}q @*, cfo s/ ?=!))) / ;+rosf]if ?= *))) s§L u/]/ sd{rf/Lsf] kfl/>dLs ?= #%))) ljt/0f ul/of]

. (Chaitra 28 Distributed Rs. 35,000 for employee’s remuneration after deducting

income tax Rs. 1,000 and P.F. Rs 8,000)

tof/ ug'{xf]; (Required): ah]6 ljj/0f (Budget Sheet) 5

;d'x “u”(Section “C”)

(la:t[t pQ/fTds k|Zgx? / Short Answer Questions)

;a} k|Zgx?sf] pQ/ lbg'xf]; . (Attempt All Questions) # x * = @$

20. ;dl/og sDklgsf] ljj/0f lgDgfg';f/ lbO{Psf 5g:

Information of Samriyan Enterprises is given below

a. gub ?=@),))) df Aoj;fo z'?

Started a business with Rs. 200,000

b. /fd;Fu ?=!%,))) sf] ;dfg vl/b

Purchase goods of Rs. 15,000 from Ram

c. gub ?= !*,))) df ;dfg ljls|

Goods sold on cash Rs 18,000

d. /fdnfO{ ?= !),))) gub ltl/of]](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-8-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

Cash paid to Ram Rs. 10,000

e. /fd;Fu km]/L gub ?= @),))) sf] ;dfg vl/b

Again goods purchase from Ram of Rs. 20,000

f. /fdnfO{ ?= @$,))) lt/]/ ;Dk'0f{ sf/f]jf/ /fkm;fkm ul/of]

Paid to Ram Rs. 24,000 in full settlement of his account.

tof/ ug'{xf]; (Required):

a. hg{n ef}r/(Journal Entries) b. cfjZos n]h/ (Necessary Ledger) c. ;Gt'ng k/LIf0f (Trail

Balance) (3+4+1)

21. bLks :6f]/sf] #!, l8;]Da/ @)@) sf] ;Gt'ng k/LIf0f lgDgfg';f/ lbOPsf] 5 :

The trail balance of Deepak Store as on 31st

December, 2020 is given below:

ljj/0f (Particulars) ?=(Rs.) ljj/0f (Particulars) ?=(Rs.)

KnfG6 / d]lzg/L(Plant and

machinery)

360,000 kmlg{r/ ljs|L gfKfmf (Gain on

sale of furniture)

10,000

tna vr{(Salary expenses) 71,000 ;fx' (Creditor) 96,000

ljs|L ePsf] j:t'sf] nfut

(Cost of goods sold)

755,000 ljs|L (Sales) 1053,000

cf;fdL (Debtors) 34,500 KnfG6 / d]lzg/Lsf] ;+lrt

d"No¥xf; (Accumulated

depreciation on plant and

machinery)

45,000

clGtdsf] df}Hbft (Stock at

end)

110,000 15% a}+s C0f ( Bank loan

)

56,000

kF"hL lkmtf{ (Drawing) 15,000 k"FhL (Capital) 350,000

10% nufgL (Investment) 120,000 nufgLdf Aofh (Interest on

investment )

10,000

VoftL (Good will) 48,500

UofF; / O{Gwg vr{ (Gas and

oil expenses)

8,000

gub (Cash) 40,000

dd{t vr{ (Repair

expenses)

34,000

clu|d aLdf (prepaid

insurance)

24,000

hDdf (Total) 1620,000 hDdf (Total) 1620,000](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-9-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

yk hfgsf/L (Additional information)

a. tna ljs|Lsf] *)% / k|zf;lgs vr{sf] @)%

Salaries are 80% of selling and 20% administrative expenditure.

b. vr{ ePsf] jLdf ?= !*)))

Insurance expires of Rs. 18,000

c. KnfG6 / d]lzg/Lsf] d"No ¥xf; !%%

Depreciation on plant and machinery is 15%

d. UofF; tyf O{Gwg vr{x? ljs|L vr{

Gas and oil expenses are selling expenses.

tof/ ug'{xf]; (Required):

a. cfo ljj/0f (Income statement based on NFRS)

b. jf;nft (Balance sheet based on NFRS) (4+4=8)

cyjf(Or),

;/sf/L n]vf k|0ffnL eg]sf] s] xf]? gFof ;/sf/L n]vf k|0ffnLsf ljz]iftfx? pNn]v ug'{xf]; . (3+5=8)

What is government accounting? Explain the features of new government

accounting system.

