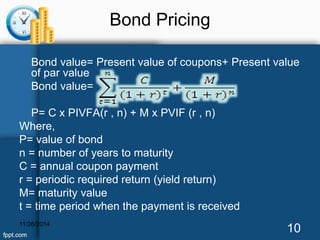

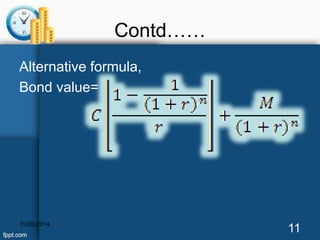

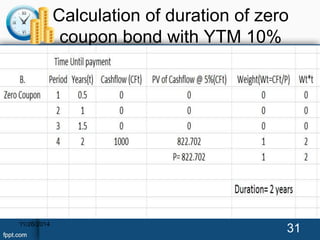

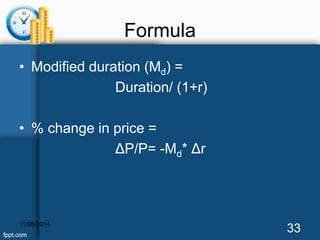

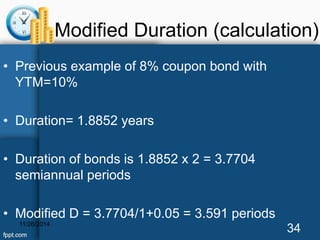

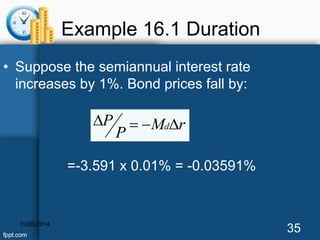

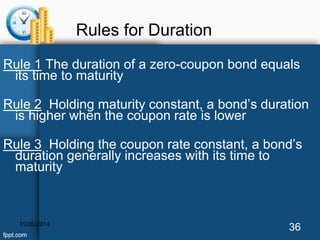

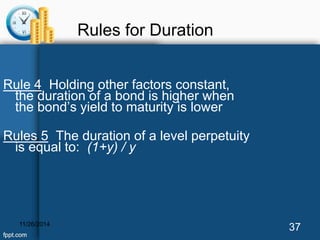

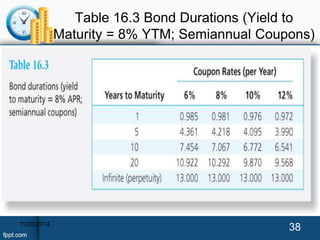

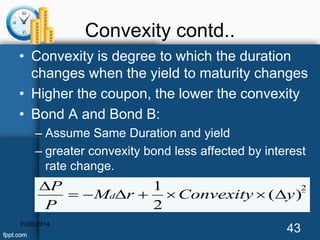

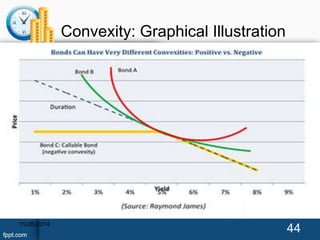

This document discusses managing bond portfolios. It defines what bonds are and describes their key features like par value, coupon rate, maturity date, and yield to maturity. It also covers bond pricing concepts such as yield to maturity, duration, convexity, and how bond prices relate to interest rates. Finally, it provides examples of bonds issued in Nepal.