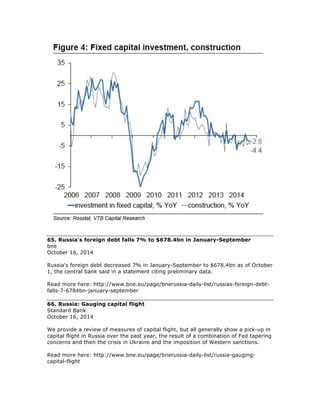

Download to read offline

![highlighted above. With oil at $90/bl, we also estimate an average annual exchange

rate close to RUB41/$, a current account surplus half that in 2014 (we expect

$59.7bn in FY14E) and inflation averaging 7.9% during the year.

Looking at the more severe scenarios, we see growth turning negative (with growth

of -5.8% at $50/bl oil) and the rouble hitting new lows (losing around 20% vs the

dollar at $50/bl). However, the weaker rouble would be likely to stabilise the current

account (we do not foresee FY deficits in any scenario) and alleviating the effects of

a drop in oil prices on the budget (with a deficit below 4% of GDP in the worst case).

As of the beginning of 4Q14, Russia had $454bn of reserves (equivalent to 23% of

GDP or 16 months of import cover), with the government’s sovereign funds

amounting to $173bn (8.6% of GDP).

Within the sovereign funds, the Reserve Fund (intended to help deal with a fall in oil

prices) amounts to $90bn (4.5% of GDP). Therefore, in general even our

hypothetical worst-case scenario looks manageable for the budget.

On the inflation front, we see price growth hitting highs at $80/bl (with annual

average consumer price inflation [CPI] of 8.7%) but coming in lower in the more

severe scenarios, with a widening output gap taking its toll on inflation trends. This

was the case in 2009, when average inflation amounted to 11.7%, after a 22% fall in

the average annual exchange rate. This compare with 14.7% average inflation in

2008 – so, ultimately, inflation slowed. During a negative external shock, Russia

therefore saw some disinflation after years of strong inflationary pressure.

Last but not least, we would like to highlight an important difference between oil-

shock scenarios and our export embargo scenarios. All things being equal, a decline

in oil prices would bring fewer pains for the Russian economy than a ban on Russian

oil exports. The reason is that a ‘price shock’ would be less painful than a ‘volume

shock’ – in the first case, production would remain roughly the same, while in the

second case production would likely be reduced at some point. This would result in

significant spillover effects on other parts of the economy (for instance, stemming

from cuts in employment). The fall in dollar amounts of exports might be the same,

but the consequences would be different. For example, we see Russian exports

declining by $60bn in the event of a 50% cut in Russian crude oil exports to the EU

and by $67bn in the event oil prices fall to $80/bl. However, in the first scenario we

estimate Russian GDP growth would contract by 2.8%, while in the second we see a

contraction of only 1.7%.](https://image.slidesharecdn.com/2eb0-bnecredit-141104005359-conversion-gate02/85/BNE-Credit-October-20-2014-Eastern-EU-Data-12-320.jpg)

![Read more here: http://www.themoscowtimes.com/article/509472.html

75. Ukrainian economy overshadowed by war

OSW

October 17, 2014

Ukraine's financial results over the past few months prove that the economic crisis

which has been ongoing since mid 2012 has exacerbated. According to data from the

Ukrainian Ministry of Economy, Gross Domestic Product for the first six months of

2014 shrank by 3%. In the second quarter, it fell by 4.6%[1] and may further be

reduced by as much as 8-10% over the year as a whole. After the first six months of

this year, the balance of payments deficit reached US$4.3 billion.

Read more here: http://www.bne.eu/page/bneukraine-daily-list/ukrainian-economy-

overshadowed-war

76. Weekly CPI: inflation creeps up and approached 8.2% YoY as of 13

October

VTB Capital

October 17, 2014

News: Rosstat reports that CPI added 0.39% over 1-13 October, with the average

daily inflation ticking up a bit to 0.030% during 7-13 October (from 0.029% in the

previous week). Component-wise, the increases in the prices of cucumbers (+10.9%

WoW), tomatoes (5.7%), gasoline (0.4%), potatoes (2.1%) and cheese (0.5%) were

the key inflation drivers last week.

Read more here: http://www.bne.eu/page/bnerussia-daily-list/weekly-cpi-inflation-

creeps-and-approached-82-yoy-13-october

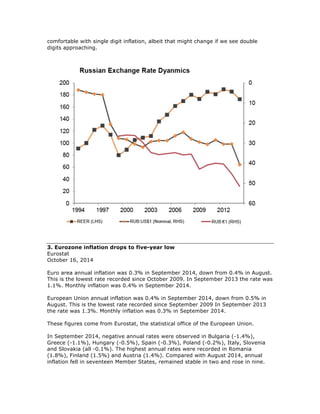

77. Where is the ruble heading?

Tim Ash, Standard Bank

October 17, 2014

We have been seeing some pretty substantive moves on the ruble in recent months -

reflecting $strength, weak oil/commodity prices, Ukraine/sanctions risk, weak growth

drivers, et al. On a basket basis, YTD we are off 15% YTD on a basket basis, record

lows there and against the $and Euro. That said, I attach a REER chart going back to

1994, which still does not suggest the ruble is that cheap.

Read more here: http://www.bne.eu/page/bnerussia-daily-list/where-ruble-heading

78. Falling imports support Russia’s current account surplus

October 17, 2014

BOFIT

October 17, 2014

Preliminary Central Bank of Russia balance-of-payments figures show a third-quarter

current account surplus again rivalling the quarterly surpluses of the previous two

years. For the past four quarters, the current account surplus rose to nearly 3 % of

GDP and the goods trade surplus continued to hold at nearly 10 % of GDP.](https://image.slidesharecdn.com/2eb0-bnecredit-141104005359-conversion-gate02/85/BNE-Credit-October-20-2014-Eastern-EU-Data-43-320.jpg)

This document provides a weekly newsletter summarizing credit stories in Eastern Europe from the previous week. It includes over 100 brief articles on topics like credit ratings changes, macroeconomic indicators, and developments in markets across Eastern Europe and Central Asia. The top credit story was Moody's cutting Russia's credit rating to the second-lowest investment grade due to sluggish growth prospects driven by sanctions, lower oil prices, and capital outflows from Russia.