22. A. a}+s gubL lstfa tof/ ug{ lgDg sf/f]jf/x? lbO{Psf 5g 4

Following transactions are given to prepare a bank cash book.

df3 !, a}+s df}Hbft ?= &%,)))

Marga 1: Balance at Bank Rs. 75,000

df3 #, ah]6 lgsf;f ?= #,@%,))) a/fa/sf] a}+s cfb]z k|fKt eof]

Marga 3: Received bank transfer order Rs. 3, 25,000 as a budget release

df3 (, kmlg{r/ vl/bsf nfuL ?= @),))) sf] r]s hf/L ul/of] .

Marga 9: Issued a cheque of Rs. 20,000 for purchasing furniture.

df3 @@, clws[t ;'jf]w /]UdLn] ?= !),))) sf] k':ts vl/b u/]sf] ljn / ?= #,))) gub k]z u/] adf]lhd

lghsf] k]ZsL km5of}6 ul/of] .

Marga 22: Cleared advance of Subodh Regmi against the submission of bill

of book purchase amount of Rs. 10,000 and cash Rs. 3,000.

df3 #), sd{rf/Lsf] df3 dlxgfsf] kfl/>lds ?=**,))) dWo] ?= !^,))) ;+rosf]if / ?= $,))) cfos/

s§f u/L afFsL /sd e'Qmfg ul/of] .

Marga 22, Distributed total salary of Rs. 88,000 after deduction of Provident fund

Rs. 16,000 and income tax of Rs. 4,000.](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-10-320.jpg)

![Source : Curriculum Development Centre, Sanothimi, Bhaktapur

B. lgDgfg';f/sf hfgsf/Lx? lbO{Psf 5g (Following information is given):

ah]6 lzif{s (Budget Heads) aflif{s ah]6

(Annual

Budget)

efb| ;Ddsf] vr{

(Expenditure

upto Bhadra)

cflZjgsf] vr{

(Expenditure of

Aswin)

tna (Salaries)

eQf (Allowances)

sfof{no vr{(Office

expenses)

3/ef8f (House rent)

kmlg{r/ / lkml6ª (Furniture

and fittings)

d]lzg (Machinery)

2,75,000

80,000

60,000

1,50,000

75,000

2,00,000

55,000

10,000

15,000

25,000

35,000

-------

24,000

6,000

3,000

12,000

--------

80,000

hDdf (Total) 8,40,000 1,40,000 1,25,000

yk hfgsf/L (Additional information):

a) zf]wegf{ sf]if ? @,(%,))) (Revolving fund received Rs. 2, 95,000)

b) gub df}Hbft ?= @,))) (Cash Balance Rs. 2,000)

c) km5of}6 x'g afFsL k]ZsL ?= !%)))(Unclear advance Rs. 15,000)

d) glhssf] sfof{noaf6 C0f ?= #,))) (Loan by nearby office Rs. 3,000)

tof/ ug'{xf]; (Required): vr{sf] kmfF6jf/L (Statement of expenditure) [4]](https://image.slidesharecdn.com/1031accounting-230925160428-b52259fa/85/1031_Accounting-pdf-11-320.jpg)

![Chapter 2 Final Accounts Exersice [2].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/chapter2finalaccountsexersice2-240706080329-f5e896f7-thumbnail.jpg?width=640&height=640&fit=bounds)

![Cpt june 2013 question paper with solution[carocks.wordpress.com]](https://cdn.slidesharecdn.com/ss_thumbnails/cptjune2013questionpaperwithsolutioncarocks-wordpress-com-130627051257-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[English Version]Maker-Ray Product Brochure V3 .pdf](https://cdn.slidesharecdn.com/ss_thumbnails/englishversionmaker-rayproductbrochurev3-260113094444-0156dbdc-thumbnail.jpg?width=640&height=640&fit=bounds)

![Alan Lucas - [Template] [Template] [Template] ScienceFairProjectTemplate.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/alanlucas-templatetemplatetemplatesciencefairprojecttemplate-260106222421-b6ad9ab7-thumbnail.jpg?width=640&height=640&fit=bounds)